Oracle Corporation’s (ORCL) latest leadership shake-up adds a new variable to an already changing investment story. Oracle has appointed Hilary Maxson as Chief Financial Officer, effective April 6, bringing in a seasoned finance executive who served as Executive VP and group CFO in Schneider Electric (SBGSY) at a time when the company is dramatically ramping spending on artificial intelligence (AI) and cloud infrastructure.

Importantly, Maxson replaces Doug Kehring, who had been serving as principal financial officer and will now shift back to operations.

The timing is critical. Oracle is in the midst of a capital-intensive pivot, pouring tens of billions into AI infrastructure, while facing rising debt, pressured free cash flow, and ongoing restructuring. The decision to reinstall a dedicated CFO signals a shift toward tighter financial oversight just as execution risk is climbing.

Does fresh financial leadership improve execution enough to justify buying the stock here?

About Oracle Stock

Best known for its pioneering relational database software and enterprise tools, Oracle has evolved into a powerhouse in cloud infrastructure, SaaS applications, hardware systems, and consulting services. Headquartered in Austin, Texas, the firm serves a global client base, and with a market cap of $418.6 billion, the company ranks among the world’s top software and cloud computing firms.

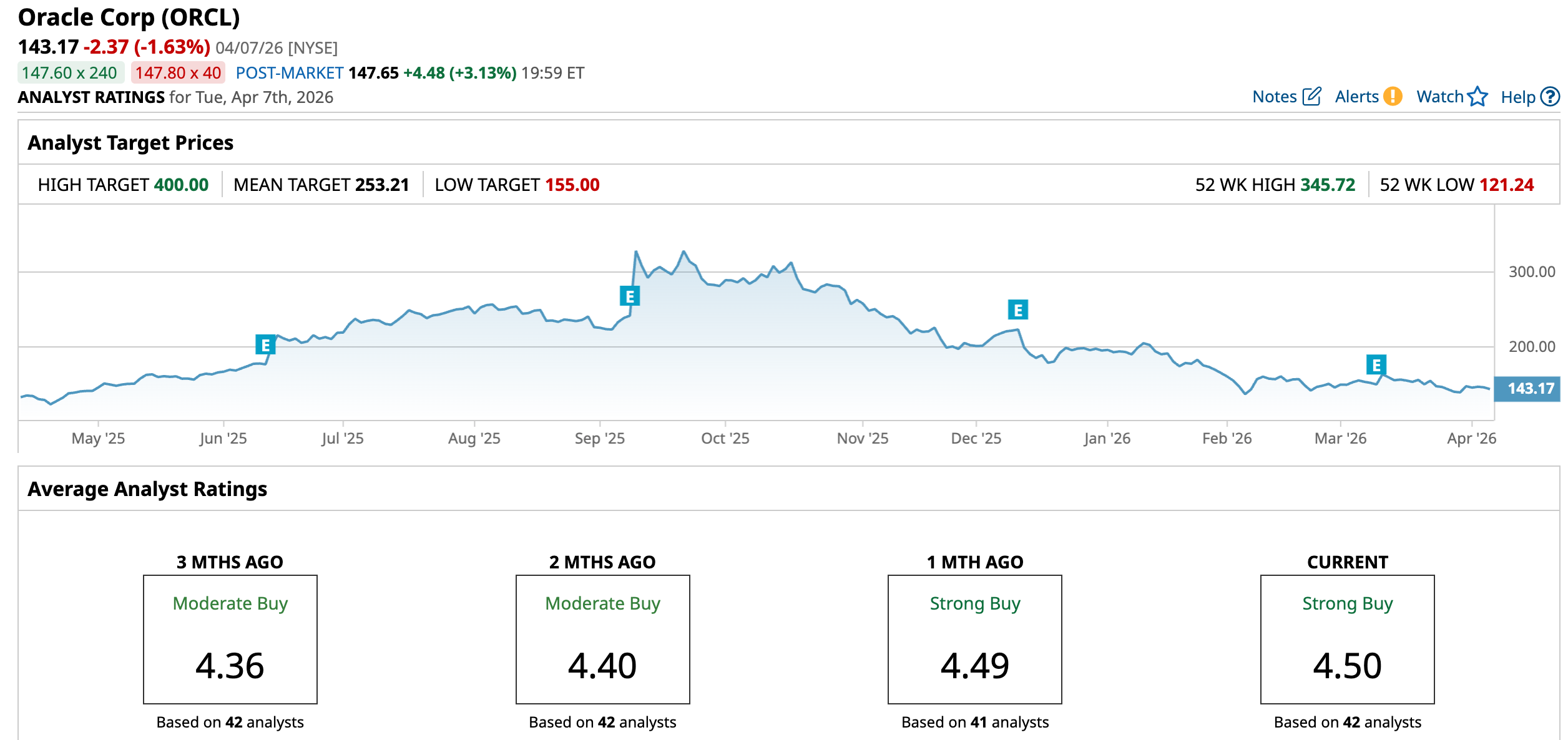

Oracle stock has exhibited gains driven by AI enthusiasm, followed by a sharp correction in 2026 as fundamentals and expectations reset. Over the past year, the stock is still up around 12.59%.

The stock rallied in 2025, fueled by a combination of accelerating Oracle Cloud Infrastructure demand, large enterprise deal wins, and a broader narrative shift that repositioned Oracle from a legacy database vendor to a credible AI infrastructure player. This surge pushed Oracle to a 52-week high of $345.72 on Sept. 10, implying a dramatic expansion in valuation multiples as investors priced in long-term growth tied to AI adoption and hyperscale cloud competition.

However, this optimism has been sharply tempered in 2026. Year-to-date (YTD), Oracle shares are down 26.55%, reflecting a significant pullback as the market reassesses both execution risks and the near-term financial impact of the company’s strategy. The decline has been driven primarily by rising capital intensity, as Oracle commits tens of billions of dollars toward data centers and AI infrastructure, and has announced layoffs.

Moreover, investors have become more cautious about Oracle’s ability to compete at scale with hyperscalers, leading to valuation compression after an extended rally.

In addition, the market reaction to Oracle's CFO appointment was notably muted, after the firm announced the appointment of Hilary Maxson as CFO on April 6.

The stock is currently trading at a discount compared to peers and its own historical average at 24.12 times forward earnings.

Q3 Results Demonstrate Cloud Momentum

Oracle Corporation reported its fiscal third-quarter 2026 results on March 10, after the market closed.

The company delivered a strong top-line performance, with revenue of $17.2 billion, up 22% year-over-year (YOY). This marked a clear acceleration in growth, driven primarily by robust demand for cloud and AI-related infrastructure. Cloud revenue reached roughly $8.9 billion, increasing 44% YOY, underscoring the central role of Oracle Cloud Infrastructure in the company’s growth narrative.

Profitability metrics also showed meaningful improvement. Oracle reported non-GAAP earnings per share of $1.79, up about 21% from the prior-year quarter and above the consensus estimate. Net income increased to around $3.7 billion, reflecting solid operating leverage even as the company continues to invest heavily in AI data center capacity.

Notably, this was one of the rare quarters where both revenue and adjusted earnings grew above 20%, highlighting a step-change in Oracle’s growth profile.

The most striking metric in the quarter was Oracle’s Remaining Performance Obligations (RPO), which surged to $553 billion, up 325% YOY, supported by large multi-year AI infrastructure deals. This provided strong visibility into future revenue streams and reinforced management’s confidence in sustained growth driven by enterprise AI adoption.

Furthermore, Oracle issued guidance for the fourth quarter, projecting revenue growth of roughly 18% to 20% YOY and adjusted EPS in the range of $1.92 to $1.96. The company also maintained its fiscal 2026 revenue outlook of $67 billion, while raising its longer-term fiscal 2027 revenue target to around $90 billion, signaling confidence in continued momentum from AI-driven demand.

Analysts remain optimistic as they predict EPS to be around $6.07 for fiscal 2026, up 38% YOY, and surge by another 3.6% annually to $6.29 in fiscal 2027.

What Do Analysts Expect for Oracle Stock?

Most recently, Oracle Corporation received a vote of confidence from Mizuho, which reiterated an “Outperform” rating and $320 price target following the company’s announcement of a new chief financial officer.

Also, Oracle remains rated “Outperform” by Bernstein SocGen Group with a $319 price target, citing solid Q3 results.

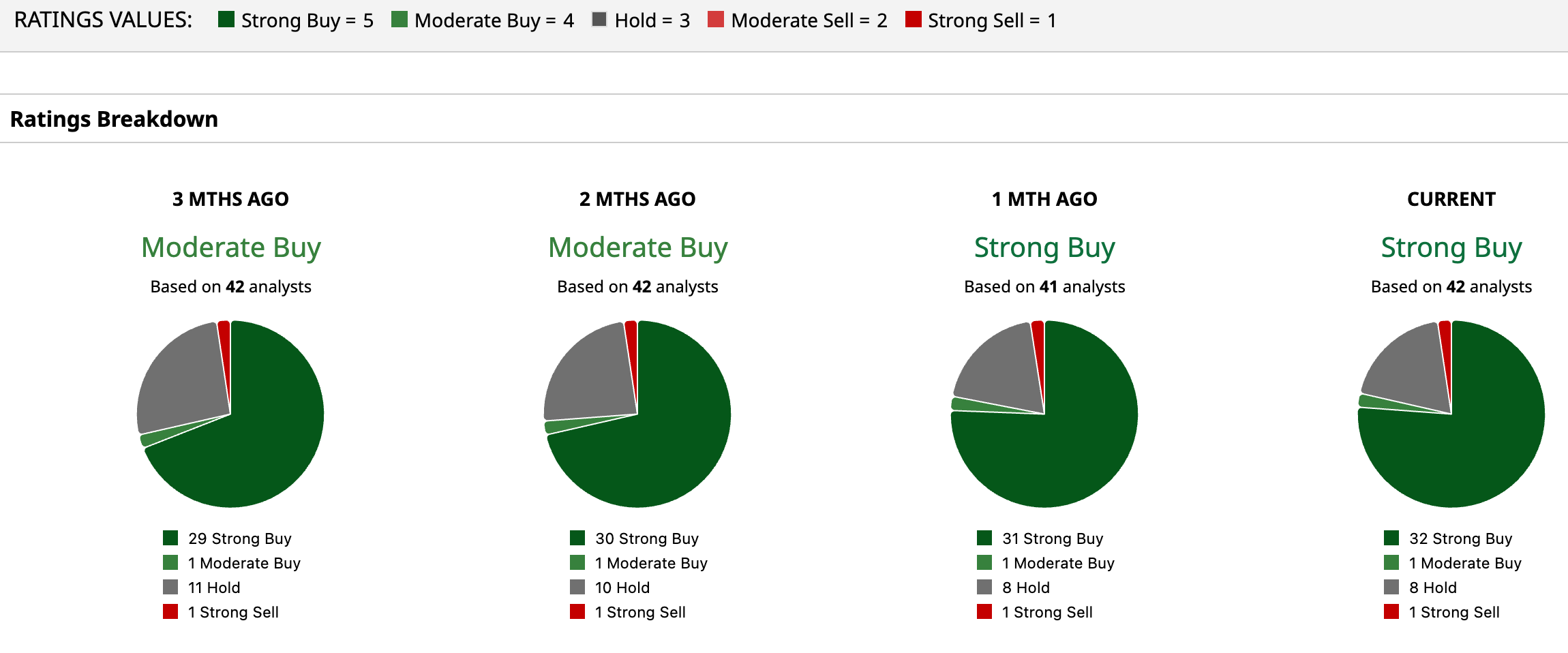

Oracle stock has a consensus “Strong Buy” rating overall. Among the 42 analysts covering the tech stock, 32 recommend a “Strong Buy,” one gives a “Moderate Buy,” eight analysts stay cautious with a “Hold” rating, and one gives a “Strong Sell” rating.

While its average price target of $253.21 indicates an upside of 76.9%, the Street-high target price of $400 suggests that the stock could rally as much as 179.39%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart