Cruise ship company Carnival (NYSE: CCL) met Wall Street’s revenue expectations in Q2 CY2026, with sales up 5.3% year on year to $6.66 billion. Its non-GAAP profit of $0.41 per share was 22.2% above analysts’ consensus estimates.

Is now the time to buy Carnival? Find out by accessing our full research report, it’s free.

Carnival (CCL) Q2 CY2026 Highlights:

- Revenue: $6.66 billion vs analyst estimates of $6.69 billion (5.3% year-on-year growth, in line)

- Adjusted EPS: $0.41 vs analyst estimates of $0.34 (22.2% beat)

- Adjusted EBITDA: $1.58 billion vs analyst estimates of $1.48 billion (23.7% margin, 6.8% beat)

- Management slightly raised its full-year Adjusted EPS guidance to $2.22 at the midpoint

- EBITDA guidance for the full year is $7.11 billion at the midpoint, below analyst estimates of $7.19 billion

- Operating Margin: 12.8%, down from 14.8% in the same quarter last year

- Free Cash Flow Margin: 26.3%, up from 24.4% in the same quarter last year

- Passenger Cruise Days: up 400,000 year on year

- Market Capitalization: $38.9 billion

"We achieved another quarter of record results, marking our twelfth consecutive quarter of record net yields and delivering over 20 percent more to the bottom line, overcoming extreme geopolitical headwinds and nearly 30 percent higher fuel costs. Continued commercial execution and a step up in our cost efficiency efforts enabled us to exceed our March guidance by $100 million. These results reflect the strong demand for our portfolio of world-class cruise lines and the continued progress we are making across the business," said Carnival Corporation's Chief Executive Officer Josh Weinstein.

Company Overview

Boasting outrageous amenities like a planetarium on board its ships, Carnival (NYSE: CCL) is one of the world's largest leisure travel companies and a prominent player in the cruise industry.

Revenue Growth

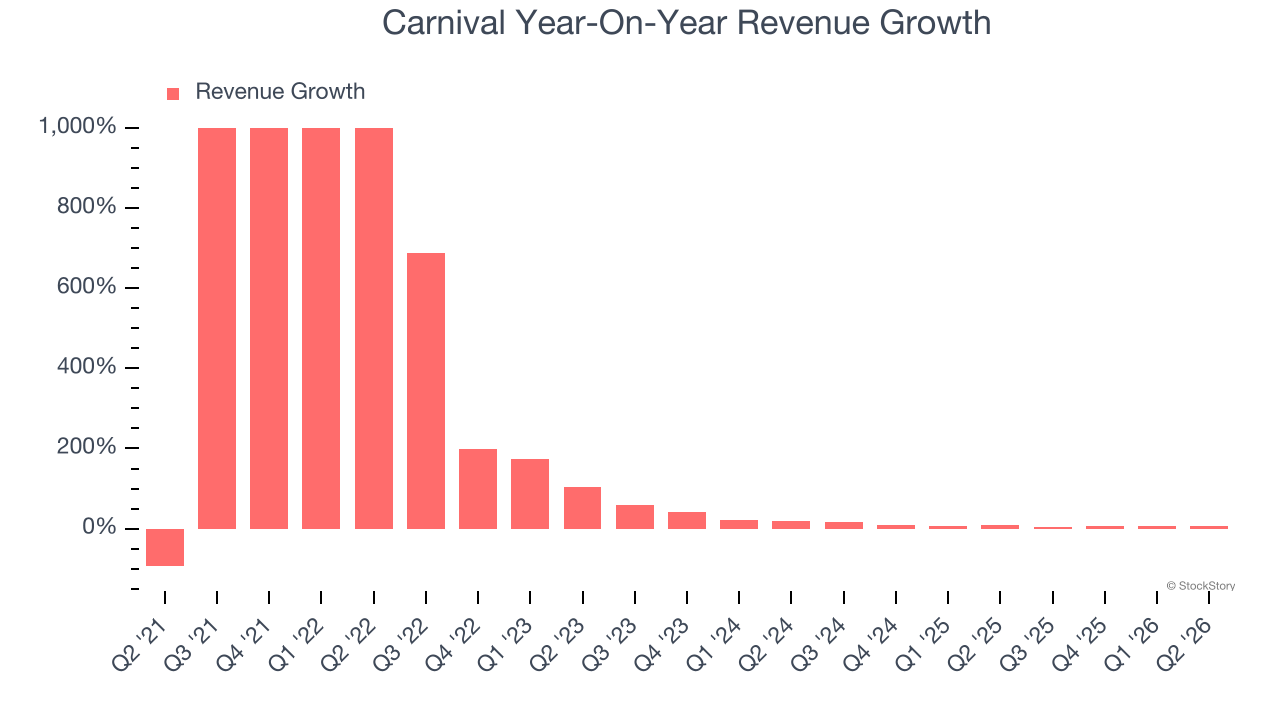

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Carnival’s sales grew at an incredible 187% compounded annual growth rate over the last five years. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Carnival’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 7.9% over the last two years was well below its five-year trend.

We can dig further into the company’s revenue dynamics by analyzing its number of passenger cruise days, which reached 25.7 million in the latest quarter. Over the last two years, Carnival’s passenger cruise days averaged 1.2% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Carnival grew its revenue by 5.3% year on year, and its $6.66 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Carnival’s operating margin has more or less stayed the same over the last 12 months , and we generally like to see margin increases due to economies of scale and cost efficiency over time.

This quarter, Carnival generated an operating margin profit margin of 12.8%, down 2 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth — for example, a company could inflate its sales through excessive spending on advertising and promotions.

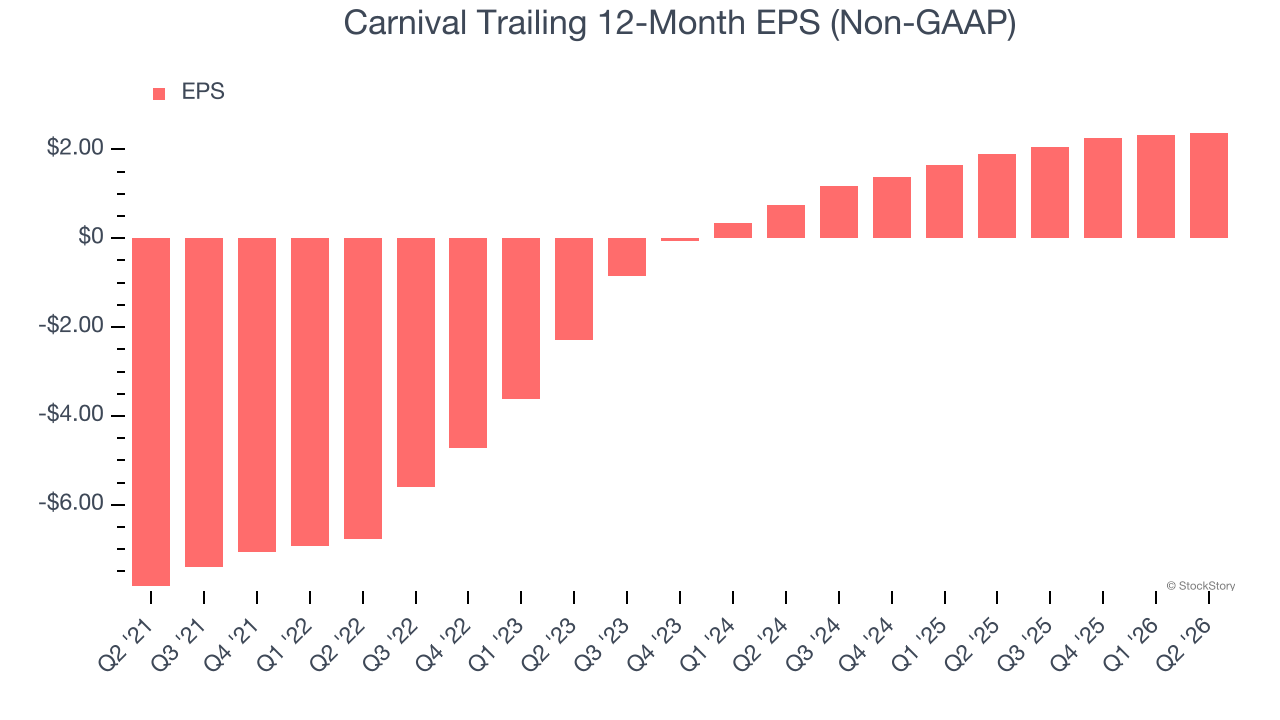

Carnival’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q2, Carnival reported adjusted EPS of $0.41, up from $0.35 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Carnival’s full-year EPS to shrink by 4.4% from $2.38 to $2.28.

Key Takeaways from Carnival’s Q2 Results

It was good to see Carnival beat analysts’ EPS expectations this quarter. We were also happy its adjusted operating income outperformed Wall Street’s estimates. On the other hand, its EBITDA guidance for next quarter missed and its full-year EBITDA guidance fell slightly short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The market seemed to be hoping for more, and the stock traded down 6.1% to $28.36 immediately following the results.

So do we think Carnival is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).