The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how sit-down dining stocks fared in Q1, starting with Bloomin' Brands (NASDAQ: BLMN).

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

The 9 sit-down dining stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 0.9%.

In light of this news, share prices of the companies have held steady as they are up 3.5% on average since the latest earnings results.

Bloomin' Brands (NASDAQ: BLMN)

Owner of the iconic Australian-themed Outback Steakhouse, Bloomin’ Brands (NASDAQ: BLMN) is a leading American restaurant company that owns and operates a portfolio of popular restaurant brands.

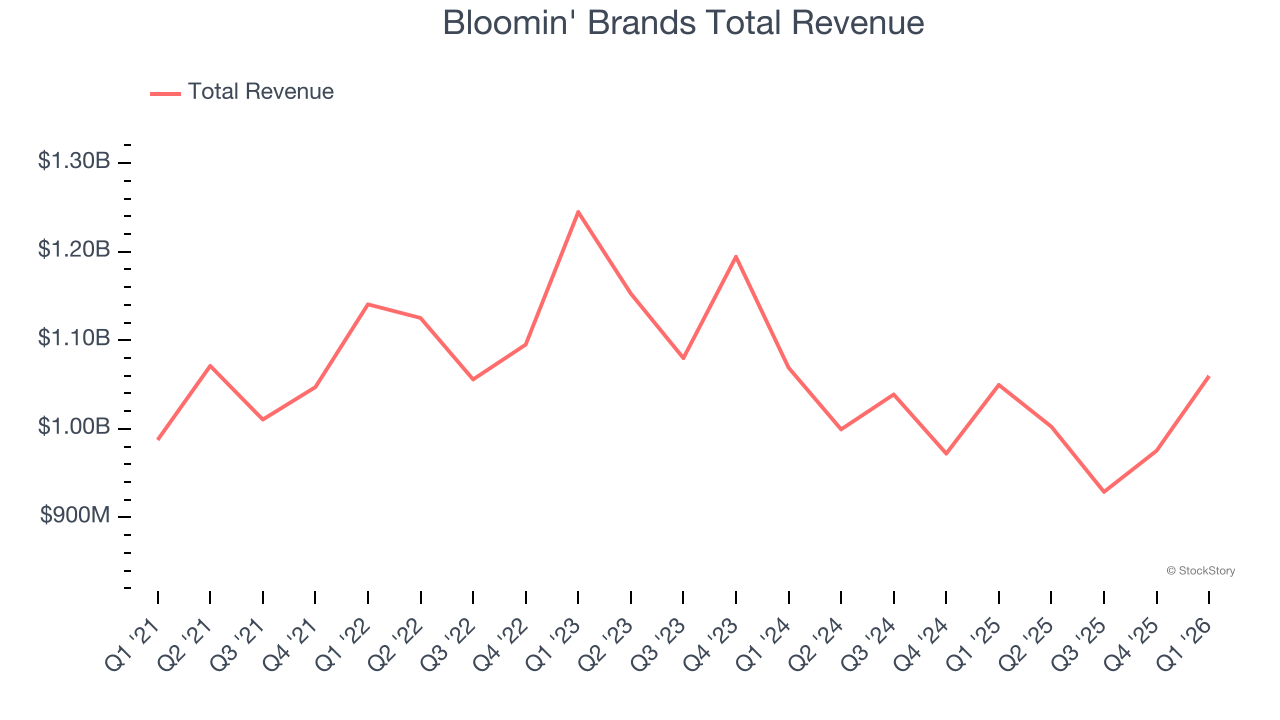

Bloomin' Brands reported revenues of $1.06 billion, flat year on year. This print exceeded analysts’ expectations by 1.6%. Overall, it was an exceptional quarter for the company with EPS guidance for next quarter exceeding analysts’ expectations and a solid beat of analysts’ EBITDA estimates.

Bloomin' Brands delivered the slowest revenue growth of the whole group. Interestingly, the stock is up 38.2% since reporting and currently trades at $7.96.

Is now the time to buy Bloomin' Brands? Access our full analysis of the earnings results here, it’s free.

Best Q1: Kura Sushi (NASDAQ: KRUS)

Known for its conveyor belt that transports dishes to diners, Kura Sushi (NASDAQ: KRUS) is a chain of sushi restaurants serving traditional Japanese fare with a touch of modernity and technology.

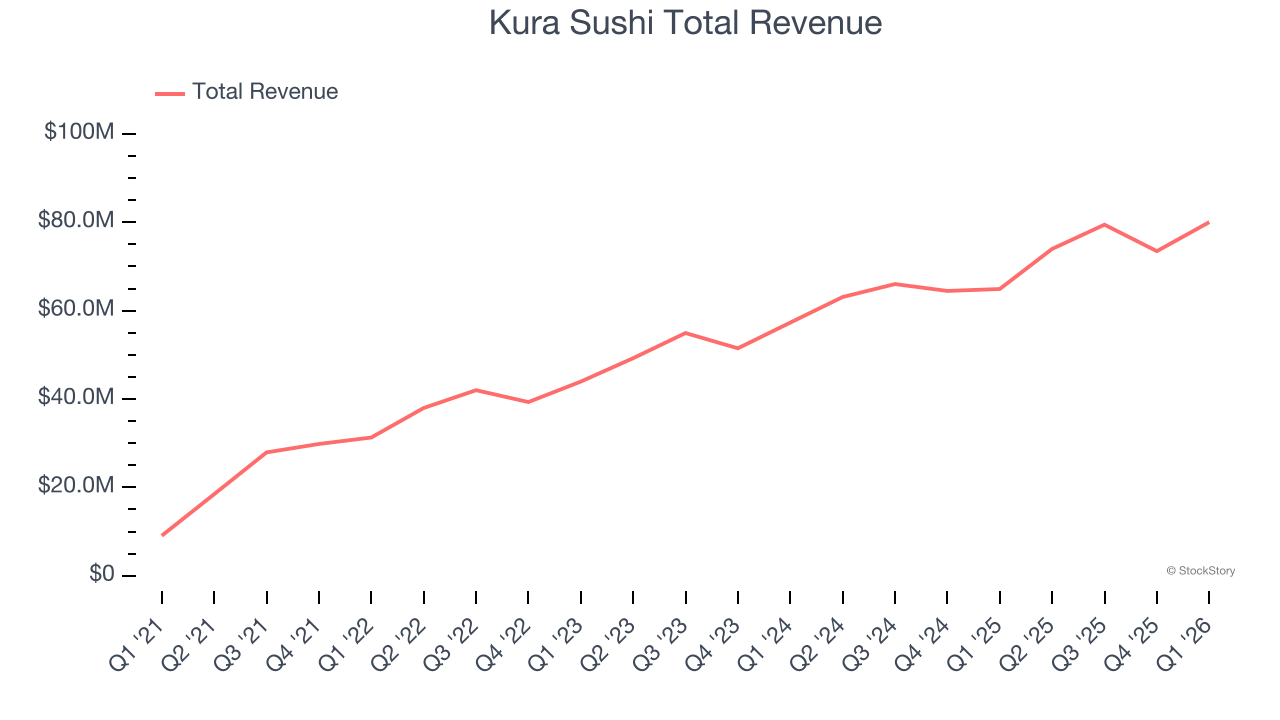

Kura Sushi reported revenues of $80.02 million, up 23.3% year on year, outperforming analysts’ expectations by 2.5%. The business had a stunning quarter with a beat of analysts’ EPS and EBITDA estimates.

Kura Sushi scored the biggest analyst estimates beat, fastest revenue growth, and highest full-year guidance raise among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 23.5% since reporting. It currently trades at $55.85.

Is now the time to buy Kura Sushi? Access our full analysis of the earnings results here, it’s free.

Brinker International (NYSE: EAT)

Founded by Norman Brinker in Dallas, Brinker International (NYSE: EAT) is a casual restaurant chain that operates the Chili’s, Maggiano’s Little Italy, and It’s Just Wings banners.

Brinker International reported revenues of $1.47 billion, up 3.2% year on year, in line with analysts’ expectations. It was a mixed quarter as it posted a narrow beat of analysts’ EBITDA estimates and full-year revenue guidance meeting analysts’ expectations.

Brinker International delivered the weakest performance against analyst estimates and weakest full-year guidance update in the group. Interestingly, the stock is up 1.2% since the results and currently trades at $130.72.

Read our full analysis of Brinker International’s results here.

First Watch (NASDAQ: FWRG)

Based on a nautical reference to the first work shift aboard a ship, First Watch (NASDAQ: FWRG) is a chain of breakfast and brunch restaurants whose menu is heavily-focused on eggs and griddle items such as pancakes.

First Watch reported revenues of $331 million, up 17.3% year on year. This result was in line with analysts’ expectations. Overall, it was a very strong quarter as it also produced a solid beat of analysts’ EBITDA and same-store sales estimates.

The stock is down 9.7% since reporting and currently trades at $11.03.

Read our full, actionable report on First Watch here, it’s free.

The Cheesecake Factory (NASDAQ: CAKE)

Celebrated for its delicious (and free) brown bread, gigantic portions, and delectable desserts, Cheesecake Factory (NASDAQ: CAKE) is an iconic American restaurant chain that also owns and operates a portfolio of separate restaurant brands.

The Cheesecake Factory reported revenues of $978.8 million, up 5.6% year on year. This number topped analysts’ expectations by 1.5%. It was a very strong quarter as it also logged an impressive beat of analysts’ same-store sales estimates and a solid beat of analysts’ revenue estimates.

The stock is down 4.2% since reporting and currently trades at $60.02.

Read our full, actionable report on The Cheesecake Factory here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.