Credit Acceptance’s 35.6% return over the past six months has outpaced the S&P 500 by 27.3%, and its stock price has climbed to $625.97 per share. This performance may have investors wondering how to approach the situation.

Is now the time to buy Credit Acceptance, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Credit Acceptance Will Underperform?

Despite the momentum, we don’t have much confidence in Credit Acceptance. Here are three reasons you should be careful with CACC, plus one stock we’d rather own.

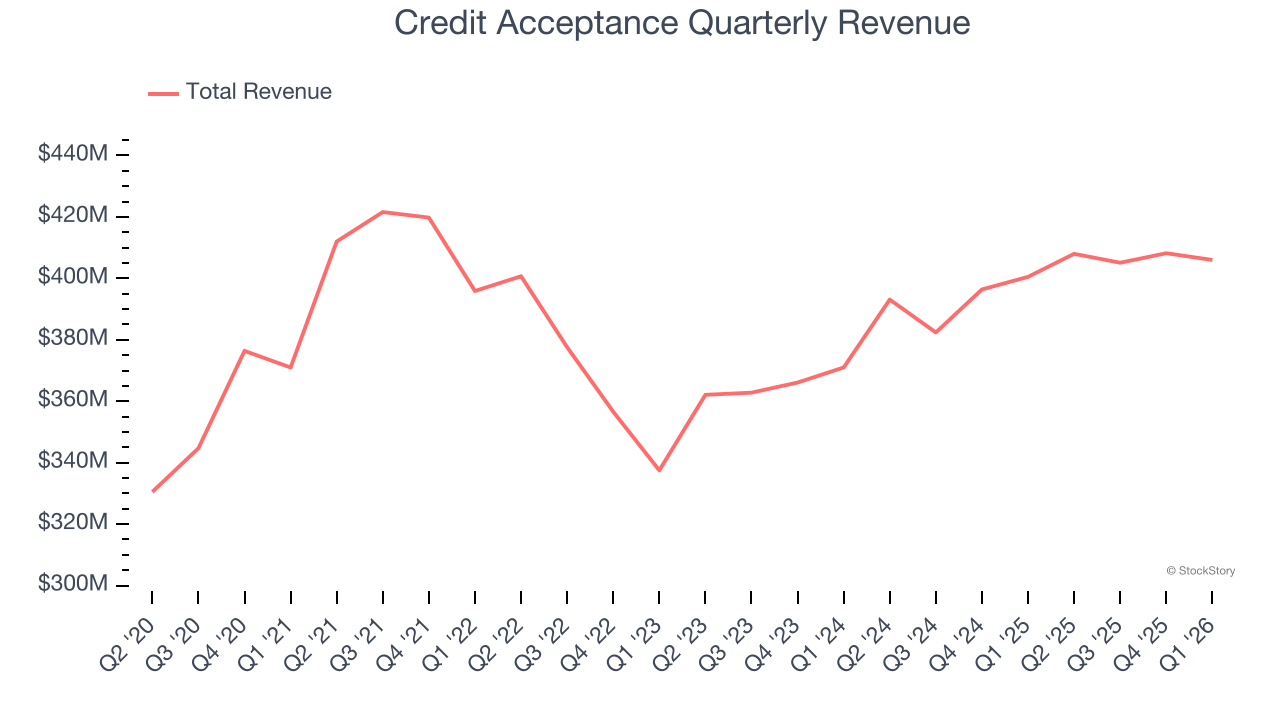

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

Over the last five years, Credit Acceptance grew its revenue at a sluggish 2.7% compounded annual growth rate. This fell short of our benchmarks.

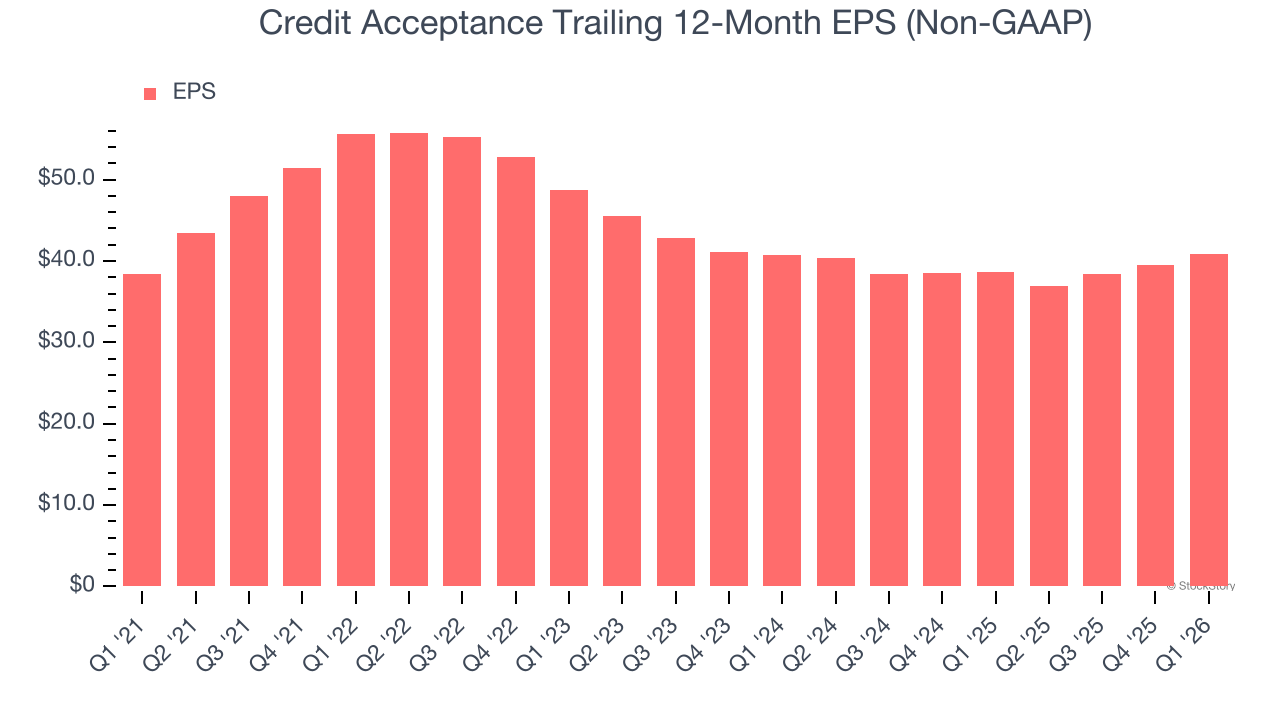

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Credit Acceptance’s weak 1.3% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

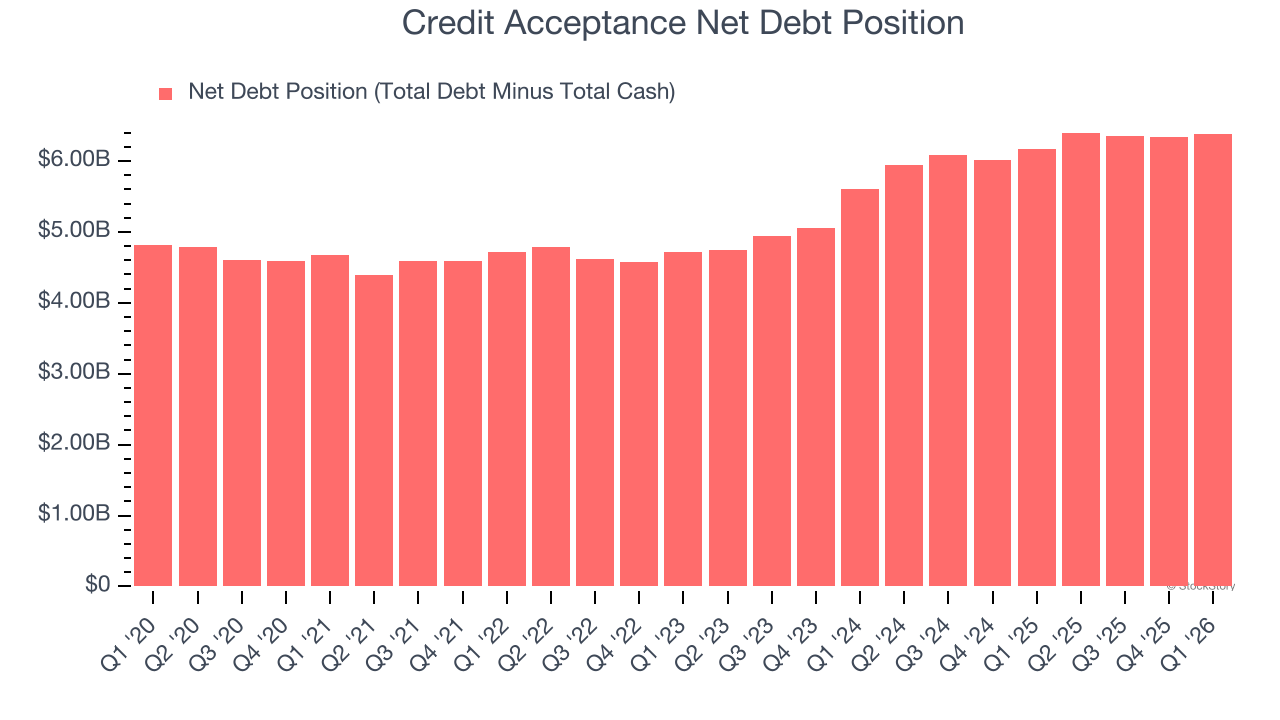

3. High Debt Levels Increase Risk

Credit Acceptance reported $25.7 million of cash and $6.41 billion of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With $647.3 million of EBITDA over the last 12 months, we view Credit Acceptance’s 9.9× net-debt-to-EBITDA ratio as inadequate. The company’s lacking profits relative to its borrowings give it little breathing room, raising red flags.

Final Judgment

We see the value of companies driving economic growth, but in the case of Credit Acceptance, we’re out. With its shares topping the market in recent months, the stock trades at 12.7× forward P/E (or $625.97 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. Let us point you toward an all-weather company that owns household favorite Taco Bell.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.