What a time it’s been for FormFactor. In the past six months alone, the company’s stock price has increased by a massive 62%, reaching $117.54 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in FormFactor, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is FormFactor Not Exciting?

We’re glad investors have benefited from the price increase, but we’re sitting this one out for now. Here are three reasons why FORM doesn’t excite us, plus one stock we’d rather own.

1. Long-Term Revenue Growth Disappoints

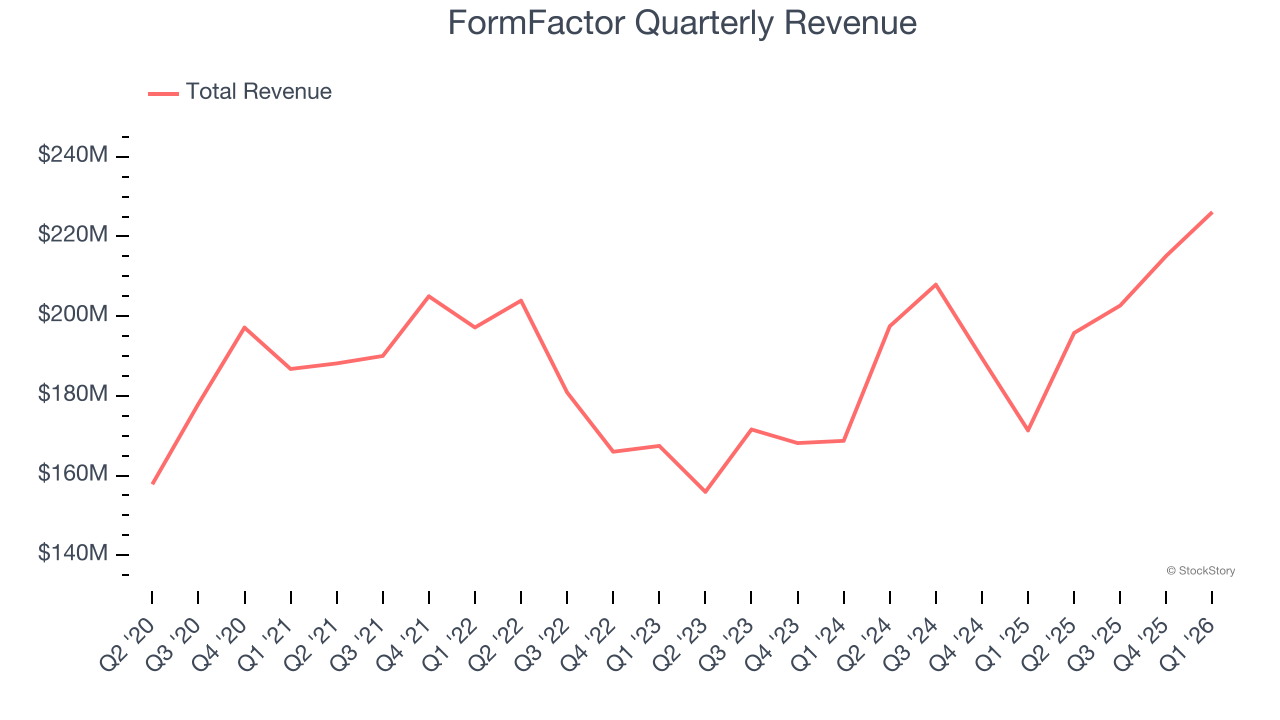

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, FormFactor’s 3.1% annualized revenue growth over the last five years was mediocre. This was below our standard for the semiconductor sector. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

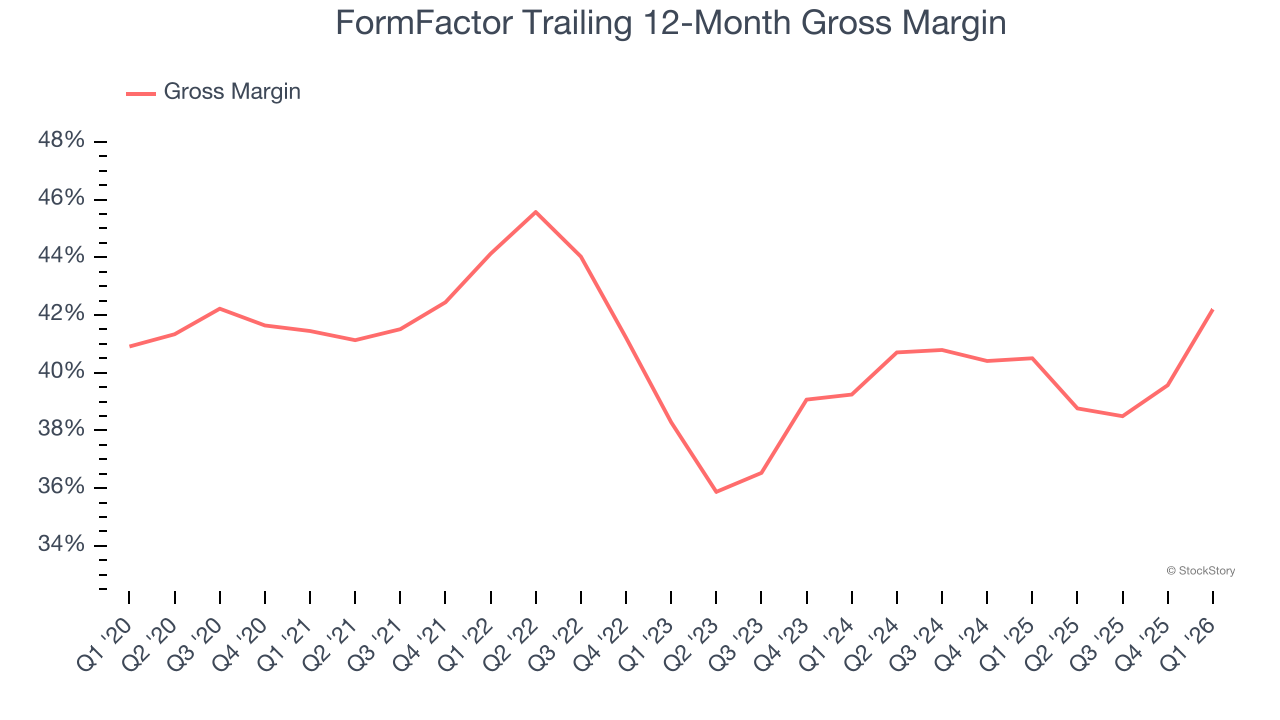

2. Low Gross Margin Reveals Weak Structural Profitability

In the semiconductor industry, a company’s gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

FormFactor’s gross margin is well below other semiconductor companies, indicating a lack of pricing power and a competitive market. As you can see below, it averaged a 41.4% gross margin over the last two years. Said differently, FormFactor had to pay a chunky $58.61 to its suppliers for every $100 in revenue.

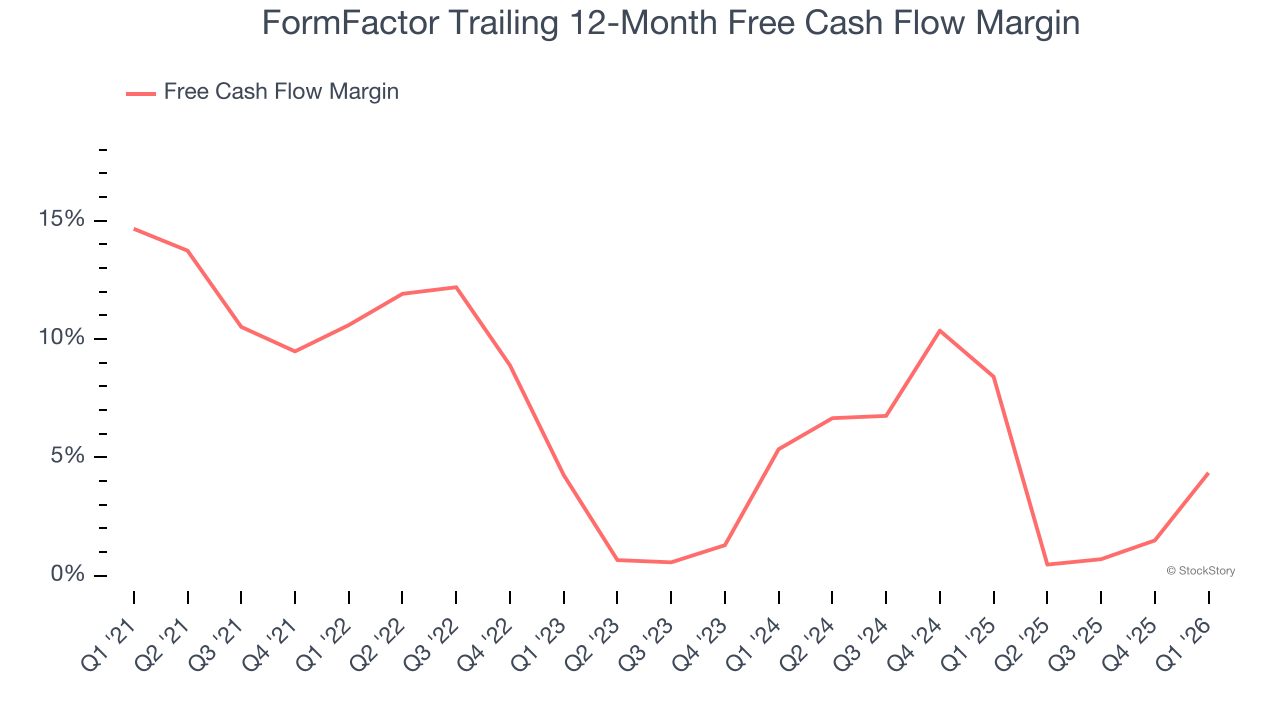

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

FormFactor has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 6.3%, below what we’d expect for a semiconductor business.

Final Judgment

FormFactor isn’t a terrible business, but it doesn’t pass our bar. After the recent surge, the stock trades at 47.3× forward P/E (or $117.54 per share). This multiple tells us a lot of good news is priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward one of our all-time favorite software stocks.

Stocks We Like More Than FormFactor

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.