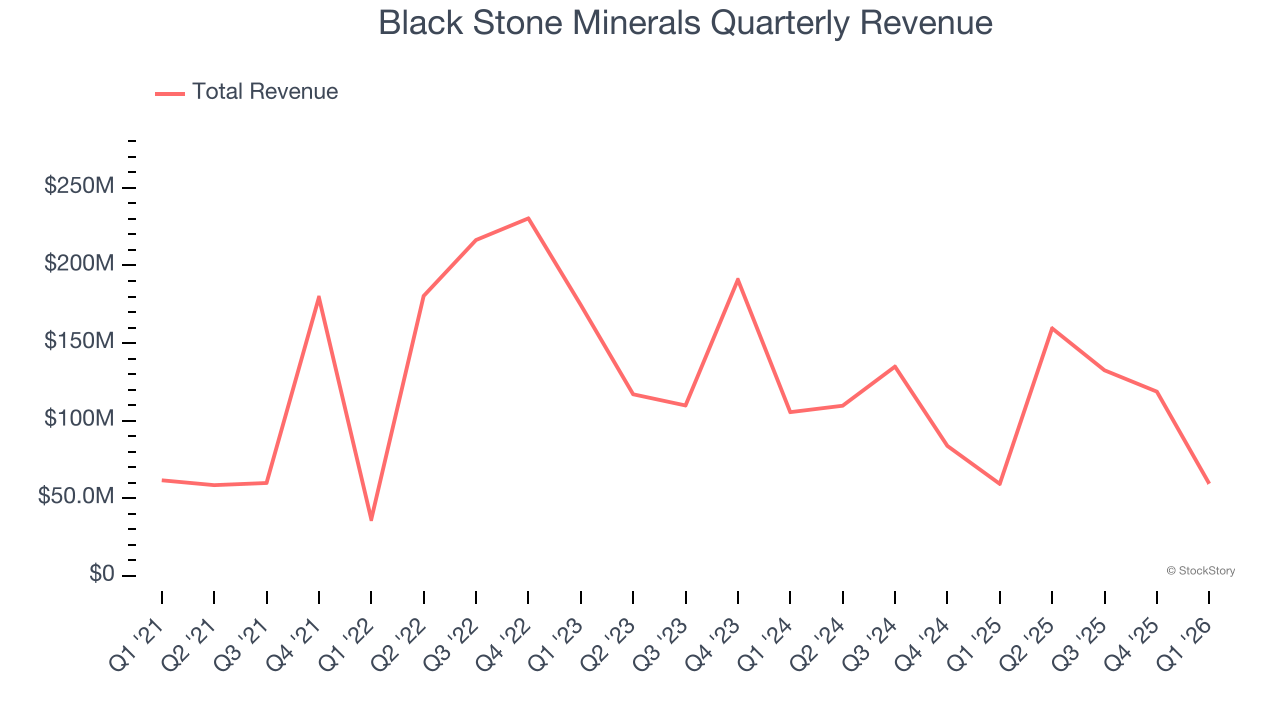

Mineral rights owner Black Stone Minerals (NYSE: BSM) fell short of the market’s revenue expectations in Q1 CY2026, with sales flat year on year at $59.36 million. Its GAAP profit of $0.03 per share was 85.7% below analysts’ consensus estimates.

Is now the time to buy Black Stone Minerals? Find out by accessing our full research report, it’s free.

Black Stone Minerals (BSM) Q1 CY2026 Highlights:

- Revenue: $59.36 million vs analyst estimates of $98.18 million (flat year on year, 39.5% miss)

- EPS (GAAP): $0.03 vs analyst expectations of $0.21 (85.7% miss)

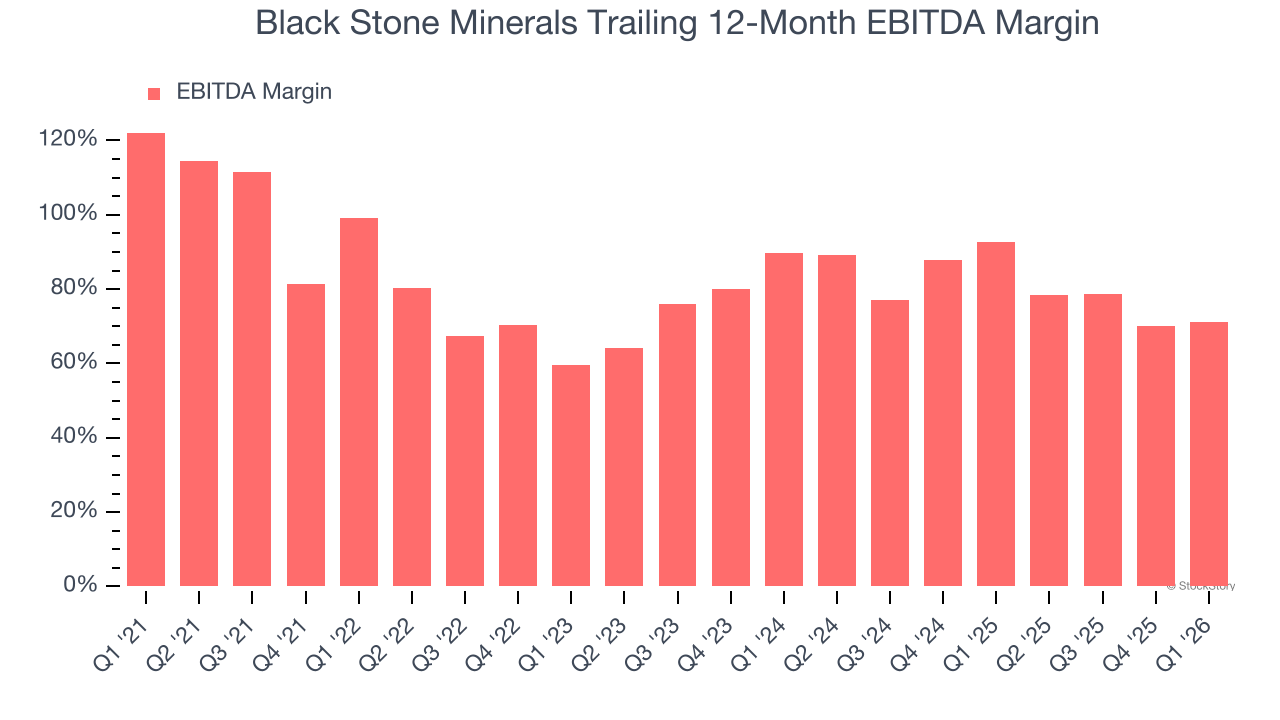

- Adjusted EBITDA: $87 million vs analyst estimates of $68.71 million (147% margin, 26.6% beat)

- Operating Margin: 28%, in line with the same quarter last year

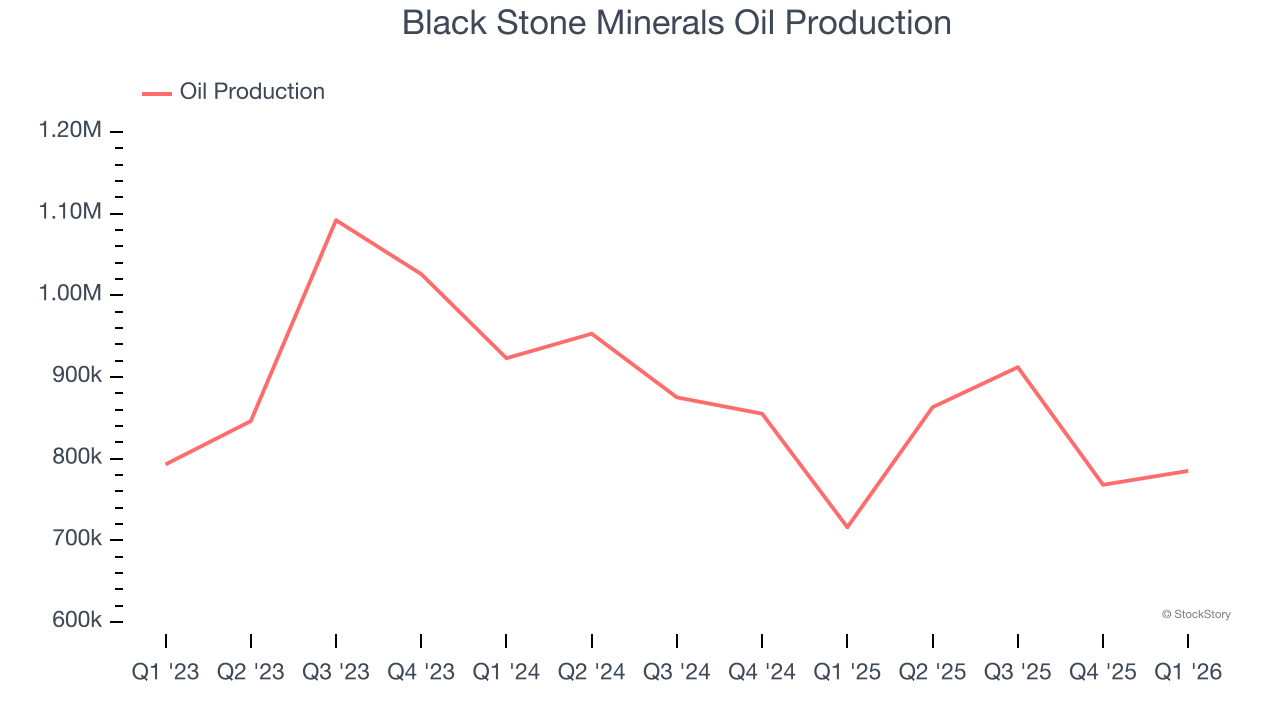

- Oil production: up 9.6% year on year

- Market Capitalization: $3.02 billion

“During the first quarter, we continued to execute across our commercial initiatives, building on the momentum established in 2025,” said Fowler Carter, Co-CEO and President of Black Stone Minerals.

Company Overview

With roots dating to the late 1800s when railroads were expanding westward and land grants were common, Black Stone Minerals (NYSE: BSM) owns oil and natural gas mineral rights across the U.S., earning royalties when energy companies drill on its land.

Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Over the last five years, Black Stone Minerals grew its sales at an impressive 16.3% compounded annual growth rate. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Energy cycles can be long enough that a single five-year period can still reflect one price environment, which is why an additional, decade-long view can help capture through-cycle performance. Black Stone Minerals’s annualized revenue growth of 2.5% over the last ten years is below its five-year trend, but we still think the results suggest decent demand.

Revenue provides useful context, but it is heavily influenced by commodity prices and acquisitions. Production volumes, by contrast, reveal whether the underlying asset base is actually growing. Over the last two years, Black Stone Minerals’s oil production averaged 6.5% year-on-year declines while its natural gas production averaged 6.1% year-on-year declines.

This quarter, Black Stone Minerals’s $59.36 million of revenue was flat year on year, falling short of Wall Street’s estimates. This quarter, Black Stone Minerals reported year-on-year Oil production growth of 9.6%.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted EBITDA Margin

Black Stone Minerals has been a well-oiled machine over the last five years. It demonstrated elite profitability for an upstream and integrated energy business, boasting an average EBITDA margin of 78.3%.

Analyzing the trend in its profitability, Black Stone Minerals’s EBITDA margin decreased by 28.1 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Black Stone Minerals generated an EBITDA margin profit margin of 147%, up 7.9 percentage points year on year. This increase was a welcome development and shows it was more efficient. This adjusted EBITDA beat Wall Street’s estimates by 26.6%.

Cash Is King

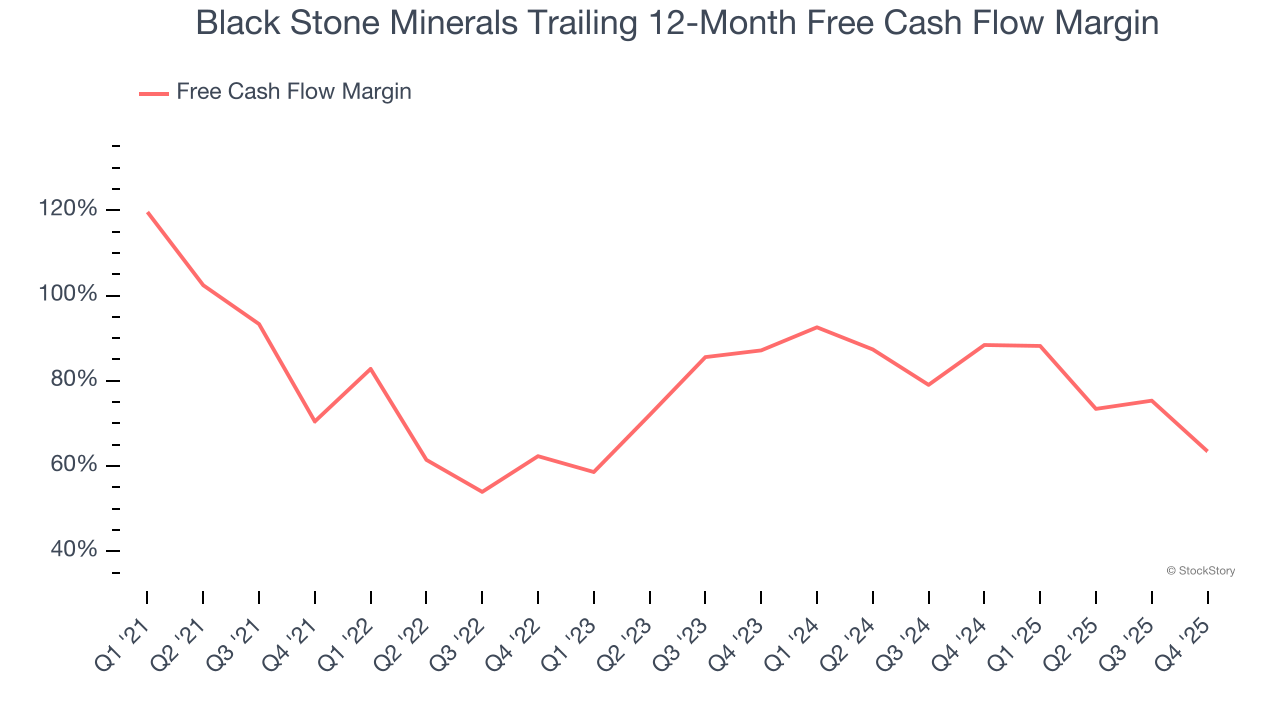

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

Black Stone Minerals has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging an eye-popping 73.6% over the last five years.

Absolute FCF margin levels matter but so does stability of free cash flow. All else equal, we’d prefer a 25.0% average free cash flow margin that is quite steady no matter how commodity prices behave rather than extremely high margins when times are good and negative ones when they’re tough.

Black Stone Minerals’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 2 (lower is better), indicating excellent insulation from commodity swings. This stability supports superior capital access in downturns and positions Black Stone Minerals to act as a consolidator when weaker peers are forced to retrench.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Black Stone Minerals? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Key Takeaways from Black Stone Minerals’s Q1 Results

We were impressed by how significantly Black Stone Minerals blew past analysts’ EBITDA expectations this quarter. On the other hand, its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $14.13 immediately after reporting.

Big picture, is Black Stone Minerals a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).