Over the past six months, First Bancorp has been a great trade, beating the S&P 500 by 14.9%. Its stock price has climbed to $58.62, representing a healthy 17.5% increase. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in First Bancorp, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is First Bancorp Not Exciting?

Despite the momentum, we're cautious about First Bancorp. Here are three reasons why FBNC doesn't excite us and a stock we'd rather own.

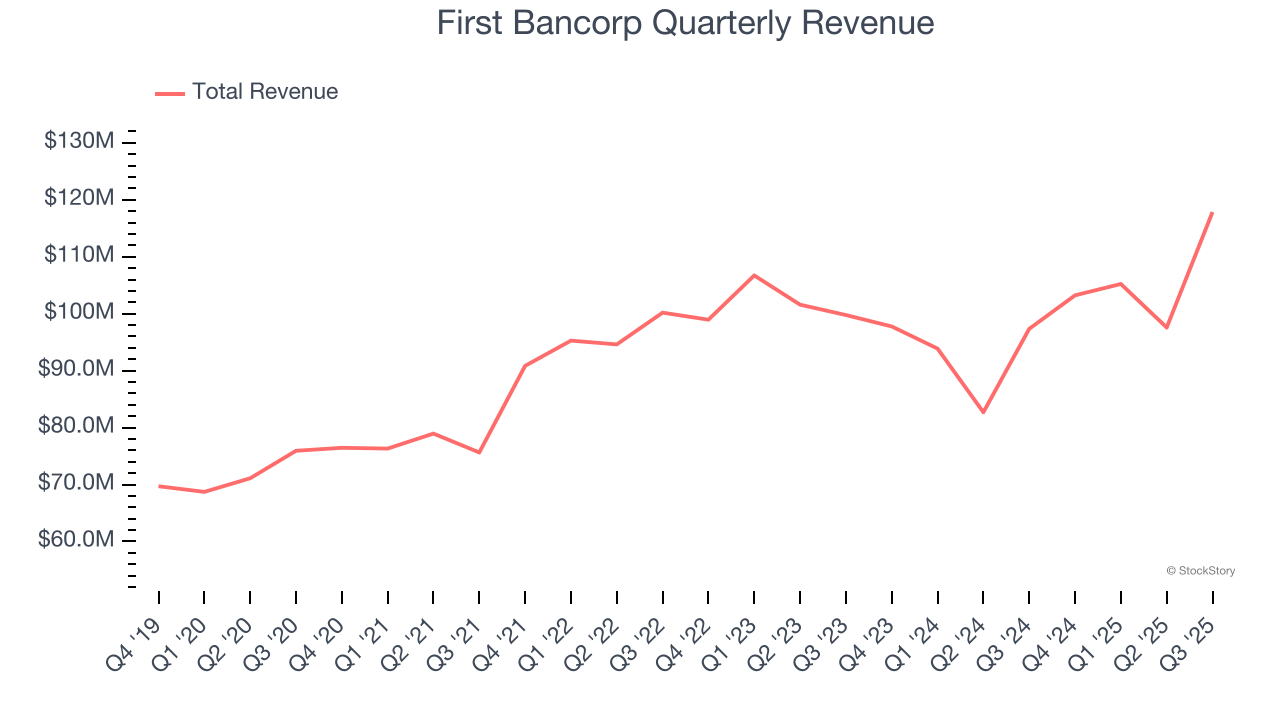

1. Long-Term Revenue Growth Disappoints

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees.

Over the last five years, First Bancorp grew its revenue at a mediocre 8.2% compounded annual growth rate. This fell short of our benchmark for the banking sector.

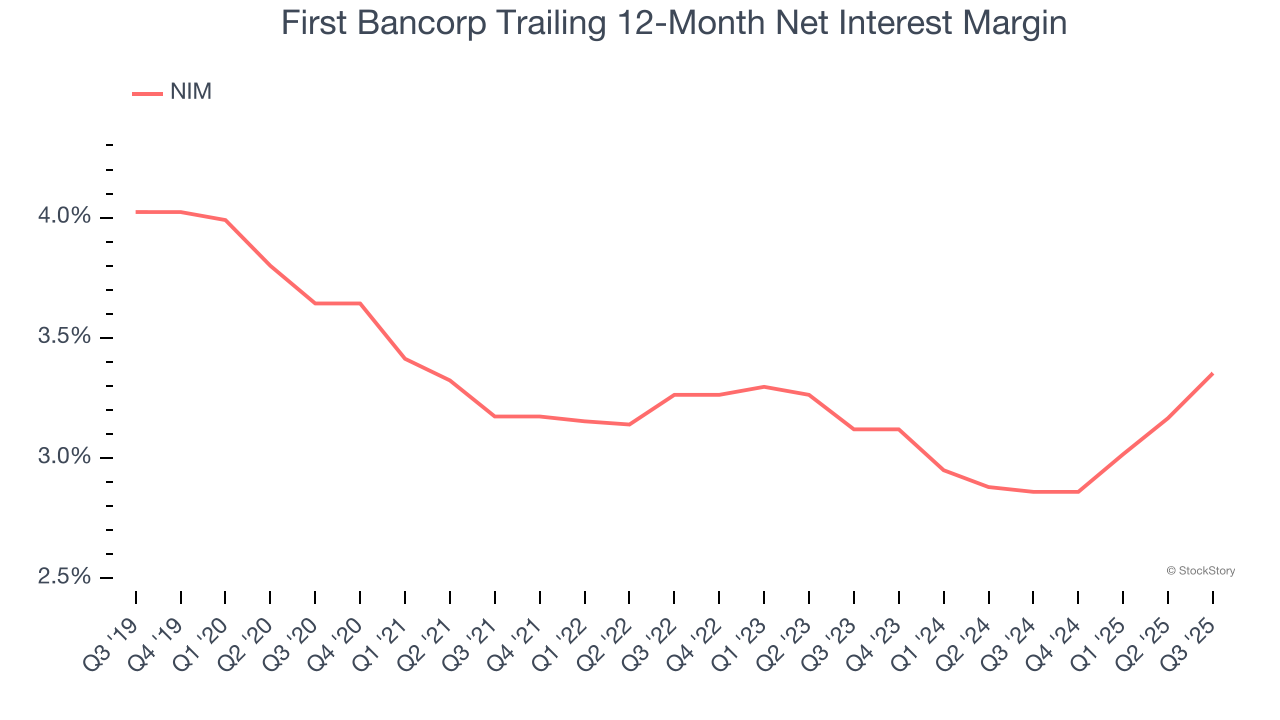

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It's one of the most important metrics to track because it shows how a bank's loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, we can see that First Bancorp’s net interest margin averaged a subpar 3.1%, meaning it must compensate for lower profitability through increased loan originations.

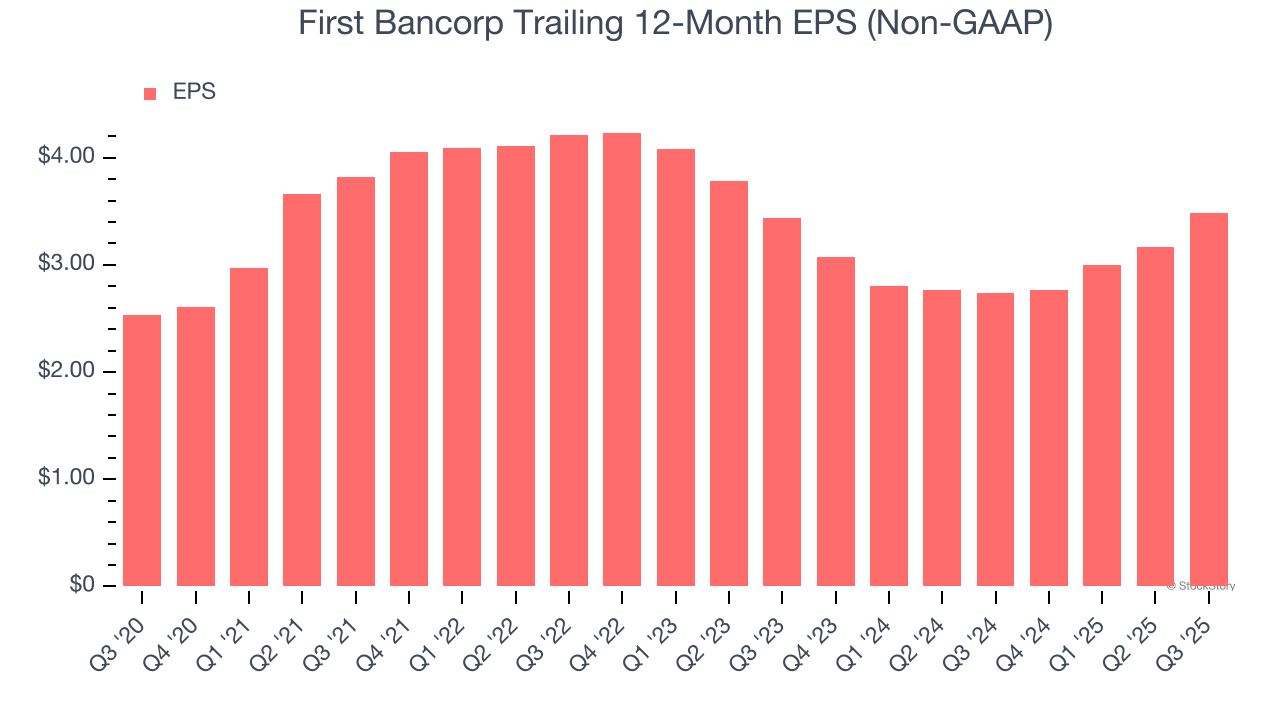

3. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

First Bancorp’s unimpressive 6.5% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Final Judgment

First Bancorp isn’t a terrible business, but it doesn’t pass our bar. With its shares topping the market in recent months, the stock trades at 1.5× forward P/B (or $58.62 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. Let us point you toward our favorite semiconductor picks and shovels play.

Stocks We Like More Than First Bancorp

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.