Over the past six months, Albertsons’s shares (currently trading at $14.30) have posted a disappointing 17% loss, well below the S&P 500’s 7.2% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Albertsons, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Albertsons Will Underperform?

Even with the cheaper entry price, we’re sitting this one out for now. Here are three reasons why ACI doesn’t excite us, plus one stock we’d rather own.

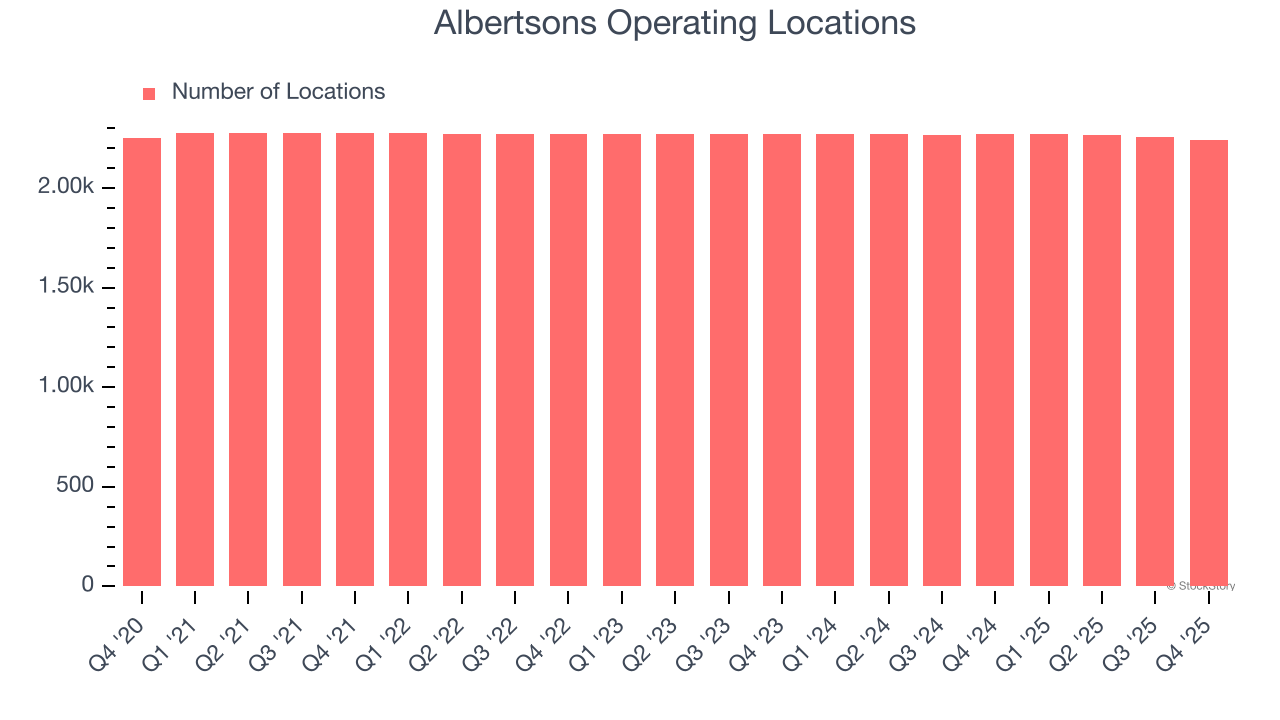

1. Lack of New Stores, a Headwind for Revenue

A retailer’s store count often determines how much revenue it can generate.

Albertsons operated 2,243 locations in the latest quarter, and over the last two years, has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

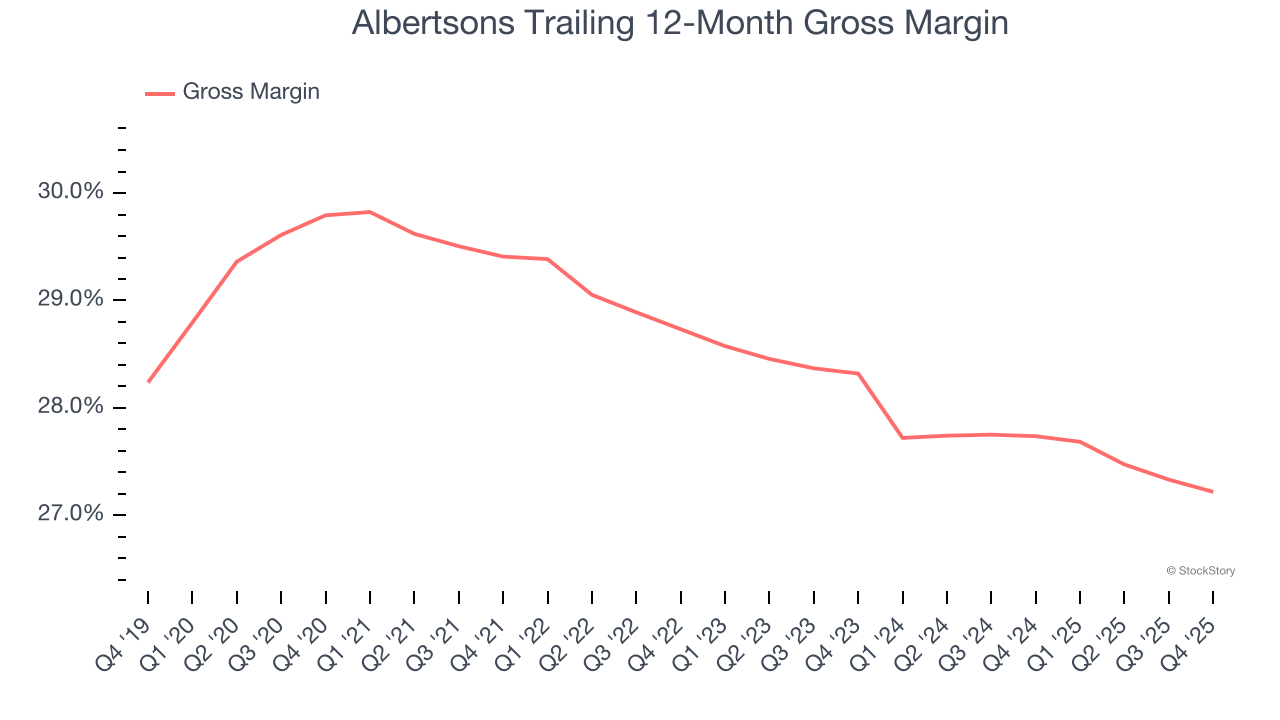

2. Low Gross Margin Reveals Weak Structural Profitability

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Albertsons has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 27.5% gross margin over the last two years. Said differently, Albertsons had to pay a chunky $72.53 to its suppliers for every $100 in revenue.

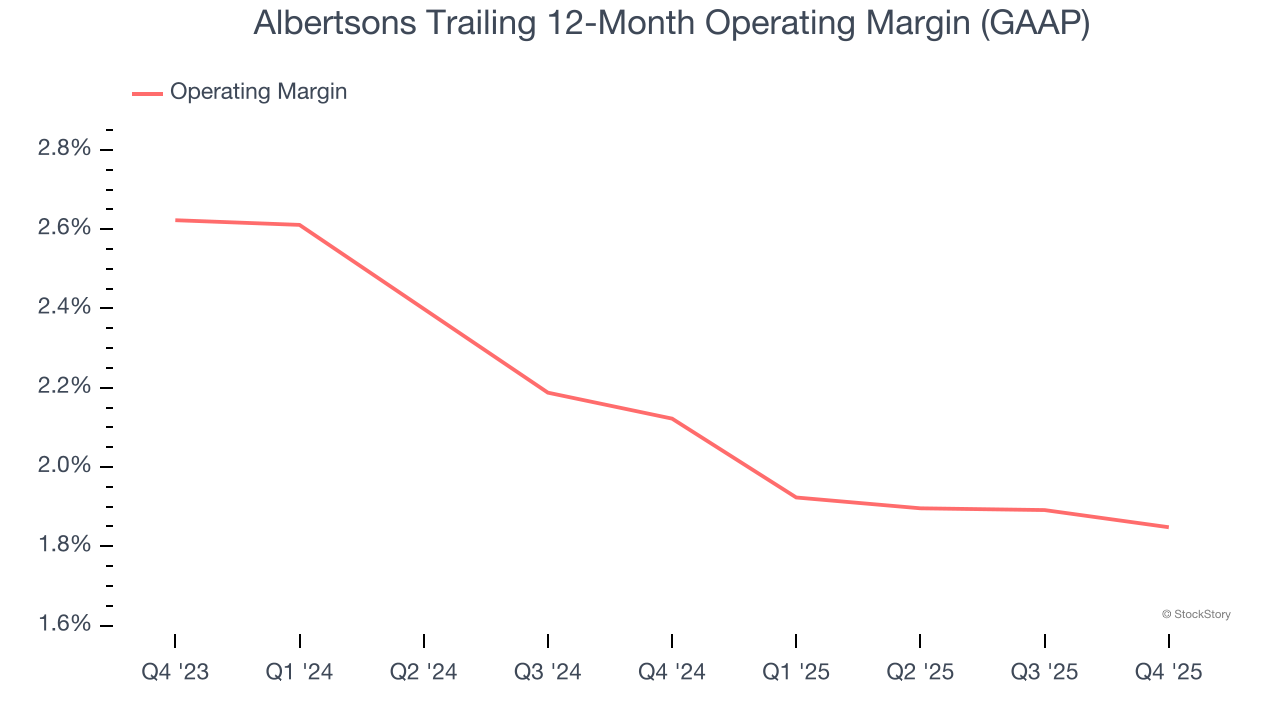

3. Weak Operating Margin Could Cause Trouble

Operating margin is an important measure of profitability for retailers as it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Albertsons’s operating margin has generally stayed the same over the last 12 months, averaging 2% over the last two years. This profitability was lousy for a consumer retail business and caused by its suboptimal cost structureand low gross margin.

Final Judgment

Albertsons doesn’t pass our quality test. Following the recent decline, the stock trades at 6.3× forward P/E (or $14.30 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Would Buy Instead of Albertsons

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.