With a market cap of $15.4 billion, Huntington Ingalls Industries, Inc. (HII) is a prominent defense company that designs, builds, overhauls, and repairs military ships, including nuclear-powered aircraft carriers and submarines for the U.S. Navy and Coast Guard. The Newport News, Virginia-based company also provides advanced mission technologies, such as C5ISR systems, cybersecurity, artificial intelligence, and fleet sustainment solutions.

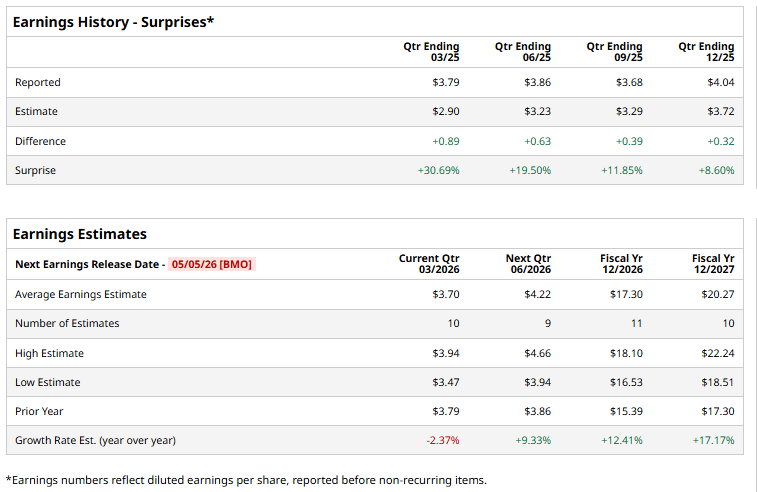

The company is expected to release its Q1 2026 results before the market opens on Tuesday, May 5. Ahead of the event, analysts anticipate Huntington Ingalls to report a profit of $3.70 per share, down 2.4% from $3.79 per share in the year-ago quarter. It has exceeded Wall Street's earnings expectations in each of the past four quarters.

For fiscal 2026, analysts expect HII to report EPS of $17.30, a rise of nearly 12.4% from $15.39 in fiscal 2025. Moreover, EPS is anticipated to grow 17.2% year over year to $20.27 in fiscal 2027.

HII stock has surged 78.7% over the past 52 weeks, outpacing both the S&P 500 Index’s ($SPX) 34.6% rise and the State Street Industrial Select Sector SPDR ETF’s (XLI) 38.8% return during the same time frame.

Huntington Ingalls has outpaced the broader market over the past year primarily due to its defensive, government-backed business model and strong demand for naval capabilities amid rising geopolitical tensions. Increased U.S. defense spending, particularly on fleet modernization, submarines, and aircraft carriers, has supported a robust multi-year backlog and revenue visibility, insulating the company from broader economic volatility.

Additionally, HII has benefited from improved execution, margin stability, and growth in its Mission Technologies segment, which is expanding into higher-margin areas such as cyber, AI, and defense IT services. This combination of stable cash flows, strategic importance to national security, and gradual diversification has strengthened investor confidence, enabling the stock to outperform the broader market.

Analysts’ consensus opinion on the stock is cautiously optimistic, with a “Moderate Buy” rating overall. Among the 13 analysts covering the stock, five are recommending a “Strong Buy,” and eight recommend a “Hold.” While the stock currently trades above the average analyst price target of $391.55, the Street high price target of $460 implies an upswing potential of 17.3% from the current market prices.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Will Q1 Earnings Power GE Vernova Stock to $1,225?

- PayPal Stock Is Down More Than 80% Over the Past 5 Years. Michael Burry Is Buying the Dip.

- Is Microsoft Stock a Buy Before Q3? Cloud and AI Trends Point to Strong Growth

- Nuclear Startup Fermi Just Lost Its CEO and COO in a Shocking Move. Should You Buy the Dip in FRMI Stock Today or Stay Far, Far Away?