Over the past six months, OceanFirst Financial’s shares (currently trading at $18.53) have posted a disappointing 6.1% loss, well below the S&P 500’s 7.8% gain. This might have investors contemplating their next move.

Is now the time to buy OceanFirst Financial, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think OceanFirst Financial Will Underperform?

Even though the stock has become cheaper, we don’t have much confidence in OceanFirst Financial. Here are three reasons you should be careful with OCFC, plus one stock we’d rather own.

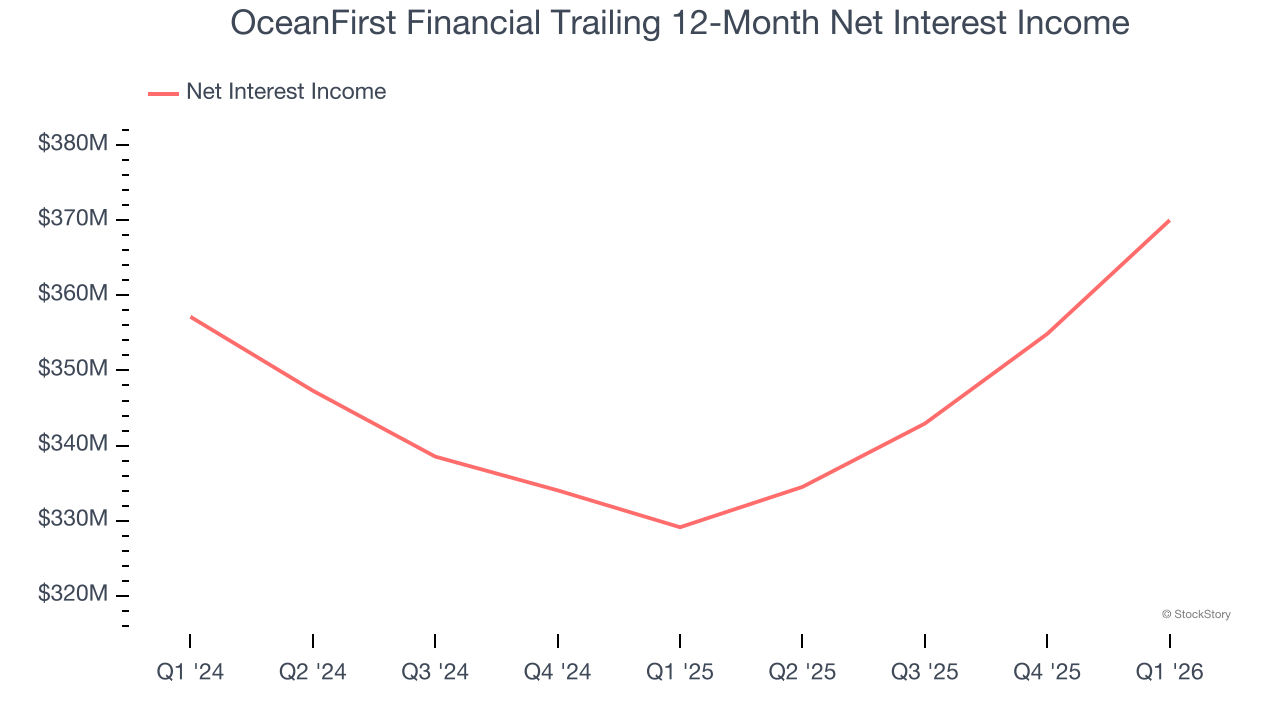

1. Net Interest Income Points to Soft Demand

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

OceanFirst Financial’s net interest income has grown at a 3.8% annualized rate over the last five years, much worse than the broader banking industry and in line with its total revenue. This was driven by its loan growth as its net interest margin, which represents how much a bank earns in relation to its outstanding loan book, declined throughout that period.

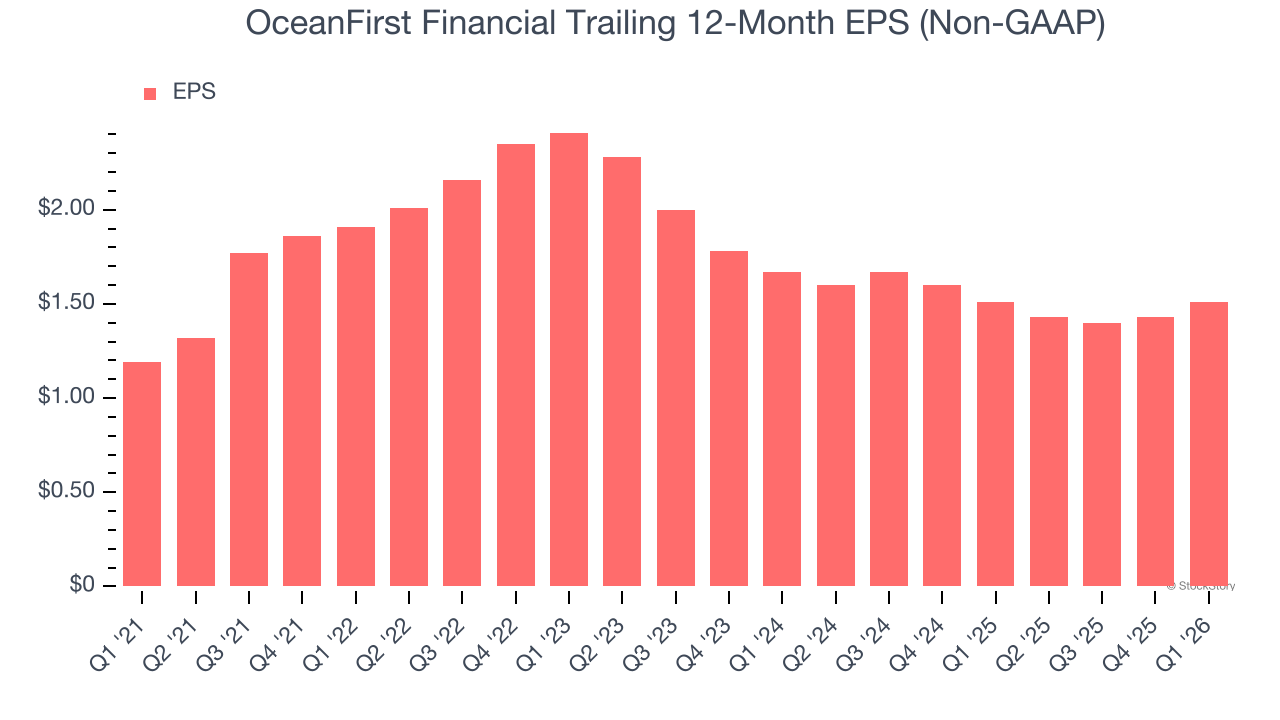

2. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

OceanFirst Financial’s EPS grew at 4.9% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 2.8% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

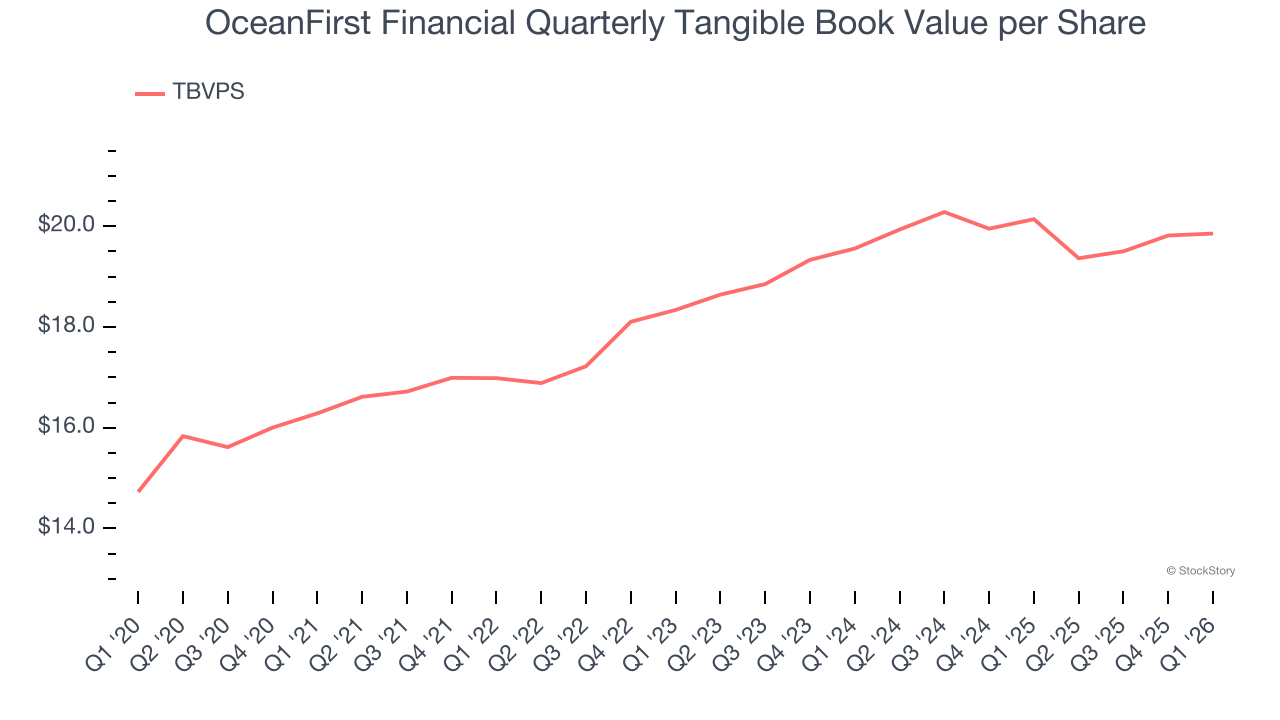

3. TBVPS Projections Show Stormy Skies Ahead

Tangible book value per share (TBVPS) growth is driven by a bank’s ability to earn more than its cost of capital through lending activities while maintaining a strong balance sheet.

Over the next 12 months, Consensus estimates call for OceanFirst Financial’s TBVPS to shrink by 1.4% to $19.57, a sour projection.

Final Judgment

OceanFirst Financial doesn’t pass our quality test. After the recent drawdown, the stock trades at 0.7× forward P/B (or $18.53 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment. Let us point you toward the most dominant software business in the world.

Stocks We Would Buy Instead of OceanFirst Financial

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.