Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Boot Barn (NYSE: BOOT) and the best and worst performers in the apparel and footwear retail industry.

Apparel and footwear was once a category thought to be relatively safe from major e-commerce penetration because of the need to try on, touch, and feel products, but the category is now meaningfully transacted online. Everyone still needs clothes and shoes to go outside unless they want some curious (or horrified) looks. But this ongoing digitization is forcing apparel and footwear retailers–that once only had brick-and-mortar stores–to respond with omnichannel offerings. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stagnate, so the evolution of clothing and shoes sellers marches on.

The 9 apparel and footwear retail stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 2.6% on average since the latest earnings results.

Boot Barn (NYSE: BOOT)

With a strong store presence in Texas, California, Florida, and Oklahoma, Boot Barn (NYSE: BOOT) is a western-inspired apparel and footwear retailer.

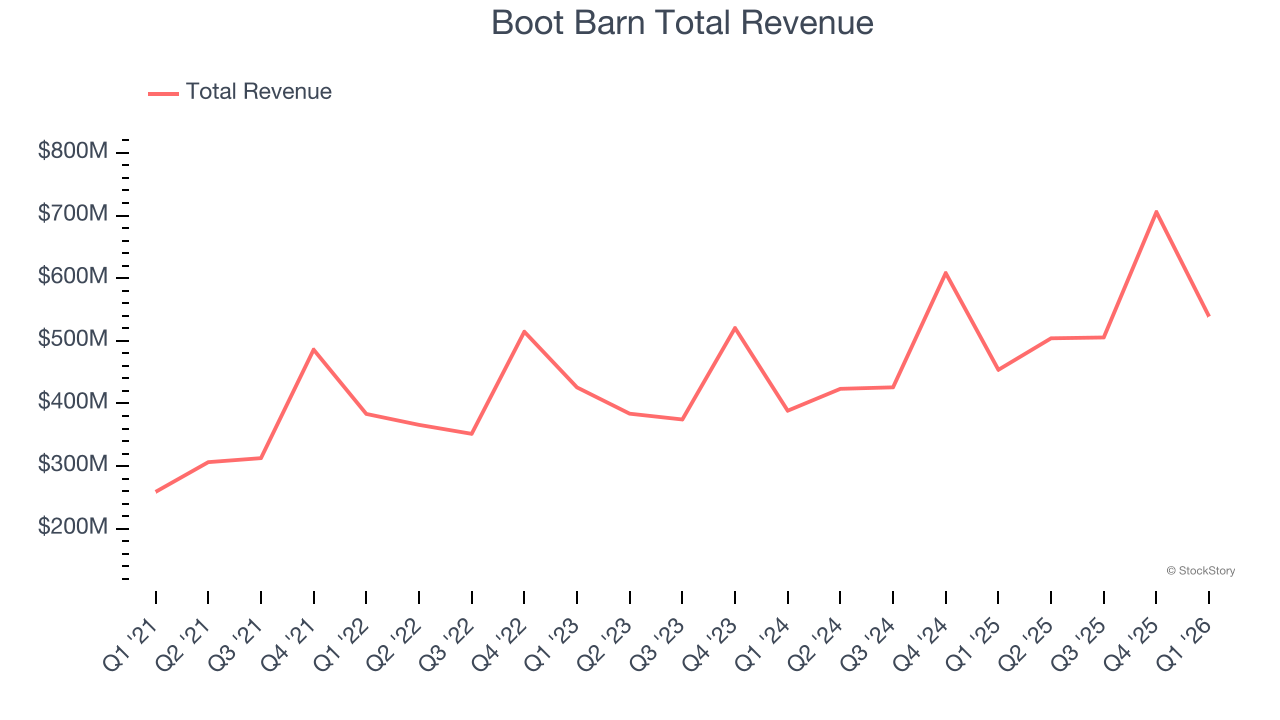

Boot Barn reported revenues of $538.8 million, up 18.7% year on year. This print exceeded analysts’ expectations by 1.5%. Overall, it was a satisfactory quarter for the company with an impressive beat of analysts’ EBITDA estimates but EPS guidance for next quarter missing analysts’ expectations significantly.

John Hazen, Chief Executive Officer, commented, “I am very proud of our performance in Fiscal 2026, which marked a record year for Boot Barn and reflects the strength of our business and the dedication of our team. We delivered strong results across key metrics, including 18% total sales growth, 80 basis points of merchandise margin expansion, and 25% growth in earnings per diluted share. We opened 80 new stores and generated 7.2% same store sales growth. The broad-based strength across merchandise categories, channels, and geographic regions underscores the strong appeal of the brand and the disciplined execution of our strategic initiatives. Looking ahead, I believe Boot Barn is well positioned to build on this foundation, and I remain confident in our ability to drive continued growth and deliver long-term value for our shareholders.”

Boot Barn achieved the fastest revenue growth of the whole group. Unsurprisingly, the stock is up 18.9% since reporting and currently trades at $174.

Is now the time to buy Boot Barn? Access our full analysis of the earnings results here, it’s free.

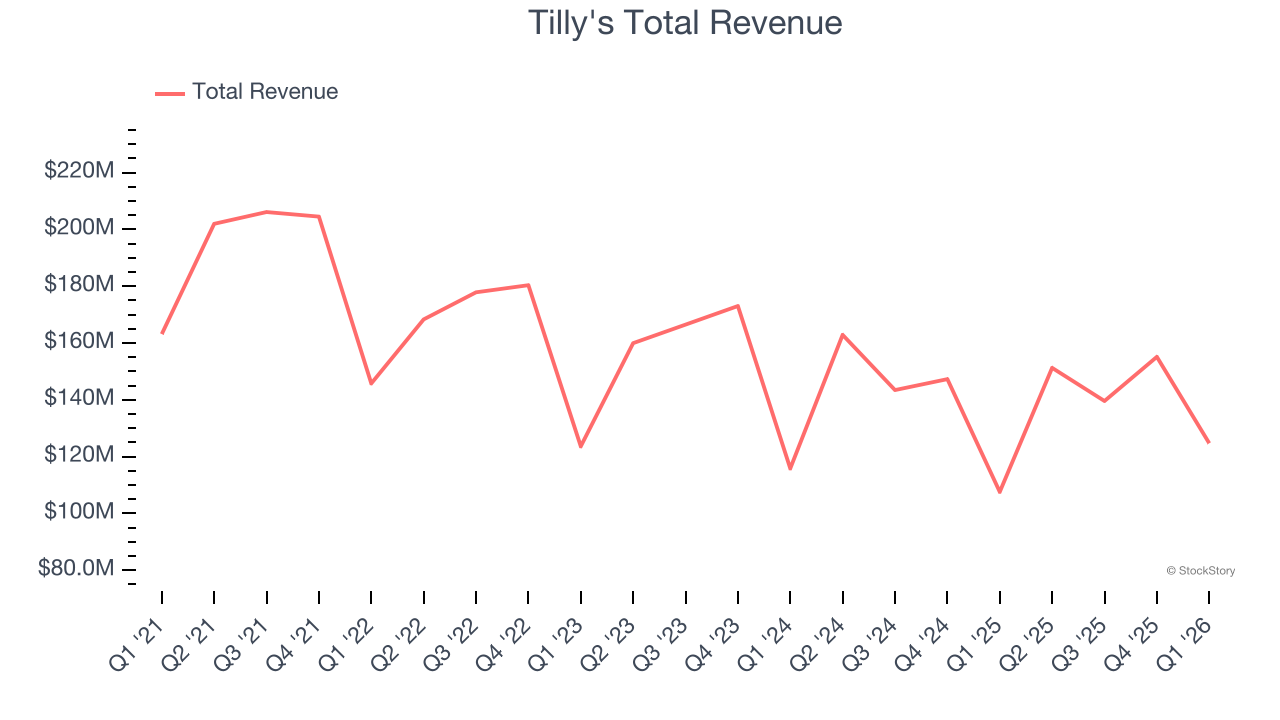

Best Q1: Tilly's (NYSE: TLYS)

With an emphasis on skate and surf culture, Tilly’s (NYSE: TLYS) is a specialty retailer that sells clothing, footwear, and accessories geared towards fashion-forward teens and young adults.

Tilly's reported revenues of $124.7 million, up 15.9% year on year, outperforming analysts’ expectations by 2.8%. The business had an exceptional quarter with EPS guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ gross margin estimates.

Tilly's delivered the biggest analyst estimate beat and highest guidance raise among its peers. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $4.45.

Is now the time to buy Tilly's? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Lululemon (NASDAQ: LULU)

Originally serving yogis and hockey players, Lululemon (NASDAQ: LULU) is a designer, distributor, and retailer of athletic apparel for men and women.

Lululemon reported revenues of $2.47 billion, up 4.3% year on year, exceeding analysts’ expectations by 1.7%. Still, it was a softer quarter as it posted full-year EPS guidance missing analysts’ expectations and EPS guidance for next quarter missing analysts’ expectations significantly.

Lululemon delivered the weakest guidance update and weakest full-year guidance update in the group. As expected, the stock is down 12.4% since the results and currently trades at $109.38.

Read our full analysis of Lululemon’s results here.

Gap (NYSE: GAP)

Operating under the Gap, Old Navy, Banana Republic, and Athleta brands, Gap (NYSE: GAP) is an apparel and accessories retailer selling casual clothing to men, women, and children.

Gap reported revenues of $3.50 billion, flat year on year. This result came in 0.8% below analysts’ expectations. Aside from that, it was a mixed quarter as it also produced full-year EPS guidance slightly topping analysts’ expectations but a miss of analysts’ EBITDA estimates.

Gap had the weakest performance against analyst estimates and slowest revenue growth among its peers. The stock is down 17.6% since reporting and currently trades at $20.59.

Read our full, actionable report on Gap here, it’s free.

American Eagle (NYSE: AEO)

With a heavy focus on denim, American Eagle Outfitters (NYSE: AEO) is a specialty retailer offering an assortment of apparel and accessories to young adults.

American Eagle reported revenues of $1.20 billion, up 9.7% year on year. This print beat analysts’ expectations by 0.9%. Taking a step back, it was a mixed quarter as it also recorded a beat of analysts’ EPS estimates but a miss of analysts’ EBITDA estimates.

The stock is flat since reporting and currently trades at $17.75.

Read our full, actionable report on American Eagle here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.