Over the past six months, Hope Bancorp has been a great trade, beating the S&P 500 by 6.1%. Its stock price has climbed to $13.40, representing a healthy 14.3% increase. This performance may have investors wondering how to approach the situation.

Is now the time to buy Hope Bancorp, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Hope Bancorp Will Underperform?

Despite the momentum, we don’t have much confidence in Hope Bancorp. Here are three reasons you should be careful with HOPE, plus one stock we’d rather own.

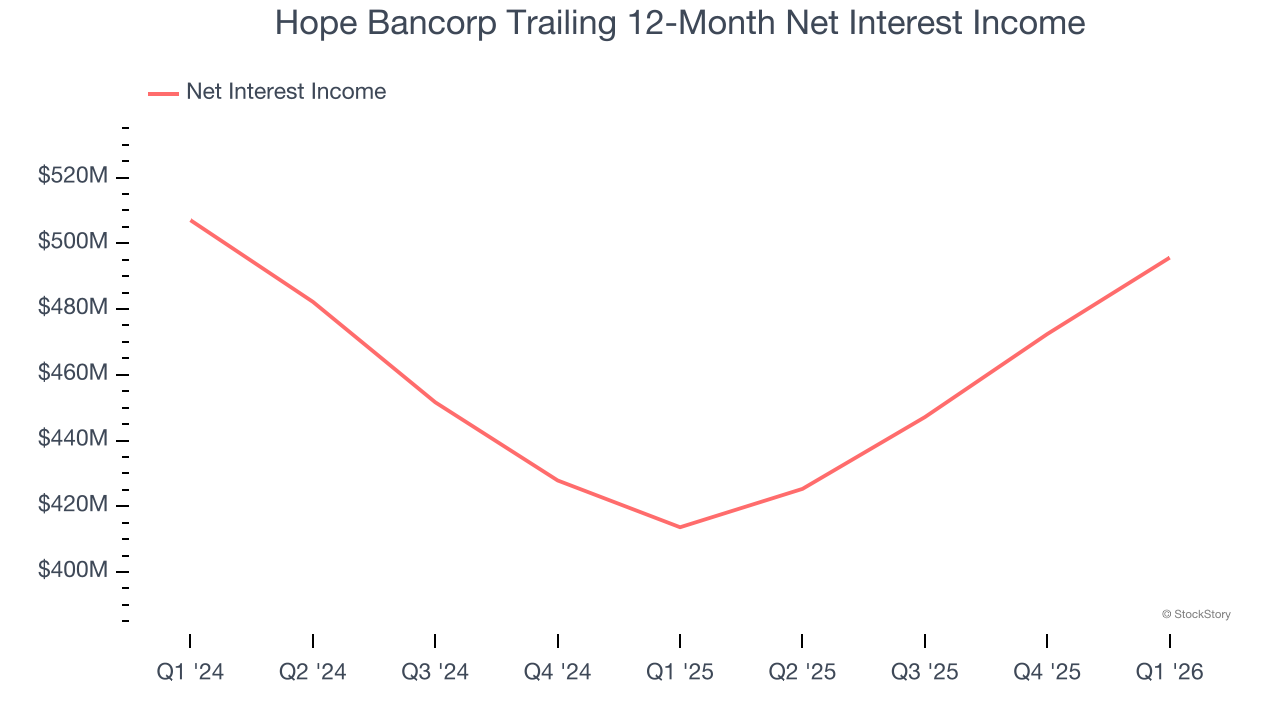

1. Net Interest Income Points to Soft Demand

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

Hope Bancorp’s net interest income has grown at a 1% annualized rate over the last five years, much worse than the broader banking industry and in line with its total revenue.

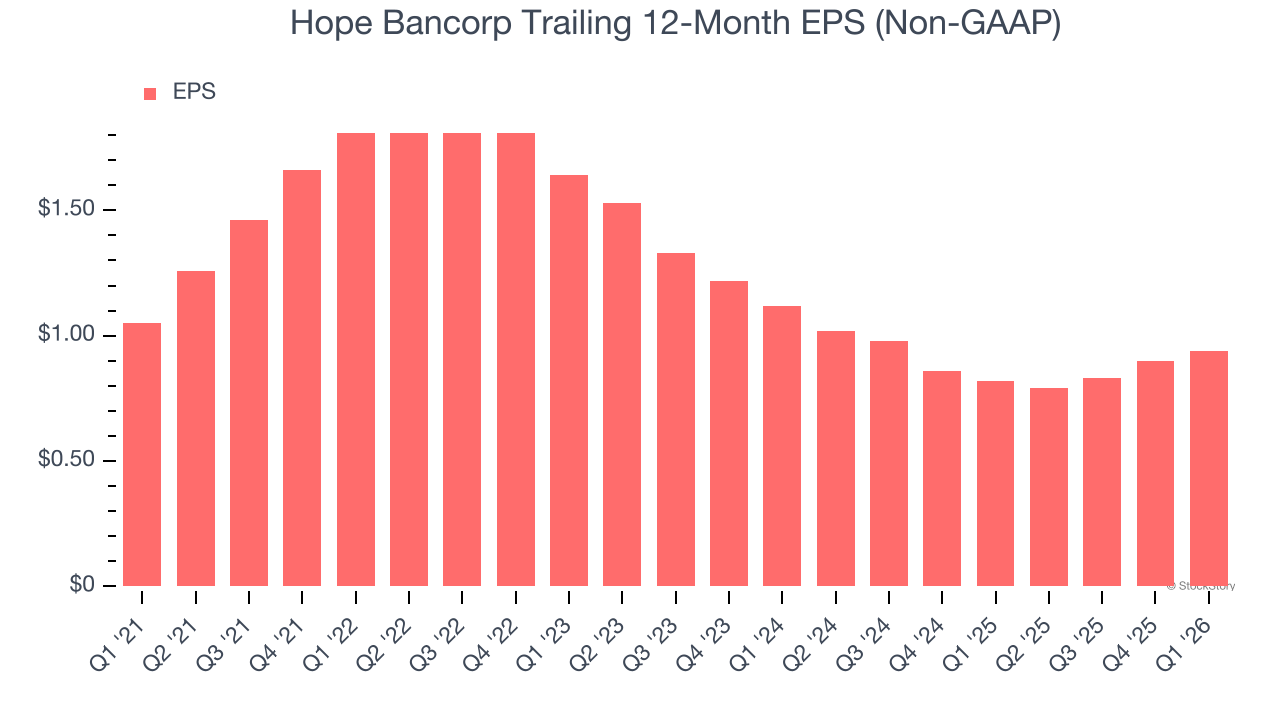

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Hope Bancorp, its EPS declined by 2.2% annually over the last five years while its revenue grew by 1.8%. This tells us the company became less profitable on a per-share basis as it expanded.

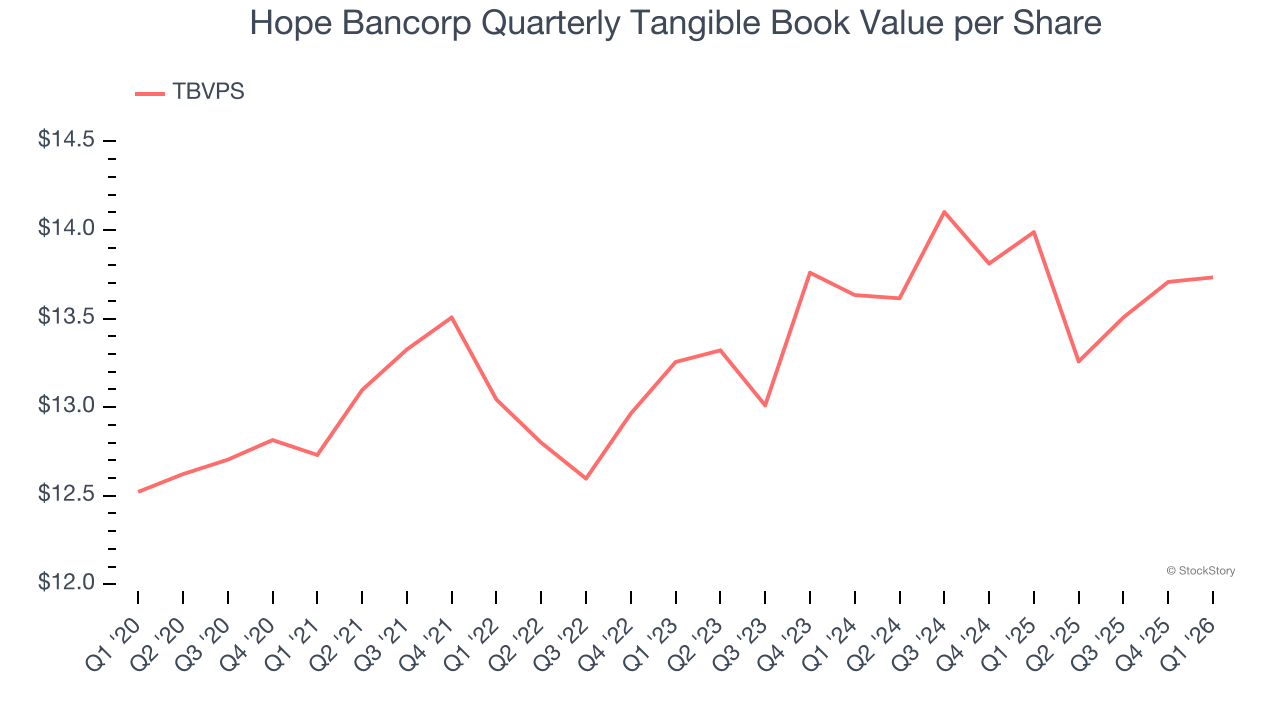

3. TBVPS Has Plateaued, Reflecting Stagnating Assets

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

Hope Bancorp’s TBVPS increased by a meager 1.5% annually over the last five years, and its recent performance paints an even worse picture as growth has stalled over the past two years, with TBVPS stuck at roughly $13.73 per share.

Final Judgment

Hope Bancorp falls short of our quality standards. With its shares topping the market in recent months, the stock trades at 0.7× forward P/B (or $13.40 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. We’d suggest looking at one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+1,154% between June 2020 and June 2025). Find your next big winner with StockStory today.