Essent Group has been treading water for the past six months, recording a small loss of 4.2% while holding steady at $56.54. The stock also fell short of the S&P 500’s 5% gain during that period.

Is there a buying opportunity in Essent Group, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Essent Group Not Exciting?

We're swiping left on Essent Group for now. Here are three reasons why you should be careful with ESNT and a stock we'd rather own.

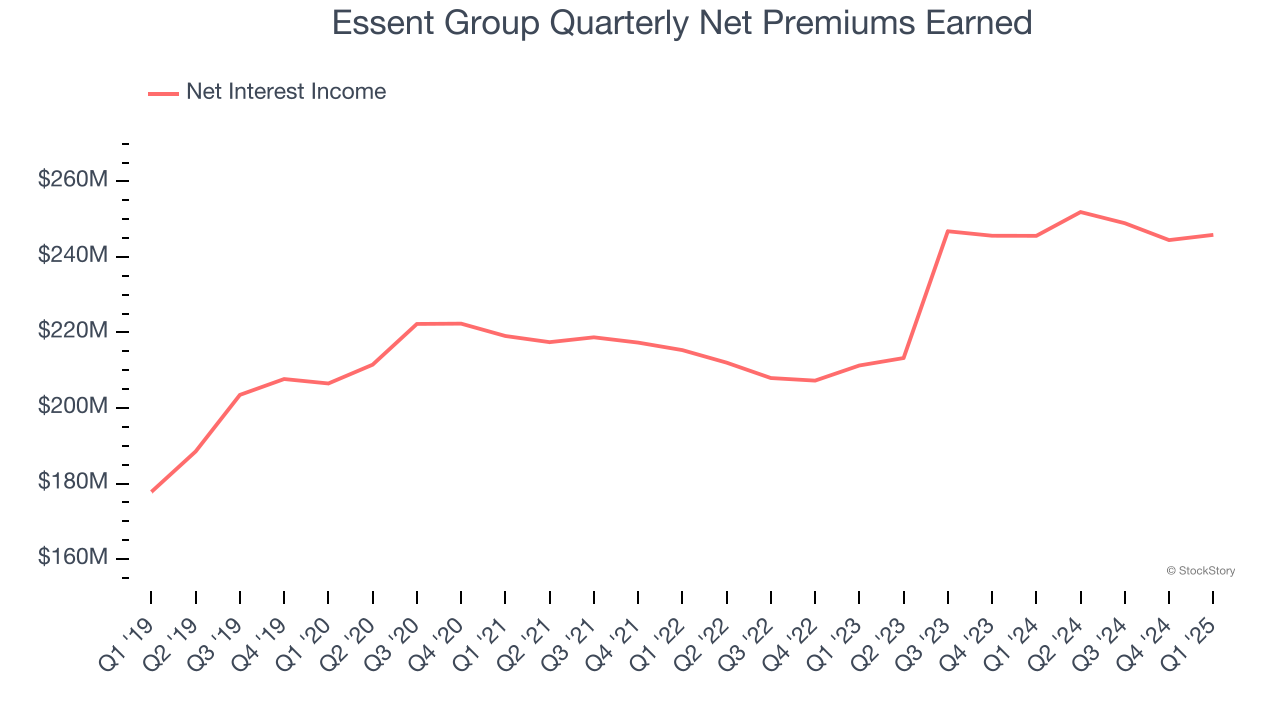

1. Net Premiums Earned Points to Soft Demand

While insurers generate revenue from multiple sources, investors view net premiums earned as the cornerstone - its direct link to core operations stands in sharp contrast to the unpredictability of investment returns and fees.

Essent Group’s net premiums earned has grown at a 4.2% annualized rate over the last five years, worse than the broader insurance industry and slower than its total revenue.

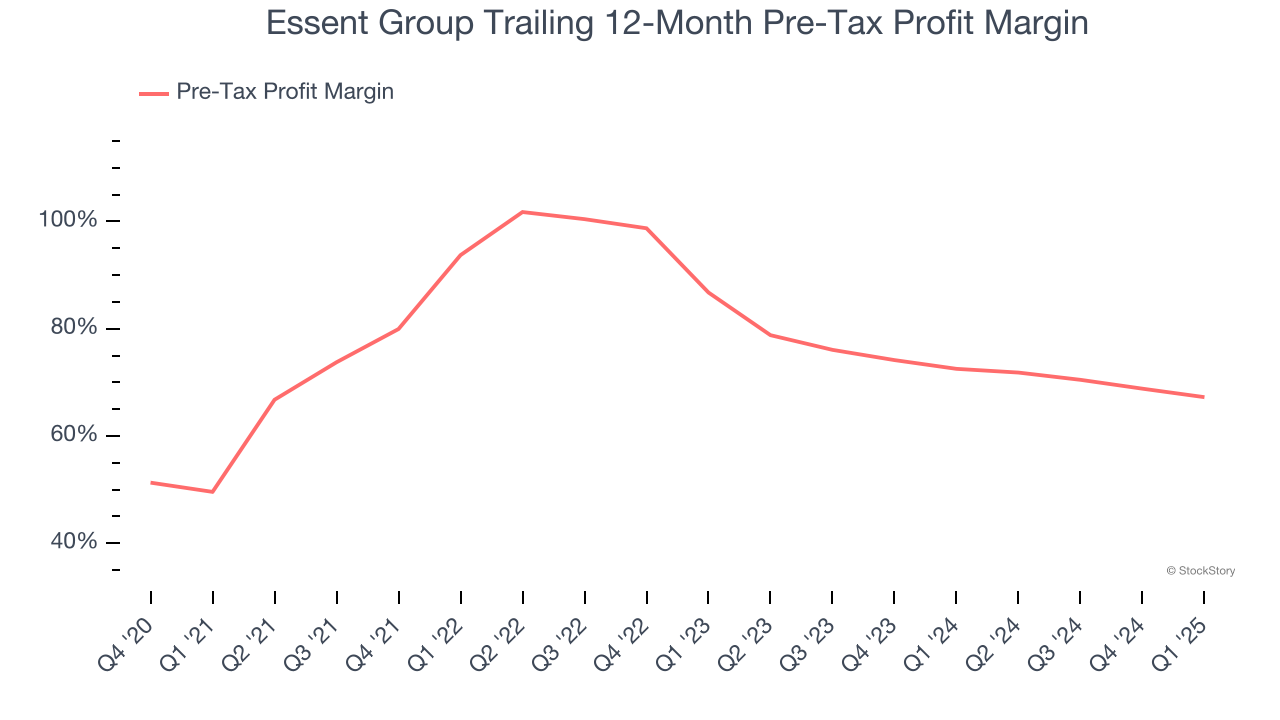

2. Deteriorating Pre-tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Insurance companies are balance sheet businesses, where assets and liabilities define the economics. Interest income and expense should therefore be factored into the definition of profit but taxes - which are largely out of a company’s control - should not. This is pre-tax profit by definition.

Over the last four years, Essent Group’s pre-tax profit margin has risen by 17.7 percentage points, clocking in at 67.2% for the past 12 months. Said differently, the company’s expenses have grown at a slower rate than revenue, which is always a positive sign.

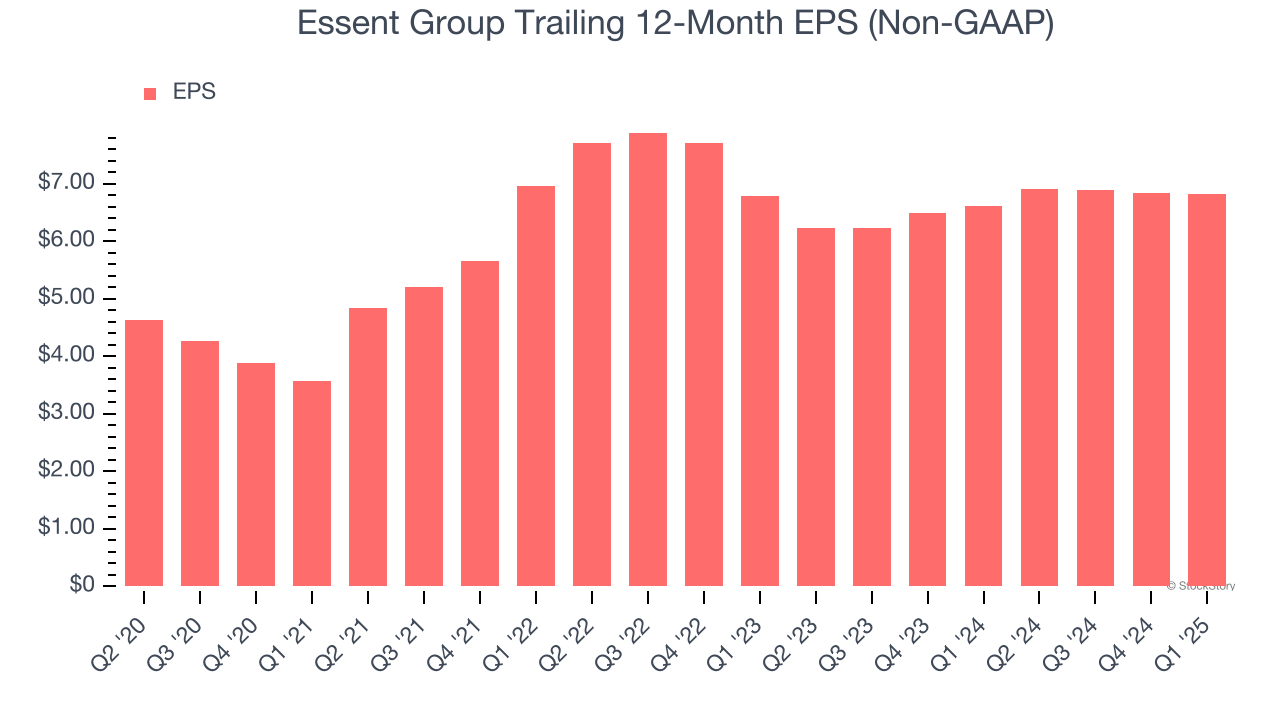

3. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Essent Group’s EPS grew at a weak 1.9% compounded annual growth rate over the last five years, lower than its 7.1% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Essent Group’s business quality ultimately falls short of our standards. With its shares trailing the market in recent months, the stock trades at 0.9× forward P/B (or $56.54 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now. Let us point you toward our favorite semiconductor picks and shovels play.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2024 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.