Renasant currently trades at $35.66 per share and has shown little upside over the past six months, posting a small loss of 4.9%. The stock also fell short of the S&P 500’s flat performance during that period.

Is now the time to buy Renasant, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Renasant Not Exciting?

We're sitting this one out for now. Here are three reasons there are better opportunities than RNST and a stock we'd rather own.

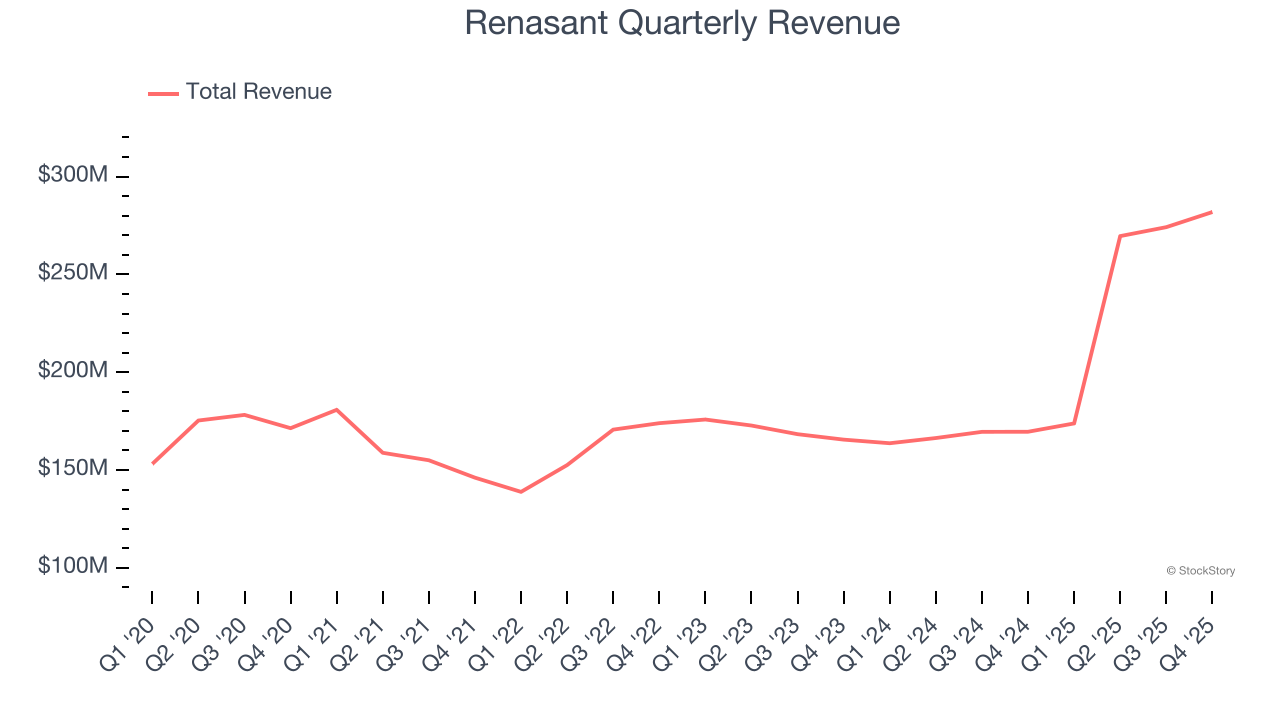

1. Long-Term Revenue Growth Disappoints

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees.

Unfortunately, Renasant’s 8.1% annualized revenue growth over the last five years was mediocre. This was below our standard for the banking sector.

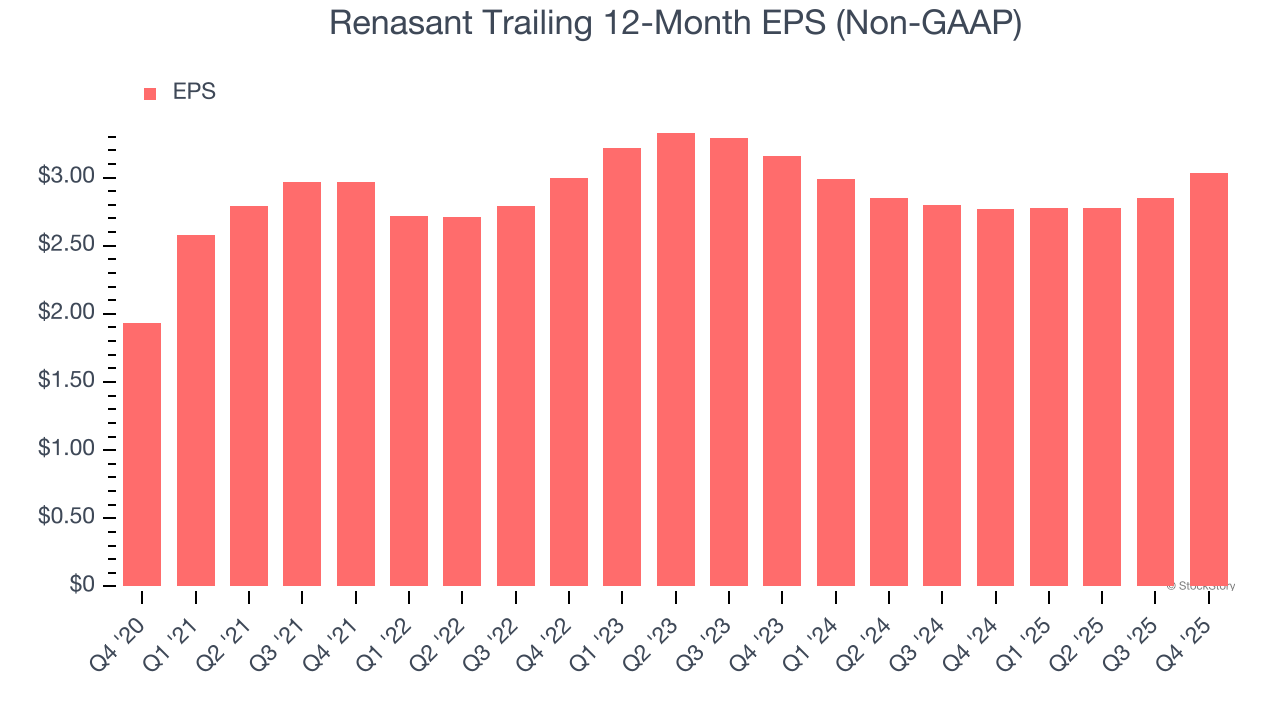

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Renasant’s unimpressive 9.4% annual EPS growth over the last five years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

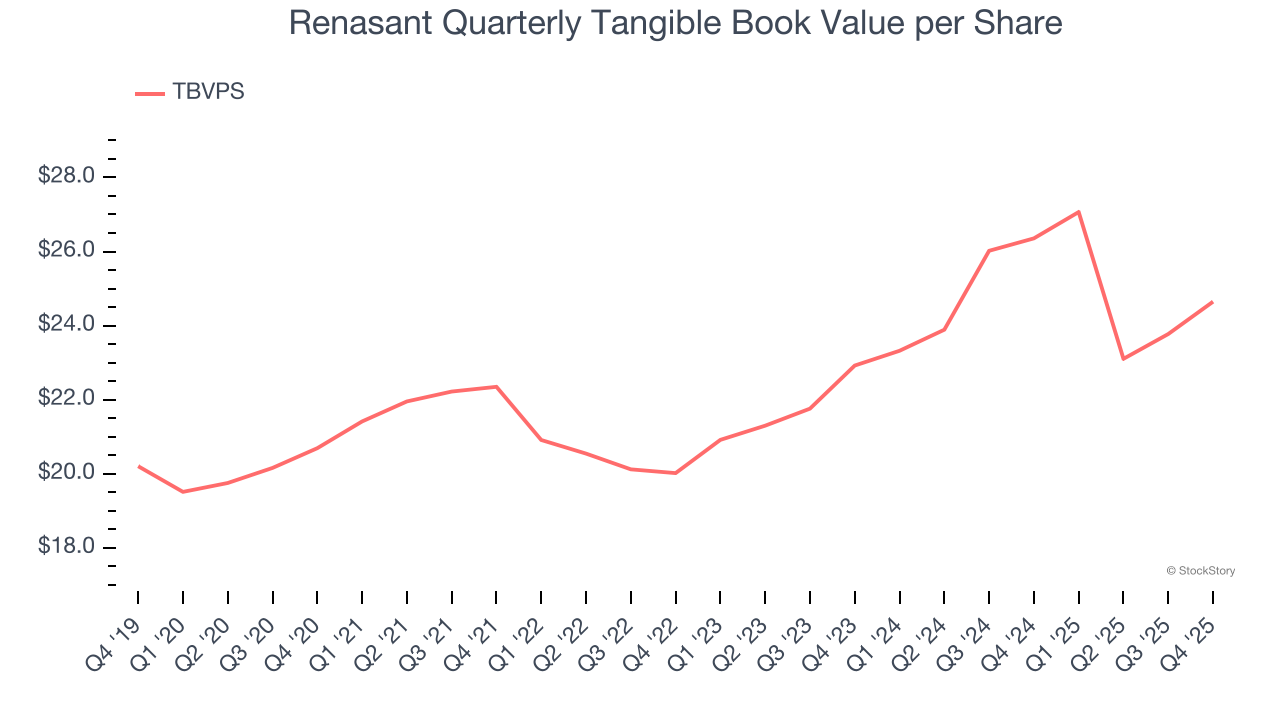

3. Substandard TBVPS Growth Indicates Limited Asset Expansion

Tangible book value per share (TBVPS) serves as a key indicator of a bank’s financial strength, representing the hard assets available to shareholders after removing intangible assets that could evaporate during financial distress.

To the detriment of investors, Renasant’s TBVPS grew at a sluggish 3.7% annual clip over the last two years.

Final Judgment

Renasant isn’t a terrible business, but it isn’t one of our picks. With its shares lagging the market recently, the stock trades at 0.8× forward P/B (or $35.66 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.