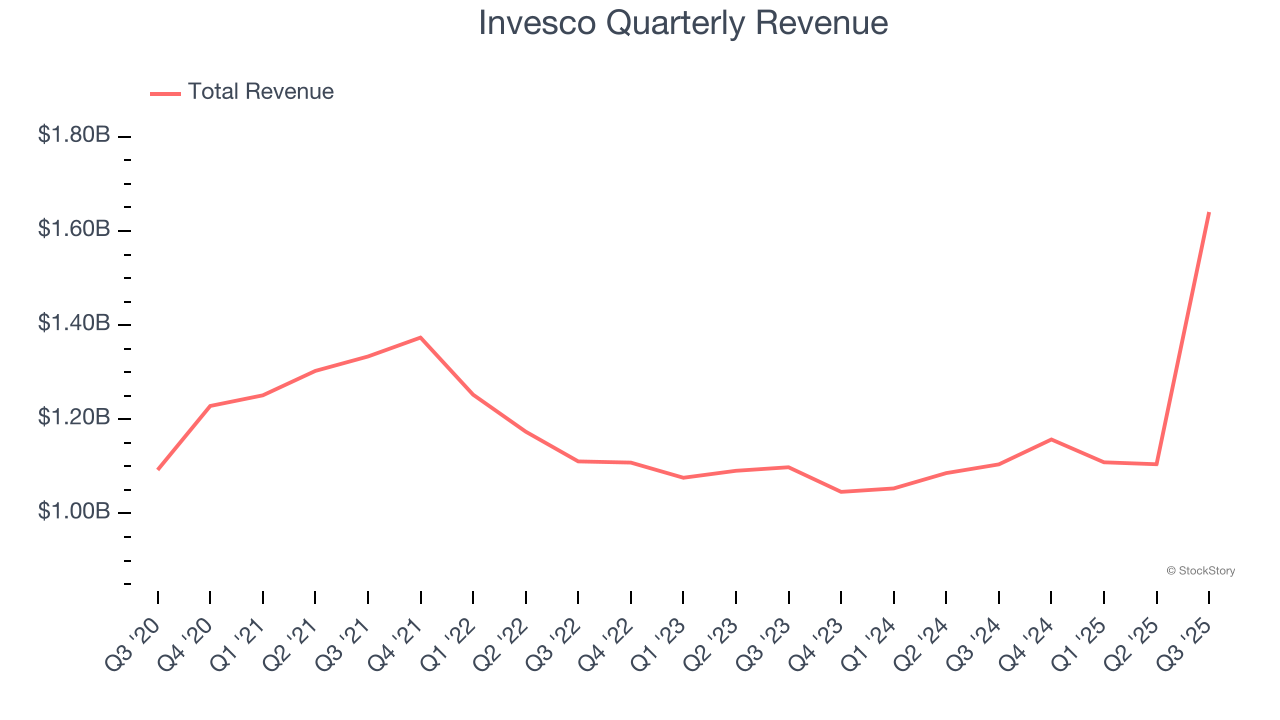

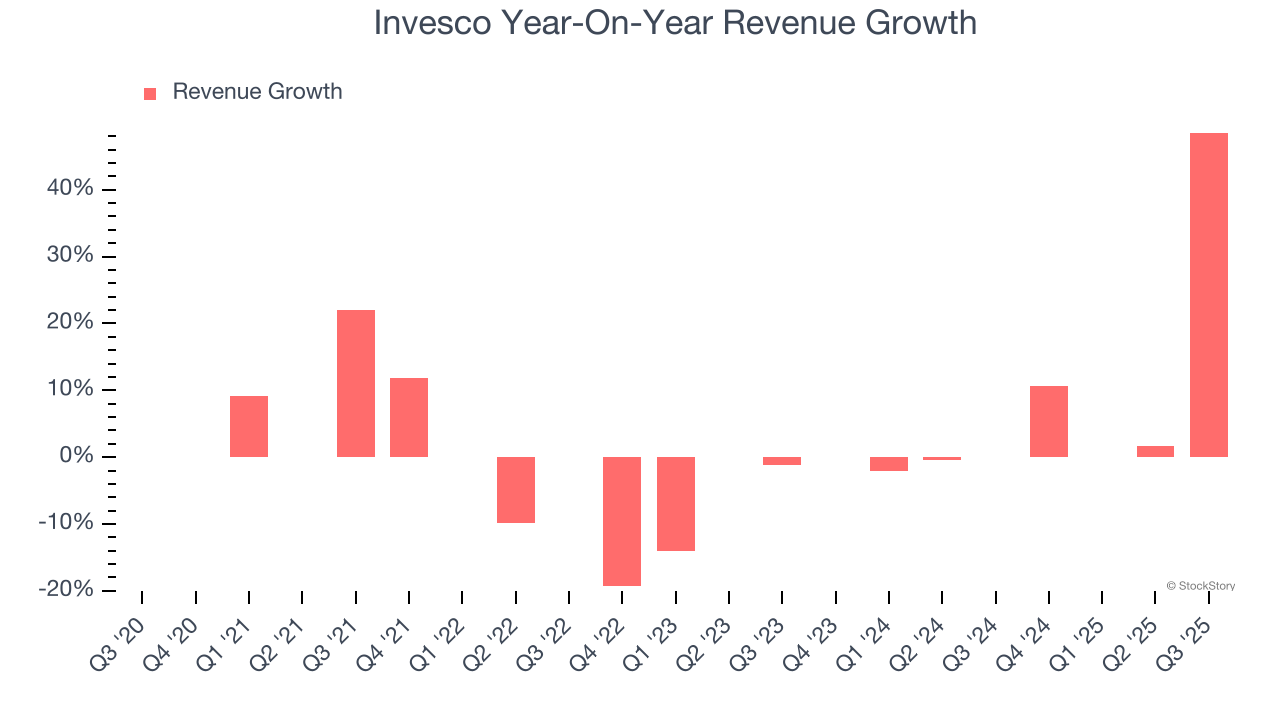

Asset management firm Invesco (NYSE: IVZ) reported Q3 CY2025 results topping the market’s revenue expectations, with sales up 48.5% year on year to $1.64 billion. Its non-GAAP profit of $0.61 per share was 39% above analysts’ consensus estimates.

Is now the time to buy Invesco? Find out by accessing our full research report, it’s free for active Edge members.

Invesco (IVZ) Q3 CY2025 Highlights:

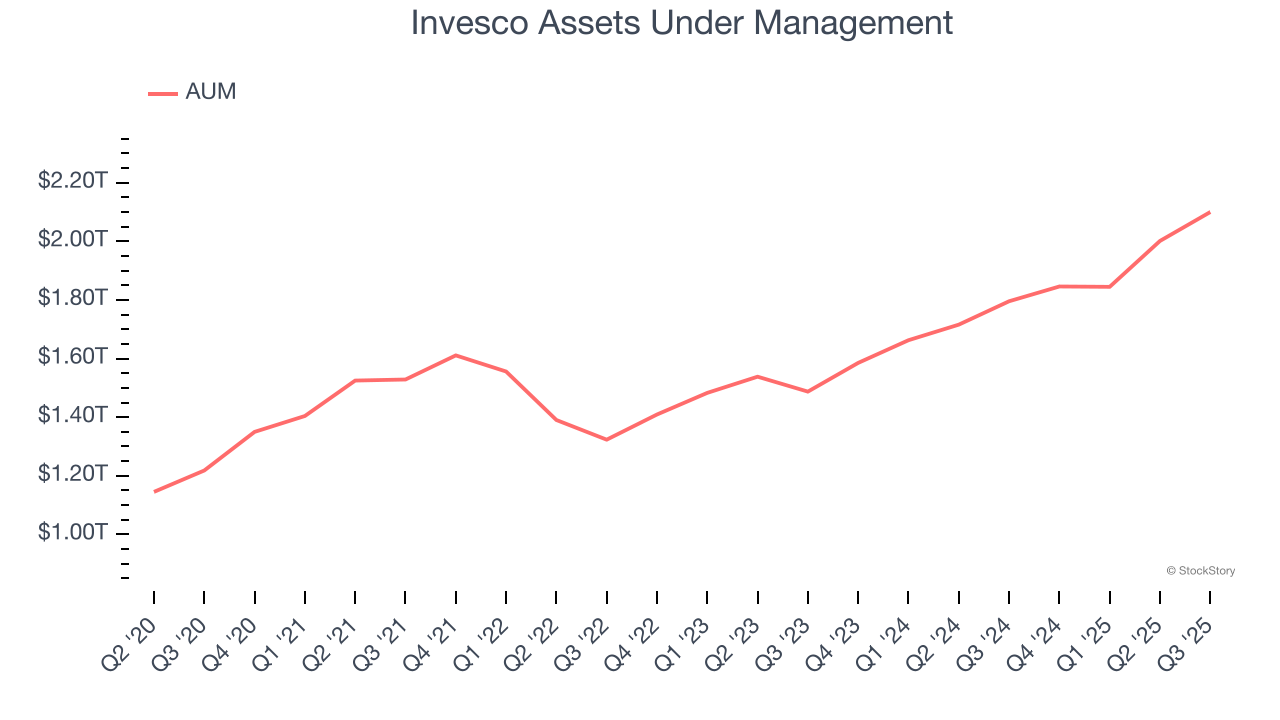

- Assets Under Management: $2.1 trillion vs analyst estimates of $1.81 trillion (17% year-on-year growth, 16.3% beat)

- Revenue: $1.64 billion vs analyst estimates of $1.18 billion (48.5% year-on-year growth, 38.8% beat)

- Pre-tax Profit: $346.7 million (21.1% margin, 139% year-on-year growth)

- Adjusted EPS: $0.61 vs analyst estimates of $0.44 (39% beat)

- Market Capitalization: $10.46 billion

Company Overview

With roots dating back to 1935 when it pioneered the first mutual fund with an objective of capital growth, Invesco (NYSE: IVZ) is a global asset management firm that offers investment solutions across equities, fixed income, alternatives, and multi-asset strategies.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Invesco’s revenue grew at a sluggish 2% compounded annual growth rate over the last five years. This was below our standards and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Invesco’s annualized revenue growth of 7% over the last two years is above its five-year trend, but we were still disappointed by the results.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Invesco reported magnificent year-on-year revenue growth of 48.5%, and its $1.64 billion of revenue beat Wall Street’s estimates by 38.8%.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Assets Under Management (AUM)

Assets Under Management (AUM) encompasses all client funds under a firm's investment management umbrella. The recurring fee structure on these assets provides consistent revenue generation, offering financial stability even during periods of poor investment returns, though sustained underperformance can impact future asset flows.

Invesco’s AUM has grown at an annual rate of 7.6% over the last four years, slightly better than the broader financials industry. When analyzing Invesco’s AUM over the last two years, we can see that growth accelerated to 14.8% annually. Fundraising or short-term investment performance were net contributors for the company over this shorter period since assets grew faster than total revenue. That said, assets aren't the be-all and end-all due to their unpredictable and cyclical nature.

Invesco’s AUM punched in at $2.1 trillion this quarter, beating analysts’ expectations by 16.3%. This print was 17% higher than the same quarter last year.

Key Takeaways from Invesco’s Q3 Results

It was good to see Invesco beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 4.8% to $24.60 immediately following the results.

Invesco had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.