eBay has had an impressive run over the past six months as its shares have beaten the S&P 500 by 21.5%. The stock now trades at $109.19, marking a 27.9% gain. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy eBay, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is eBay Not Exciting?

Despite the momentum, we don’t have much confidence in eBay. Here are three reasons you should be careful with EBAY, plus one stock we’d rather own.

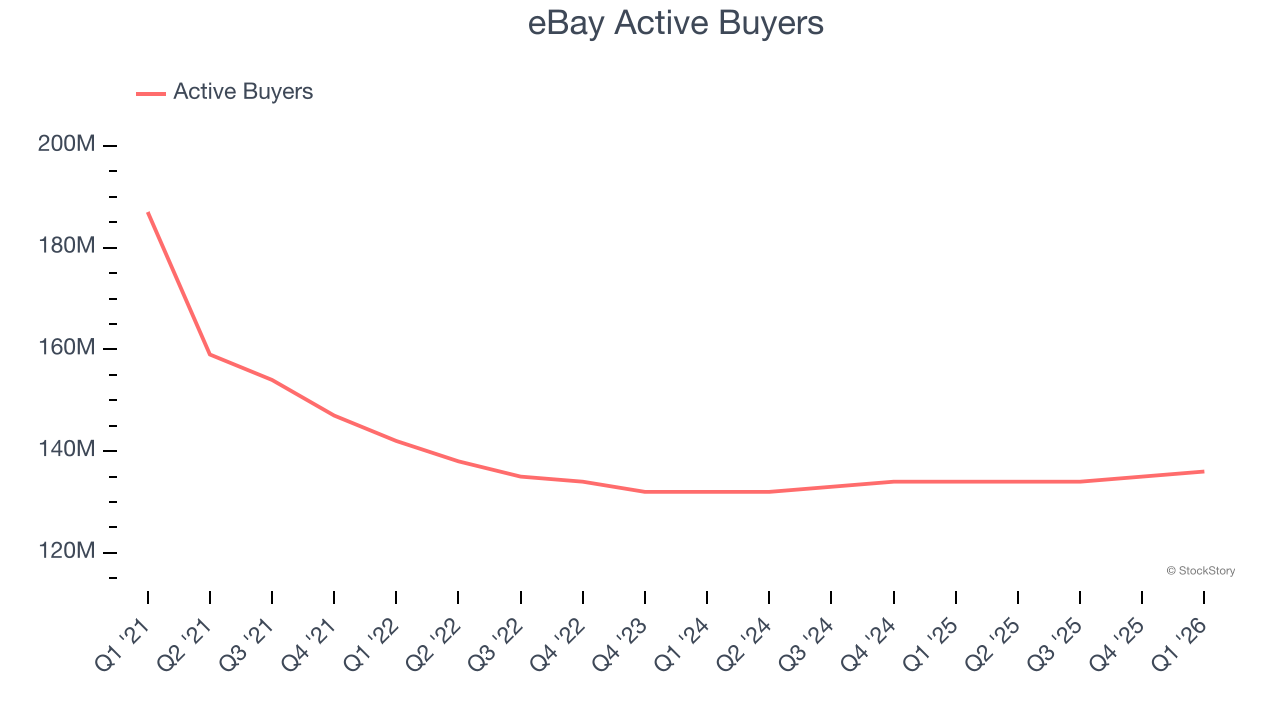

1. Change in Active Buyers Points to Soft Demand

As an online marketplace, eBay generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, eBay’s active buyers, a key performance metric for the company, increased by 1.3% annually to 136 million in the latest quarter. This growth rate is one of the lowest in the consumer internet sector, largely a function of its already massive scale and saturated market. If eBay wants to reaccelerate growth, it likely needs to innovate with new products.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect eBay’s revenue to rise by 5.8%, close to This projection is underwhelming and indicates its newer products and services will not lead to better top-line performance yet.

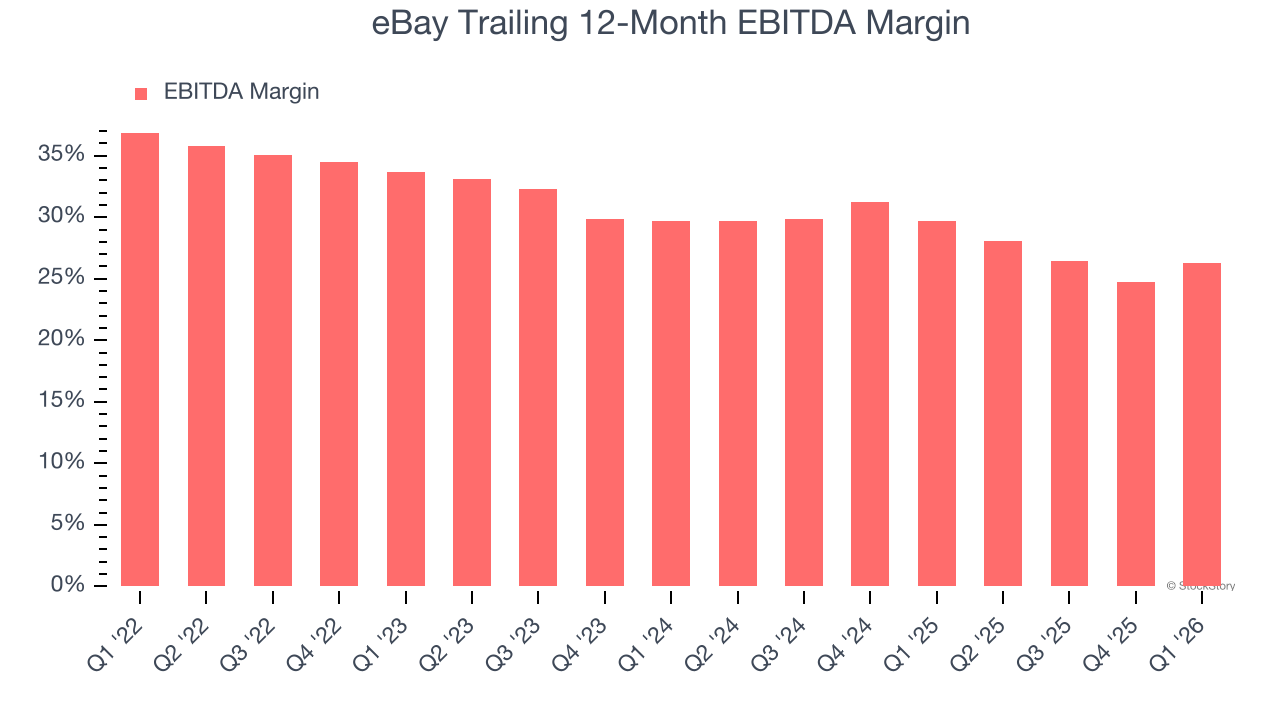

3. Shrinking EBITDA Margin

EBITDA is a good way of judging operating profitability for consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a more standardized view of the business’s profit potential.

Analyzing the trend in its profitability, eBay’s EBITDA margin decreased by 7.4 percentage points over the last few years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its EBITDA margin for the trailing 12 months was 26.3%.

Final Judgment

eBay’s business quality ultimately falls short of our standards. With its shares outperforming the market lately, the stock trades at 13.8× forward EV/EBITDA (or $109.19 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of eBay

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.