Oracle (ORCL) will release its third-quarter fiscal year 2026 results today after the market closes. Notably, ORCL stock has suffered a dramatic correction in recent months. Shares have fallen more than 55% from their 52-week high of $345.72, erasing any artificial intelligence (AI)-driven gains.

The steep decline reflects growing investor unease over several issues, including Oracle’s aggressive capital spending on AI and cloud, customer concentration risk, and uncertainty about how the company plans to finance the massive infrastructure investments required to support rising demand.

Despite those concerns, the company’s business momentum remains solid. The Oracle Cloud Infrastructure (OCI) segment is witnessing a surge in AI workloads. In particular, demand tied to graphics processing units (GPUs) has been a key contributor, as enterprises increasingly deploy AI applications that require significant computing power. This could provide a meaningful boost to Oracle’s top line.

Further, due to the selloff, Oracle’s 14-period relative strength index (RSI) currently sits around 46, well below the 70 level that typically signals overbought conditions. This suggests that the stock has room to run following the earnings release.

Options markets are pricing in a potential move of about 10.4% in either direction for contracts expiring on March 13. That implied volatility is lower than Oracle’s average post-earnings move of roughly 16.1% over the past four quarters, suggesting traders anticipate a more moderate reaction this time around.

Historically, Oracle’s earnings announcements have produced mixed responses from investors. The stock has declined following two of its last four earnings releases.

Oracle's Q3 Expectations

While Oracle stock has dropped significantly, expectations remain high for another solid quarter from the company as it continues to benefit from accelerating demand for cloud and AI infrastructure.

Notably, in Q2, Oracle’s cloud business accounted for roughly half of its total revenue. Within that segment, Oracle Cloud Infrastructure (OCI) delivered strong results. Infrastructure revenue totaled $4.1 billion, up 66% year-over-year. Demand for AI-related computing power was a key driver, with GPU-related revenue surging 177%.

Another indicator of Oracle’s growing momentum is its massive backlog of contracted business. Remaining performance obligations (RPO) reached $523.3 billion by the end of the last quarter. That figure represents a 433% increase from a year earlier and a $68 billion increase since August alone. Major deals with technology leaders such as Meta Platforms (META) and Nvidia (NVDA) have played a significant role in building this backlog as Oracle continues to diversify its enterprise customer base.

Looking ahead to the third quarter, AI is expected to remain a major catalyst for growth. Demand for AI infrastructure is surging across the industry, and Oracle’s cloud infrastructure platform is likely to deliver significant growth.

The company is also seeing increasing demand for multicloud deployments. The strong expansion in multicloud consumption during the previous quarter is expected to continue into Q3.

Management’s guidance reflects the strong demand environment. Oracle expects total cloud revenue growth to accelerate from 37% to 41% on a constant-currency basis. Overall, company revenue is projected to increase between 16% and 18%. However, the rapid expansion of infrastructure capacity is likely to put some pressure on margins and free cash flow in the near term due to upfront investment costs.

Profitability is still expected to improve. ORCL’s adjusted earnings per share (EPS) is projected to grow between 12% and 14%, reaching a range of $1.64 to $1.68 in constant currency. Analysts are forecasting earnings of about $1.34 per share for the quarter, representing year-over-year growth of roughly 13.6%. Oracle has beaten analyst estimates in each of the past four quarters, including an impressive 51.2% earnings surprise in the previous quarter.

Is Oracle Stock a Buy Now?

With a rapidly expanding backlog, strong demand for OCI, and growing traction in multicloud deployments, Oracle appears well-positioned to deliver strong growth in Q3. Another important growth driver is the faster conversion of RPO into revenue. At the same time, the company is working to broaden its customer base and expand adoption across industries.

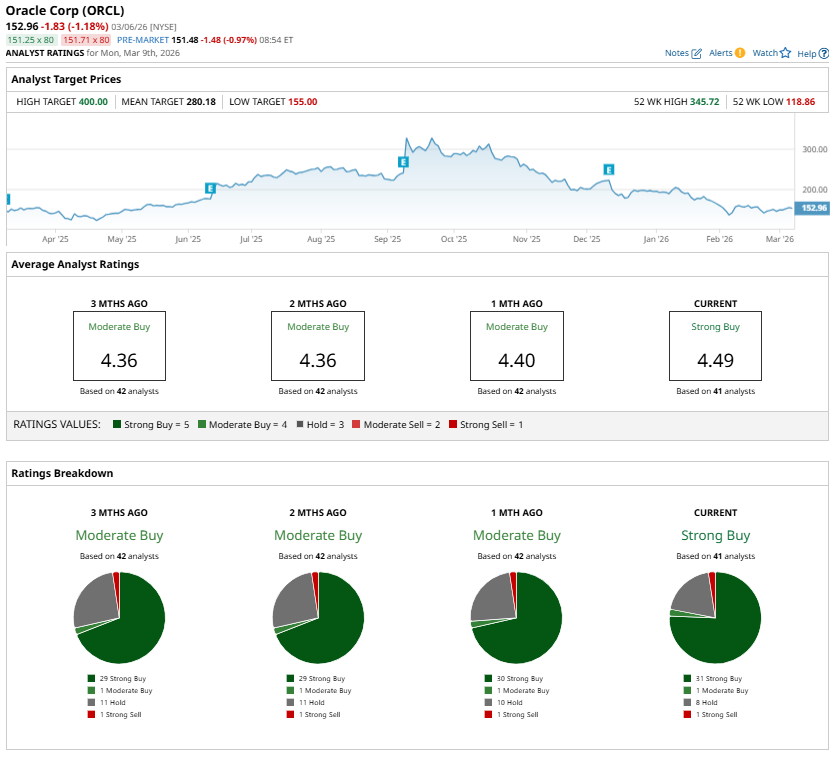

Further, the recent drop in Oracle’s share price has made the valuation more attractive compared with earlier levels. Many analysts remain optimistic about the company’s prospects and currently assign a “Strong Buy” consensus rating to the stock ahead of the Q3 earnings.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart