Gap’s stock price has taken a beating over the past six months, shedding 22.5% of its value and falling to $20.59 per share. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Gap, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Gap Not Exciting?

Despite the more favorable entry price, we’re sitting this one out for now. Here are three reasons we avoid GAP, plus one stock we’d rather own.

1. Long-Term Revenue Growth Flatter Than a Pancake

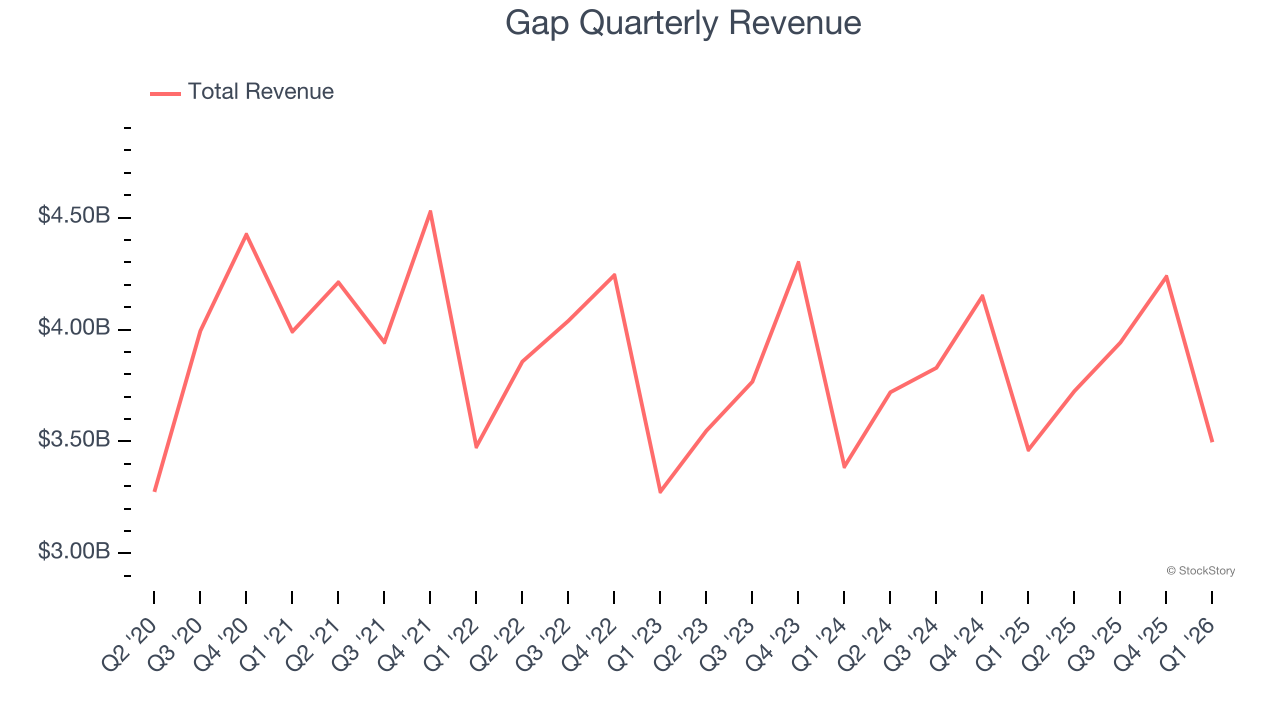

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Gap struggled to consistently increase demand as its $15.4 billion of sales for the trailing 12 months was close to its revenue three years ago. This wasn’t a great result and signals it’s a lower quality business.

2. Lack of New Stores, a Headwind for Revenue

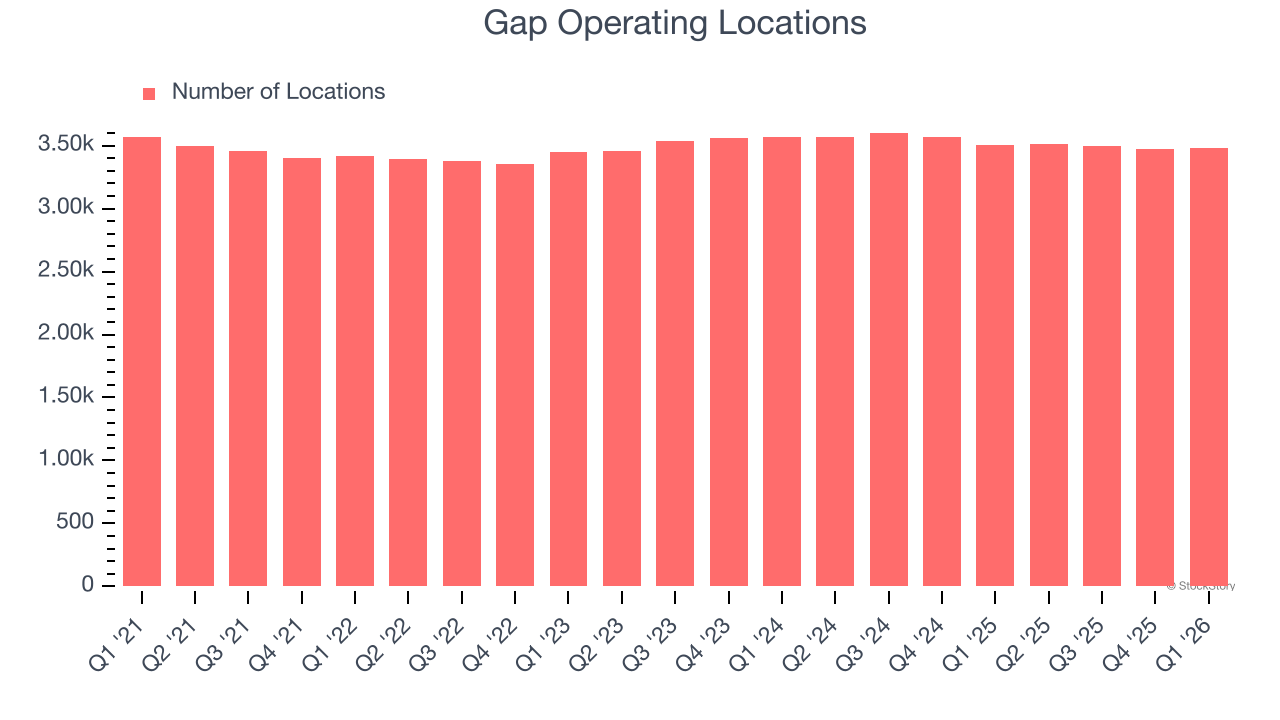

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Gap operated 3,477 locations in the latest quarter, and over the last two years, has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Gap historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.4%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+.

Final Judgment

Gap’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 8.5× forward P/E (or $20.59 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We’re fairly confident there are better investments elsewhere. Let us point you toward one of our top software and edge computing picks.

Stocks We Like More Than Gap

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.