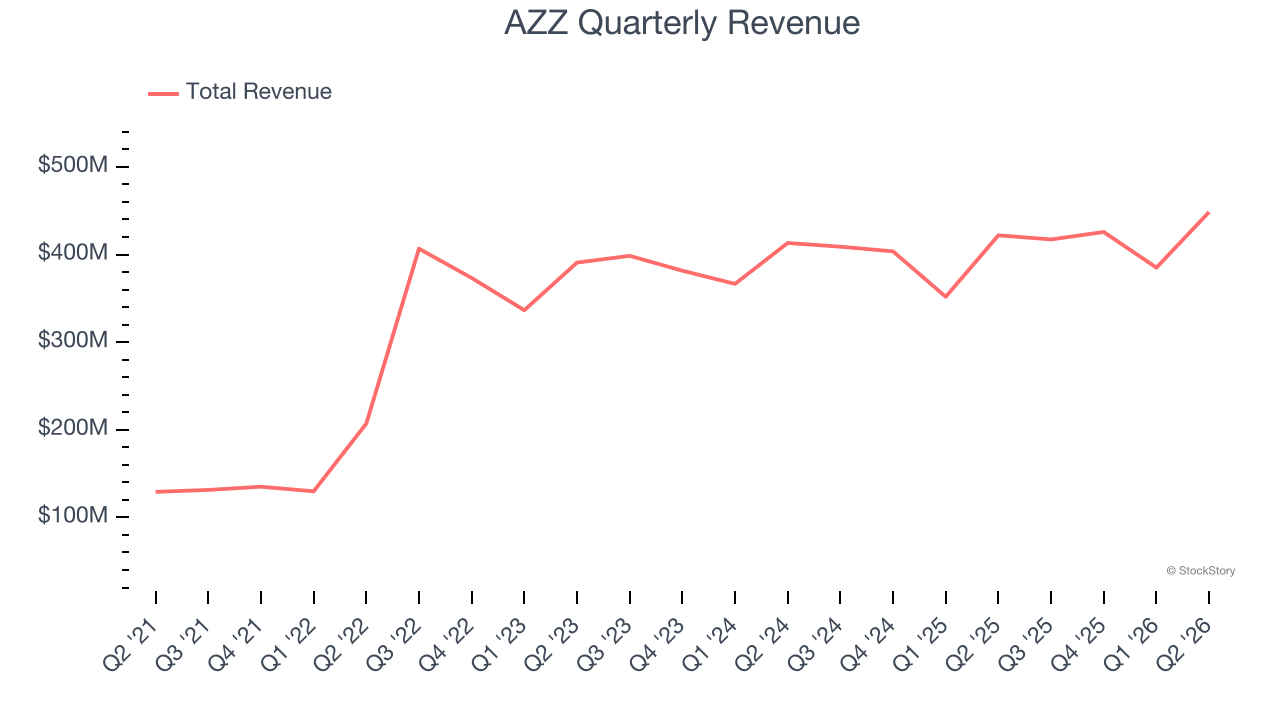

Metal coating and infrastructure solutions provider AZZ (NYSE: AZZ) reported Q2 CY2026 results topping the market’s revenue expectations, with sales up 6.3% year on year to $448.5 million. The company’s full-year revenue guidance of $1.83 billion at the midpoint came in 4.3% above analysts’ estimates. Its non-GAAP profit of $1.85 per share was 9.6% above analysts’ consensus estimates.

Is now the time to buy AZZ? Find out by accessing our full research report, it’s free.

AZZ (AZZ) Q2 CY2026 Highlights:

- Revenue: $448.5 million vs analyst estimates of $434.5 million (6.3% year-on-year growth, 3.2% beat)

- Adjusted EPS: $1.85 vs analyst estimates of $1.69 (9.6% beat)

- Adjusted EBITDA: $99.45 million vs analyst estimates of $97.06 million (22.2% margin, 2.5% beat)

- The company lifted its revenue guidance for the full year to $1.83 billion at the midpoint from $1.75 billion, a 4.3% increase

- Management raised its full-year Adjusted EPS guidance to $6.95 at the midpoint, a 3% increase

- EBITDA guidance for the full year is $395 million at the midpoint, above analyst estimates of $388.3 million

- Operating Margin: 17.2%, in line with the same quarter last year

- Market Capitalization: $4.49 billion

Tom Ferguson, President, and Chief Executive Officer of AZZ, commented, "We are off to a great start in the fiscal year as sales grew to $448.5 million, up 6.3% over the prior year quarter. Our sales momentum and disciplined operational execution resulted in Adjusted EBITDA of $99.5 million, or 22.2% of sales, which generated adjusted diluted EPS of $1.85, up 3.9%. Metal Coatings achieved strong, double-digit sales gains on higher volume of galvanized steel. Meanwhile, Precoat Metals reached record first-quarter sales, fueled by a combination of price increases to offset materials and input cost inflation and the ongoing production ramp-up at the Washington, Missouri facility. We are on track to set new sales and profitability records in fiscal year 2027 due to external market visibility as we continue to execute our strategic plans; therefore, we have increased our annual guidance range."

Company Overview

Responsible for projects like nuclear facilities, AZZ (NYSE: AZZ) is a provider of metal coating and power infrastructure solutions.

Revenue Growth

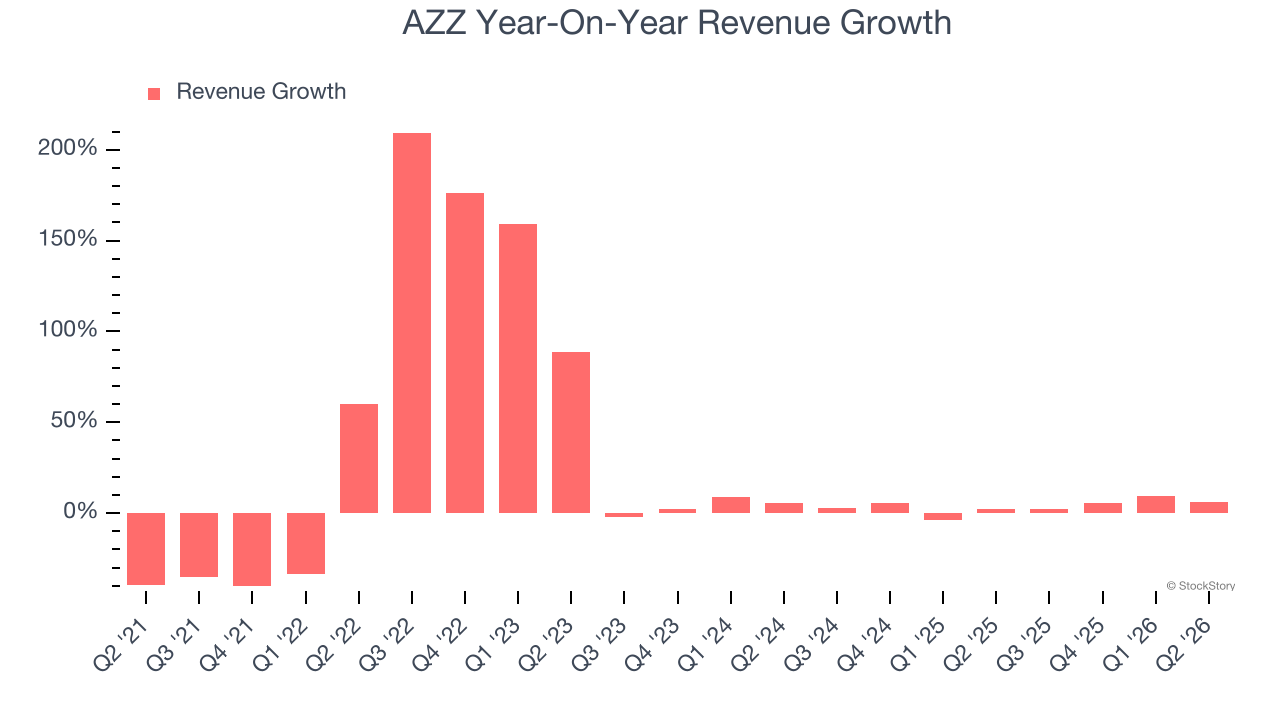

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, AZZ’s sales grew at an incredible 17.3% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. AZZ’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 3.7% over the last two years was well below its five-year trend.

This quarter, AZZ reported year-on-year revenue growth of 6.3%, and its $448.5 million of revenue exceeded Wall Street’s estimates by 3.2%.

Looking ahead, sell-side analysts expect revenue to grow 5.9% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector. At least the company is tracking well in other measures of financial health.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

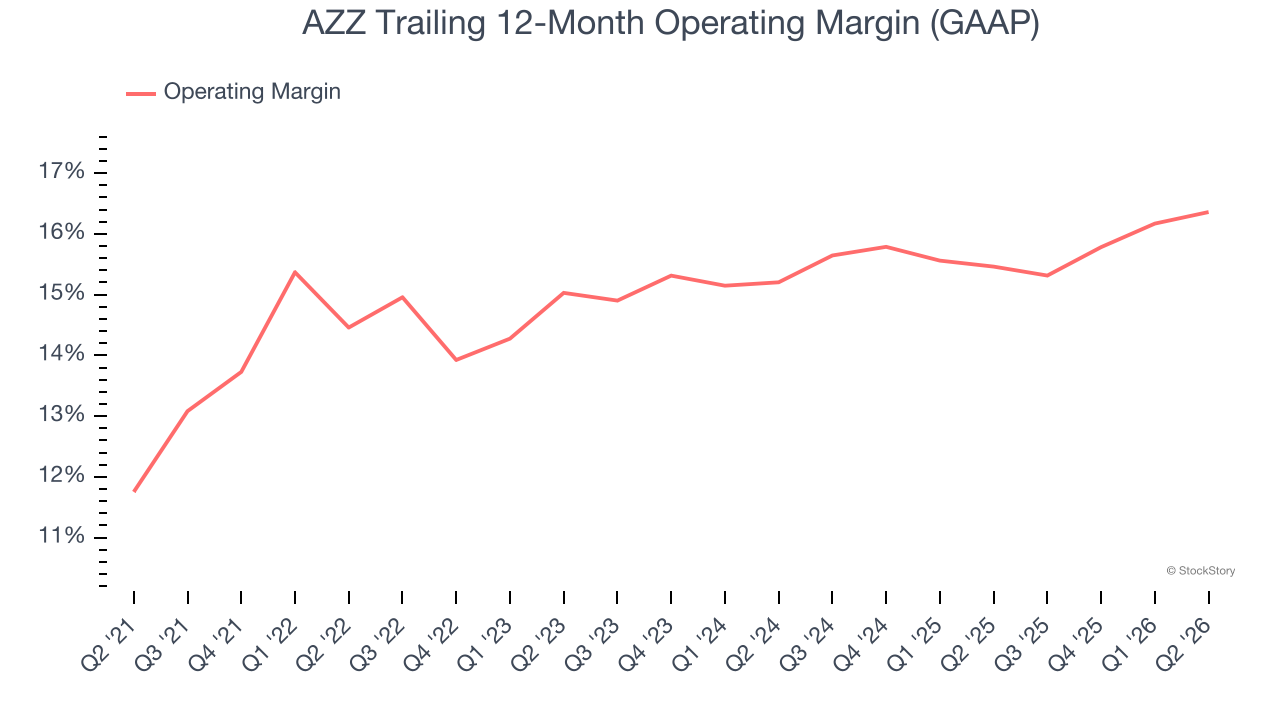

AZZ has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 15.4%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, AZZ’s operating margin rose by 1.9 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q2, AZZ generated an operating margin profit margin of 17.2%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

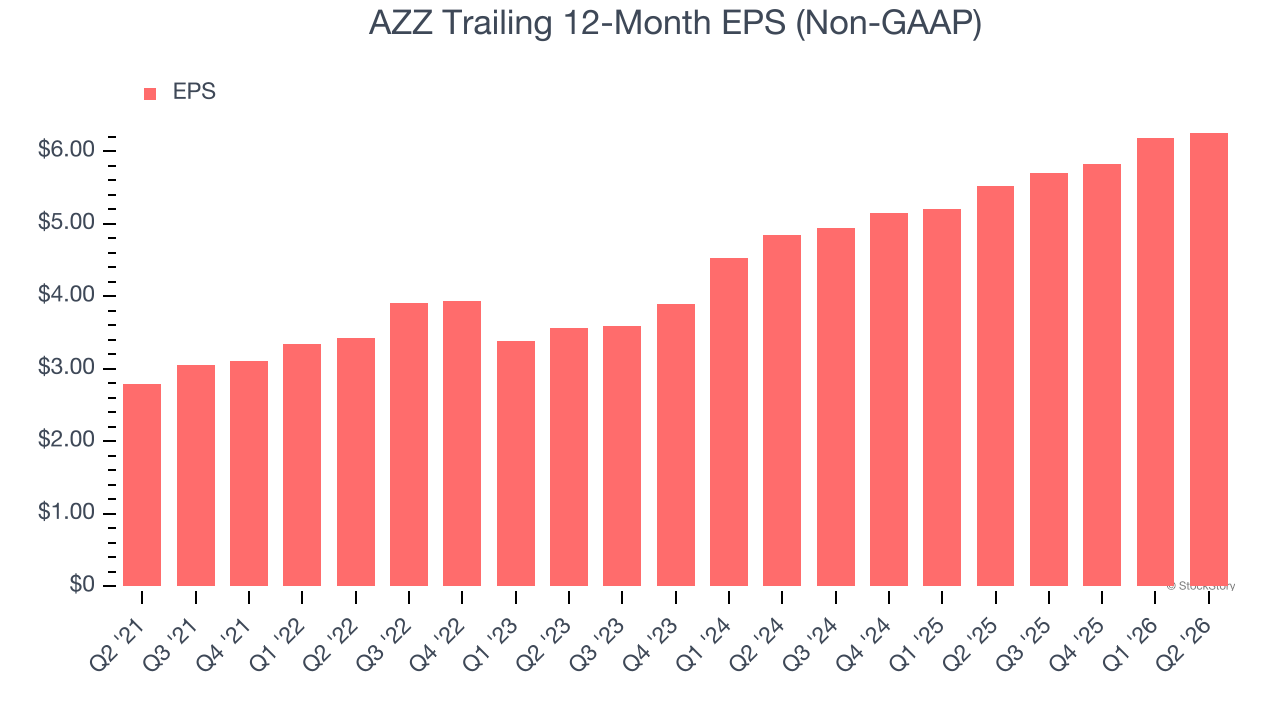

AZZ’s astounding 17.5% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For AZZ, its two-year annual EPS growth of 13.6% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q2, AZZ reported adjusted EPS of $1.85, up from $1.78 in the same quarter last year. This print beat analysts’ estimates by 9.6%. Over the next 12 months, Wall Street expects AZZ’s full-year EPS to grow 13.5% from $6.26 to $7.10.

Key Takeaways from AZZ’s Q2 Results

We were impressed by AZZ’s optimistic full-year revenue guidance, which blew past analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 7.4% to $154.18 immediately following the results.

AZZ put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).