Over the last six months, Waters Corporation’s shares have sunk to $357.08, producing a disappointing 7.2% loss - a stark contrast to the S&P 500’s 7.8% gain. This may have investors wondering how to approach the situation.

Following the pullback, is this a buying opportunity for WAT? Find out in our full research report, it’s free.

Why Does Waters Corporation Spark Debate?

Founded in 1958 and pioneering innovations in laboratory analysis for over six decades, Waters (NYSE: WAT) develops and manufactures analytical instruments, software, and consumables for liquid chromatography, mass spectrometry, and thermal analysis used in scientific research and quality testing.

Two Positive Attributes:

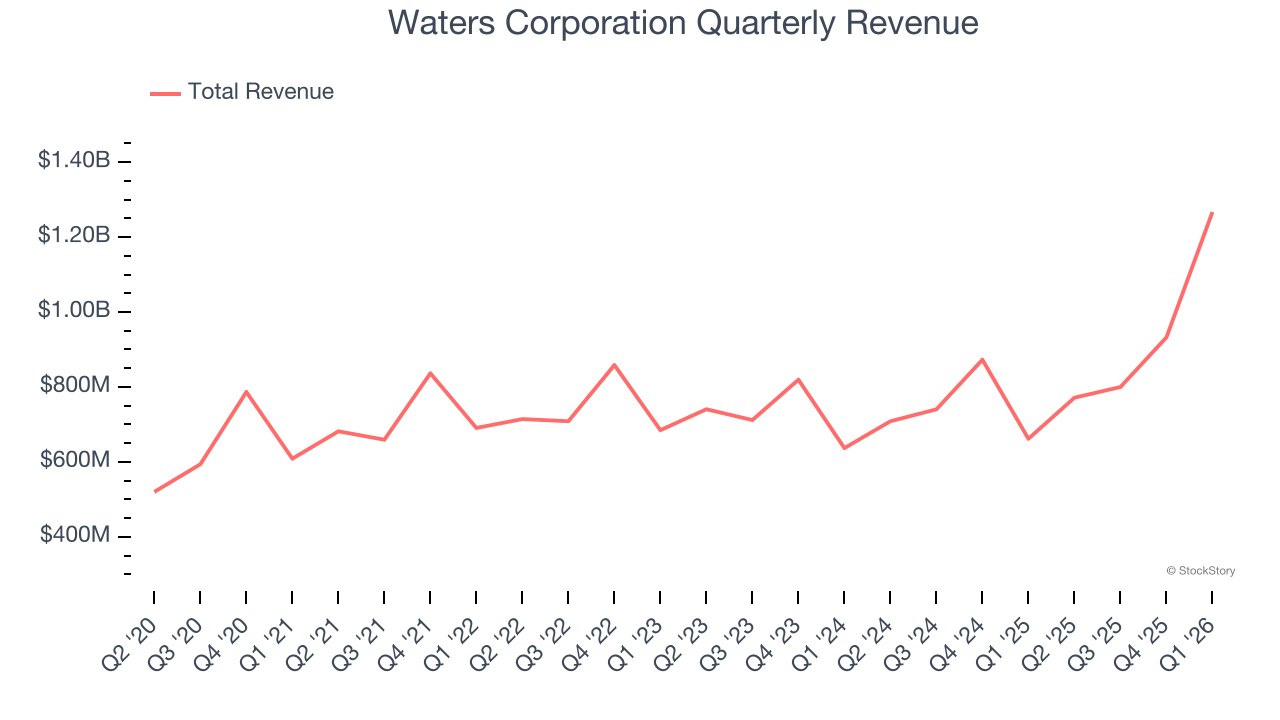

1. Long-Term Revenue Growth Shows Momentum

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Waters Corporation’s 8.5% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

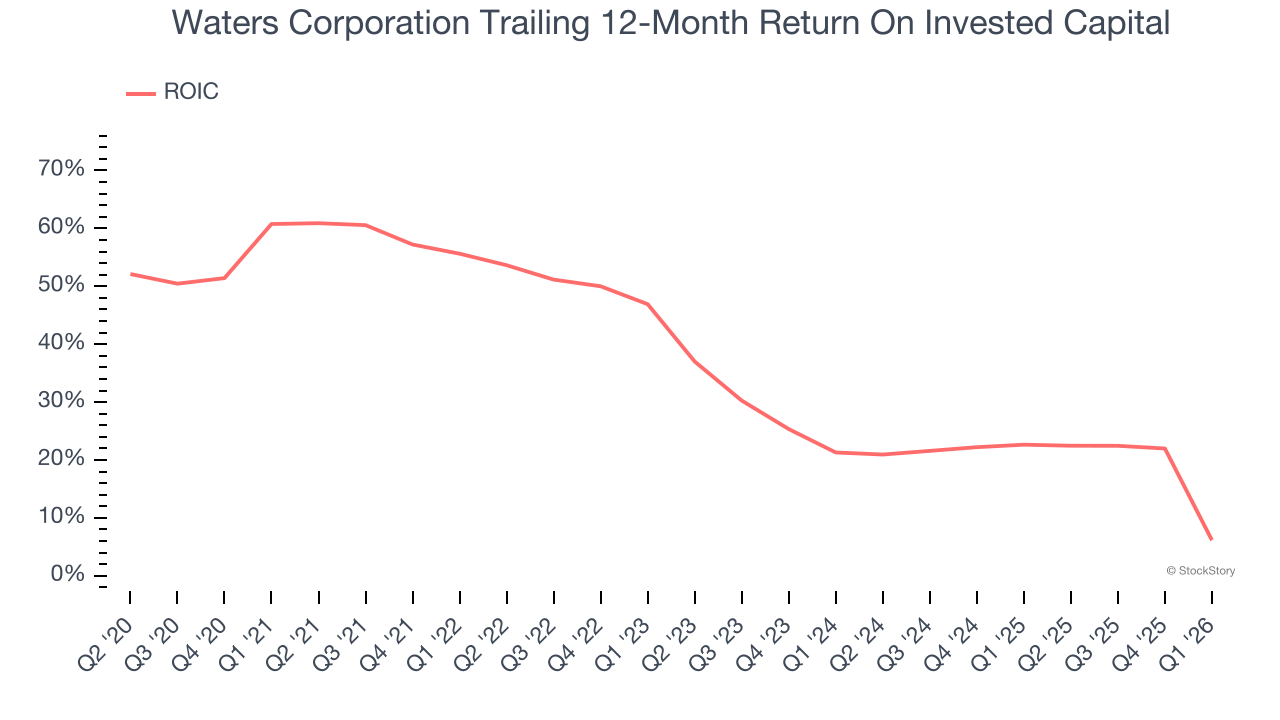

2. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Waters Corporation’s five-year average ROIC was 30.5%, placing it among the best healthcare companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

One Reason to Be Careful:

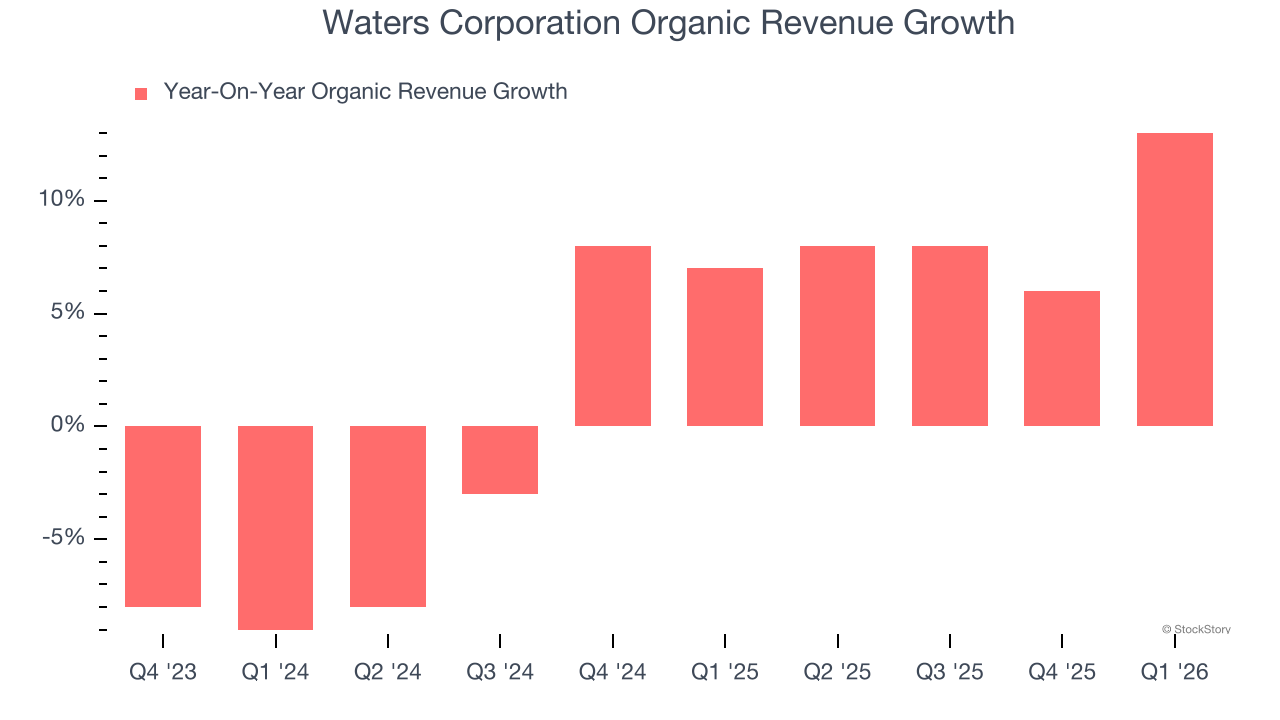

Slow Organic Growth Suggests Waning Demand In Core Business

We can better understand Research Tools & Consumables companies by analyzing their organic revenue. This metric gives visibility into Waters Corporation’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Waters Corporation’s organic revenue averaged 4.9% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Final Judgment

Waters Corporation’s merits more than compensate for its flaws. After the recent drawdown, the stock trades at 23.9× forward P/E (or $357.08 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Waters Corporation

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.