Illumina has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 15% to $140.33 per share while the index has gained 13.3%.

Is there a buying opportunity in Illumina, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Illumina Not Exciting?

We're swiping left on Illumina for now. Here are three reasons you should be careful with ILMN and a stock we'd rather own.

1. Long-Term Revenue Growth Disappoints

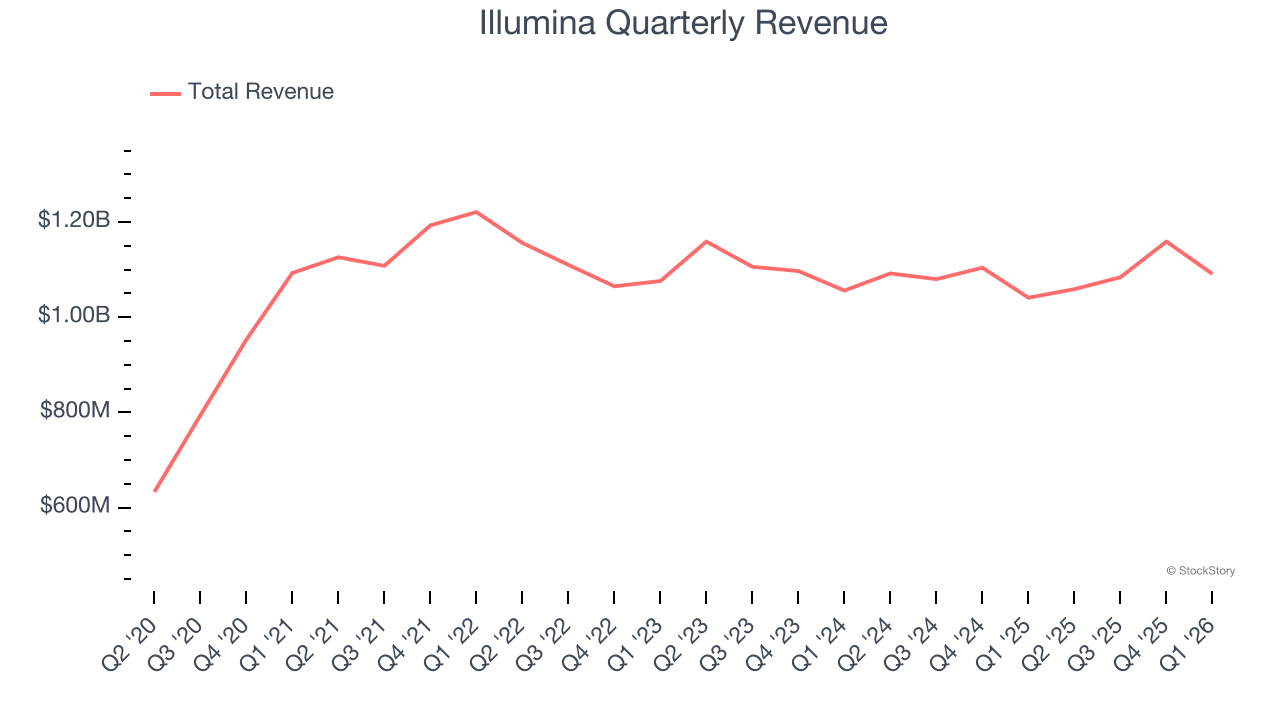

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Illumina grew its sales at a mediocre 4.8% compounded annual growth rate. This was below our standard for the healthcare sector.

2. Core Business Falling Behind as Demand Plateaus

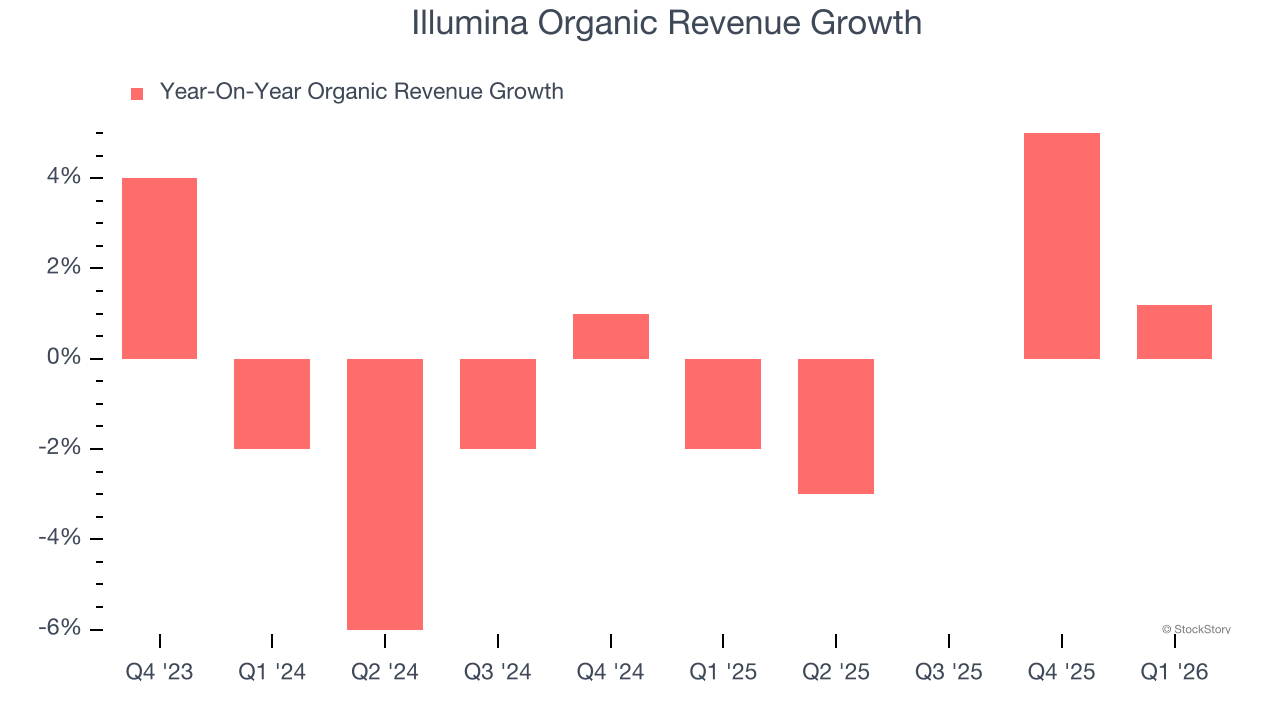

Investors interested in Genomics & Sequencing companies should track organic revenue in addition to reported revenue. This metric gives visibility into Illumina’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Illumina failed to grow its organic revenue. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Illumina might have to lean into acquisitions to accelerate growth, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

3. Previous Growth Initiatives Haven’t Paid Off Yet

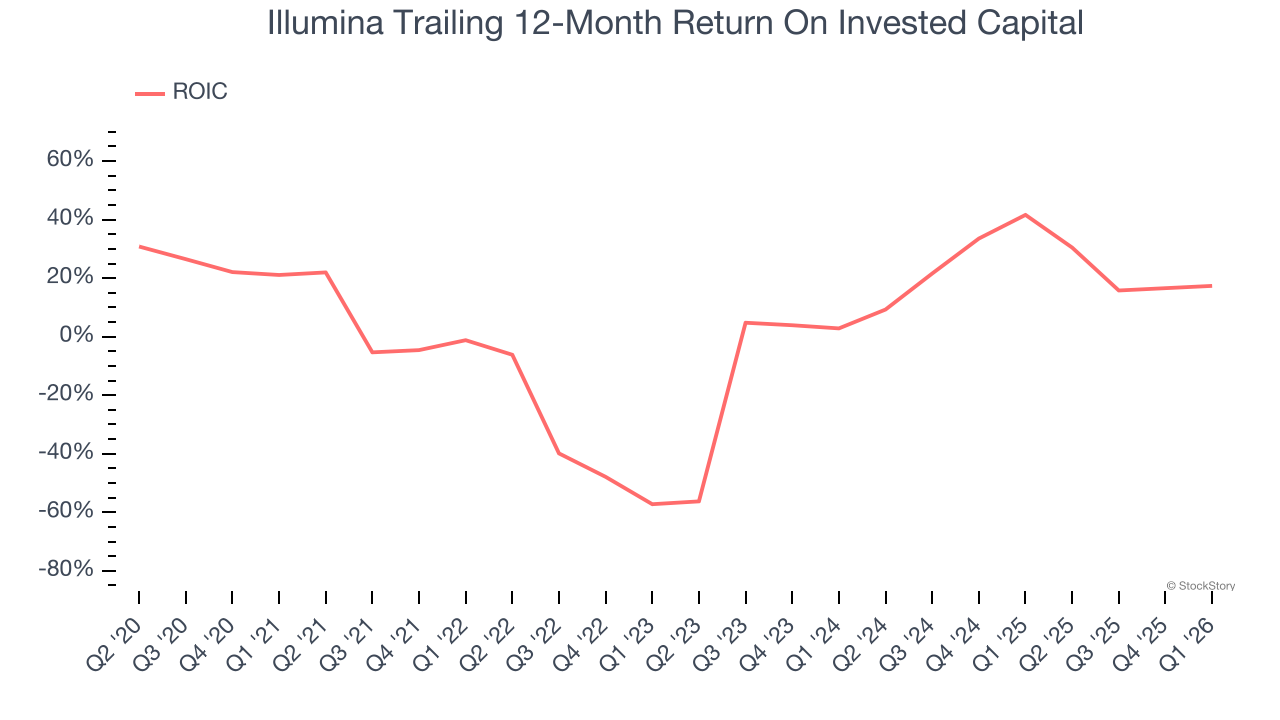

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Illumina historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.7%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

Final Judgment

Illumina’s business quality ultimately falls short of our standards. That said, the stock currently trades at 26.6× forward P/E (or $140.33 per share). At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of Illumina

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week - FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.