Nio (NIO) is heading into one of its most important earnings reports in years. The China-based electric vehicle maker is set to release first-quarter 2026 results on Thursday, May 21, before U.S. markets open, and investors will be watching closely to see whether the company can turn strong delivery growth into a more durable financial recovery.

The report comes at a time when Nio is trying to prove that its strategy still has room to work. The company has spent years building around a battery-swapping model that sets it apart from many other EV makers, while also expanding into a three-brand lineup that now includes Nio, Onvo, and Firefly. That mix gives the company exposure to premium SUVs, mass-market family vehicles and smaller urban cars, but it also raises the bar for execution.

Nio has already shown that demand can be strong. The company said it delivered 83,465 vehicles in the first quarter, well above the top end of its own guidance. That kind of volume matters because it suggests the brand portfolio is gaining traction and that the new models are finding buyers in a highly competitive market.

The Stock Has Already Been Through a Sharp Swing

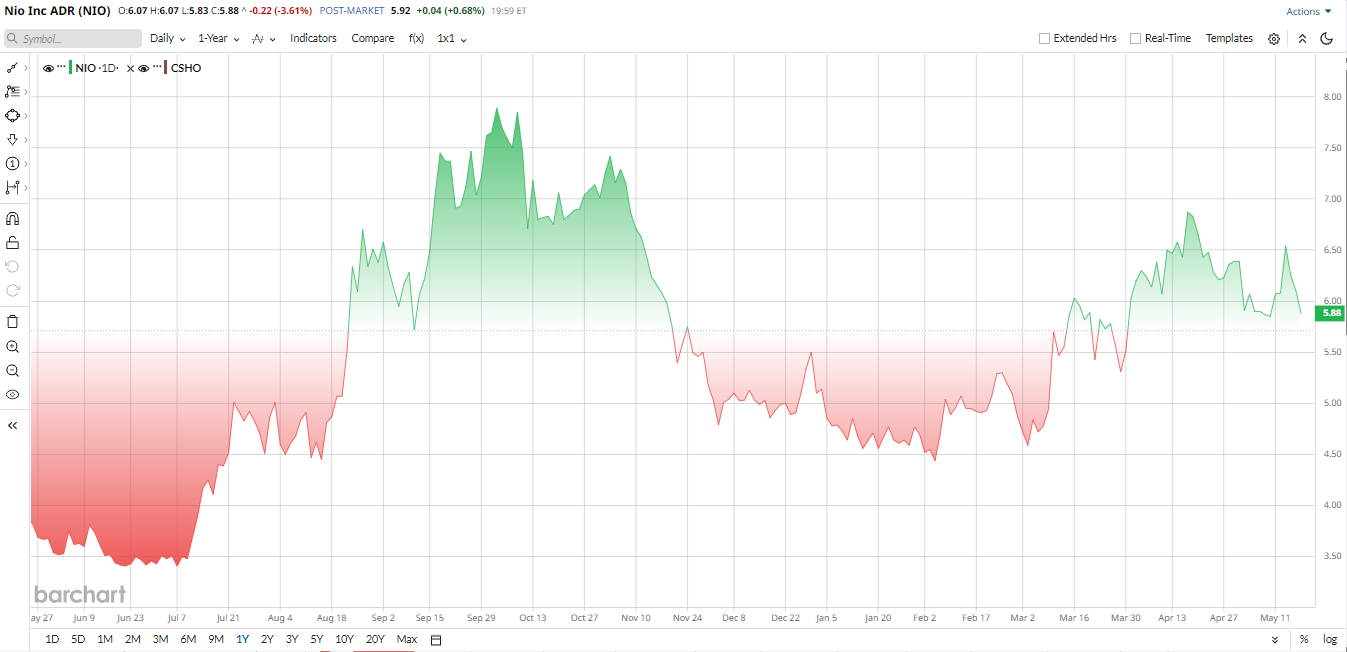

The market has not been waiting for the earnings report quietly. Nio shares have gained roughly 13% year-to-date, but that gain has been uneven. The stock surged sharply in March after the company reported its first-ever quarterly net profit in the fourth quarter of 2025, a milestone that briefly changed the tone around the name.

At the same time, the shares have also pulled back nearly 16% over the past month as some investors locked in gains ahead of the report. That kind of move is not unusual for Nio, which has long been one of the more volatile names in the EV space. The stock’s history suggests that sentiment can shift fast when investors get a fresh read on deliveries, margins, or guidance.

Valuation Leaves Room for Both Optimism and Caution

Nio’s valuation continues to divide investors. On one hand, the stock trades at about 0.9 times forward sales, which looks inexpensive compared with many growth stocks and even some auto peers. That lower sales multiple suggests the market is still skeptical about how much of Nio’s growth can be converted into lasting earnings power.

On the other hand, the company’s price-to-book ratio is above 22x, which shows that the market is still assigning significant value to the turnaround story. That is a high bar for a company that has yet to prove it can consistently generate profits.

What to Expect from the Upcoming Report

For the first quarter, Wall Street is looking for revenue of about $3.78 billion, which would mark a 109% increase from a year earlier. That is a sharp top-line jump and would reinforce the idea that Nio’s delivery momentum is real.

Even so, the market is not expecting the company to stay in the black just yet. Analysts are looking for a net loss of about $0.24 per share, suggesting that the fourth-quarter profit was not enough to signal a full turnaround. In other words, Nio is expected to show strong sales growth, but the financial picture may still be uneven.

Gross margin will be another important number. Citi has projected a first-quarter margin of 17.9%, helped by strong vehicle volume and a sales mix tilted toward higher-priced SUVs. If Nio can deliver that type of margin result, it would support the case that scale and product mix are beginning to work in its favor.

Management’s guidance also matters. The company previously pointed to first-quarter revenue of $3.5 billion to $3.6 billion, which was already above earlier market expectations. That means investors will not just be looking for a beat. They will also want to know whether the company sees continued momentum in the second quarter.

Analysts Remain Cautious, but Constructive

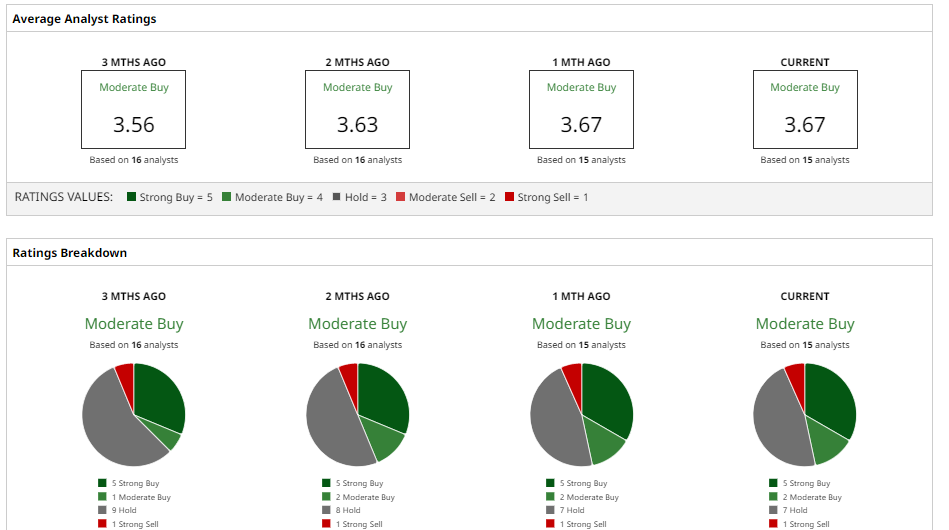

Opinion on Nio is still mixed. Of the 17 analysts covering the stock, five rate it “Strong Buy,” two “Moderate Buy,” seven rate it “Hold,” and only one rate it “Strong Sell,” which suggests the Street is not fully aligned on the pace of the recovery.

The average 12-month price target is about $6.60, indicating that many analysts see around 14% upside if the company keeps improving deliveries and margins.

Morgan Stanley has pointed to the ramp-up of Onvo models as a key driver, while DBS has argued that new products and better profitability could support a re-rating. Bank of America, meanwhile, has remained more cautious, saying the valuation already reflects much of the good news.

That split captures the investment case well. Nio has already shown it can grow fast. The real test now is whether it can do that while moving closer to consistent profitability.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- IBM Stock Leads Mega-Cap Stock Decliners as Market Volatility Triggers Steep Selloff. That Doesn’t Tell You the Whole Story.

- Ahead of Walmart Earnings, Here Is What Barchart Options Data Shows for WMT Stock

- Citi Just Raised Its Price Target on Sandisk Stock by 50%. Here's Why.

- Cerebras Stock Staged an Explosive IPO. Investors Now Are Betting on 1.5% of Nvidia and AMD’s Combined Market Value for a Chance at Riches.