Artificial intelligence (AI) server firm Super Micro Computer (SMCI) is finding itself in murkier waters. As if smuggling Nvidia (NVDA) chips in contravention of export controls was not enough, the company's own shareholders have now accused Super Micro of falsely inflating sales and the price of SMCI stock. Shareholders filed the suit in a federal court in San Francisco, California, and are seeking unspecified damages for investors between April 30, 2024, and March 19, 2026.

However, to answer the question in the title, this news may not really matter for the stock now. To me, Super Micro has already been one to avoid — not because of its capabilities, but because of its governance issues. Now, a complete overhaul of leadership looks like it may be the only way out for the company.

Super Micro's Financials Are Decent on the Surface

Super Micro Computer delivered a notably strong performance in the fiscal second quarter of 2026, marking the first quarter in some time where it beat expectations on both the top and bottom lines. Net sales surged to $12.7 billion, more than doubling from $5.7 billion in the year-ago period, while EPS rose 17% year-over-year (YOY) to $0.69, comfortably exceeding the Street consensus of $0.49.

For Q3 2026, the company guided for net sales of at least $12.3 billion and EPS of at least $0.60. That implies growth of approximately 167% YOY and 94% YOY, respectively.

On the cash flow side, the first six months of the fiscal year showed an operating cash outflow of $941.4 million, compared with a positive $169.1 million in the prior-year period. The company still maintained a healthy liquidity position, ending the quarter with approximately $4.19 billion in cash and equivalents, significantly above its short-term debt

Valuation-wise, shares of Super Micro appear relatively attractive. The forward price-to-earnings (P/E) ratio stands at 12 times while the forward price-to-sales (P/S) ratio stands at 0.61 times, both well below the sector medians. SMCI stock is down 25% on a year-to-date (YTD) basis.

Competition Is Another Area of Hurt

The recent wave of governance controversies and the March 2026 shareholder lawsuit have undoubtedly cast a heavy shadow over Super Micro Computer. While the company has been nimble in capturing early market share in the AI infrastructure space, these mounting legal and reputational risks are causing hyperscalers and risk-averse enterprise clients to reconsider their vendor allocations. Consequently, the company has been forced into survival pricing, drastically compressing its gross margins in early 2026.

In stark contrast, established peers like Dell Technologies (DELL) and Hewlett Packard Enterprise (HPE) are capitalizing on the upheaval by offering an appealing mix of stability, robust supply chains, and comprehensive IT services. Notably, Dell has positioned itself as a formidable heavyweight, recently boasting a staggering $43 billion AI server backlog. Similarly, Hewlett Packard provides another avenue for enterprise buyers who prioritize secure, managed deployments over cutting-edge hardware release cycles. These competitors are also no longer trailing in technological capability, as they have aggressively invested in liquid cooling and high-density rack manufacturing to close the gap that once made Super Micro the undisputed leader.

Meanwhile, although Super Micro has long championed its modular approach which allows it to swiftly bring new GPU platforms to market months ahead of the competition, Dell has effectively neutralized this advantage with its latest PowerEdge liquid-cooled series. Dell now pushes extreme density with 72 GPUs capable of handling up to 480 kilowatts with near-perfect heat capture, claiming up to a 25 times efficiency improvement over traditional air-cooled systems.

Notably, Hewlett Packard is taking a slightly different route to capture the enterprise market. Rather than engaging in a pure specifications arms race emphasizing raw exaflops, the company integrates its ProLiant and Edgeline servers with advanced silicon-level security and cloud-like management software. This turnkey approach resonates deeply with corporate IT departments that need reliable AI integration without the overhead of managing customized superclusters.

Now, Dell and Hewlett Packard match or exceed Super Micro in thermal efficiency and compute density, pairing these capabilities with the enterprise reliability that the current market heavily favors.

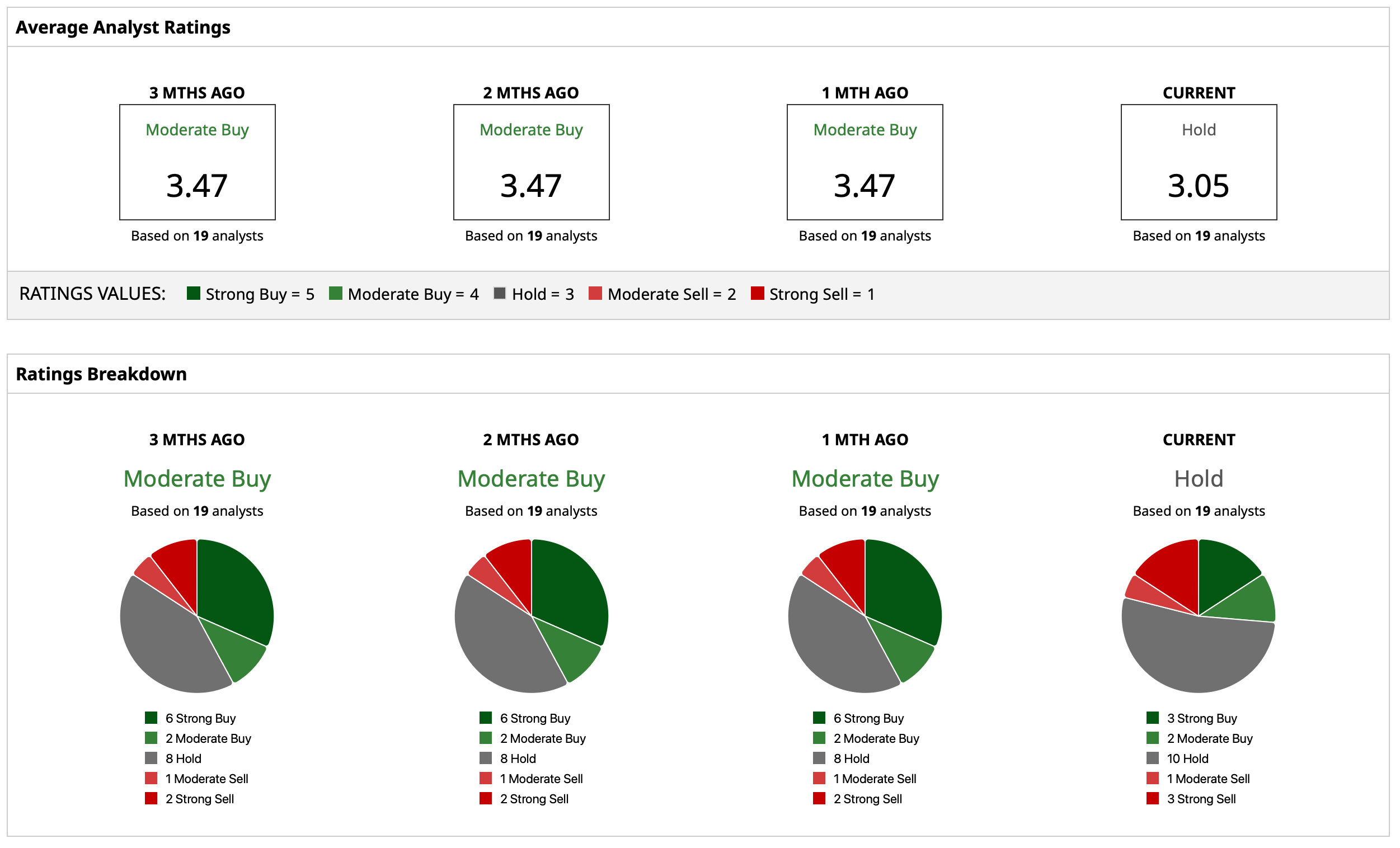

What Do Analysts Think of SMCI Stock?

Overall, analysts have a consensus “Hold” rating on SMCI stock. The mean price target of $34.67 implies potential upside of about 59% from current levels. Out of 19 analysts covering SMCI stock, three have a “Strong Buy” rating, two have a “Moderate Buy” rating, 10 have a “Hold” rating, one has a “Moderate Sell” rating, and three have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Amazon Just Lost a Key AI Chip Executive. Is That Bad News for AMZN Stock?

- Meta Platforms Stock Is Firmly in Oversold Territory. Should You Buy the Dip?

- An Oil Price Shock Is Hurting Carnival Stock. But Is It a Buy Now in Hopes of a Quick Turnaround?

- Bill Ackman Is Pounding the Table on Fannie Mae. Should You Buy FNMA Stock Today?