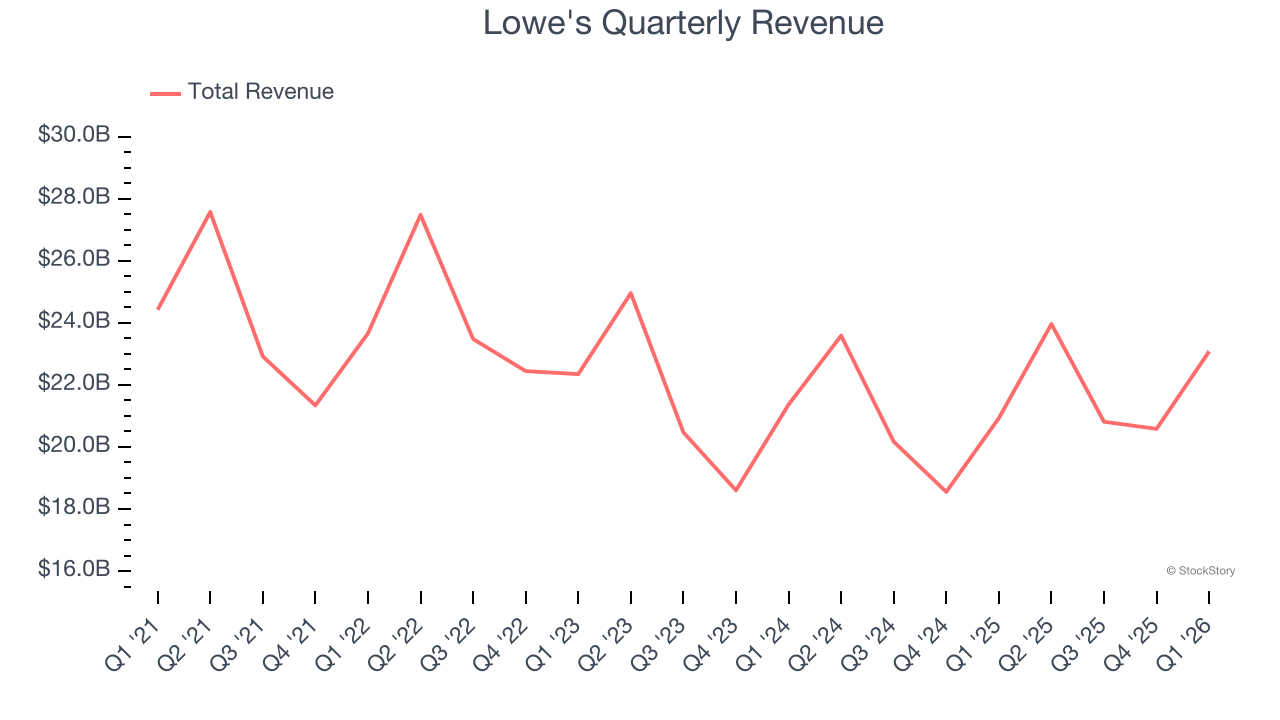

Home improvement retailer Lowe’s (NYSE: LOW) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 10.3% year on year to $23.08 billion. The company expects the full year’s revenue to be around $93 billion, close to analysts’ estimates. Its non-GAAP profit of $3.03 per share was 2.1% above analysts’ consensus estimates.

Is now the time to buy Lowe's? Find out by accessing our full research report, it’s free.

Lowe's (LOW) Q1 CY2026 Highlights:

- Revenue: $23.08 billion vs analyst estimates of $22.95 billion (10.3% year-on-year growth, 0.6% beat)

- Adjusted EPS: $3.03 vs analyst estimates of $2.97 (2.1% beat)

- Adjusted EBITDA: $3.26 billion vs analyst estimates of $3.13 billion (14.1% margin, 4.1% beat)

- The company reconfirmed its revenue guidance for the full year of $93 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $12.50 at the midpoint

- Operating Margin: 11.1%, in line with the same quarter last year

- Free Cash Flow Margin: 12.3%, down from 13.7% in the same quarter last year

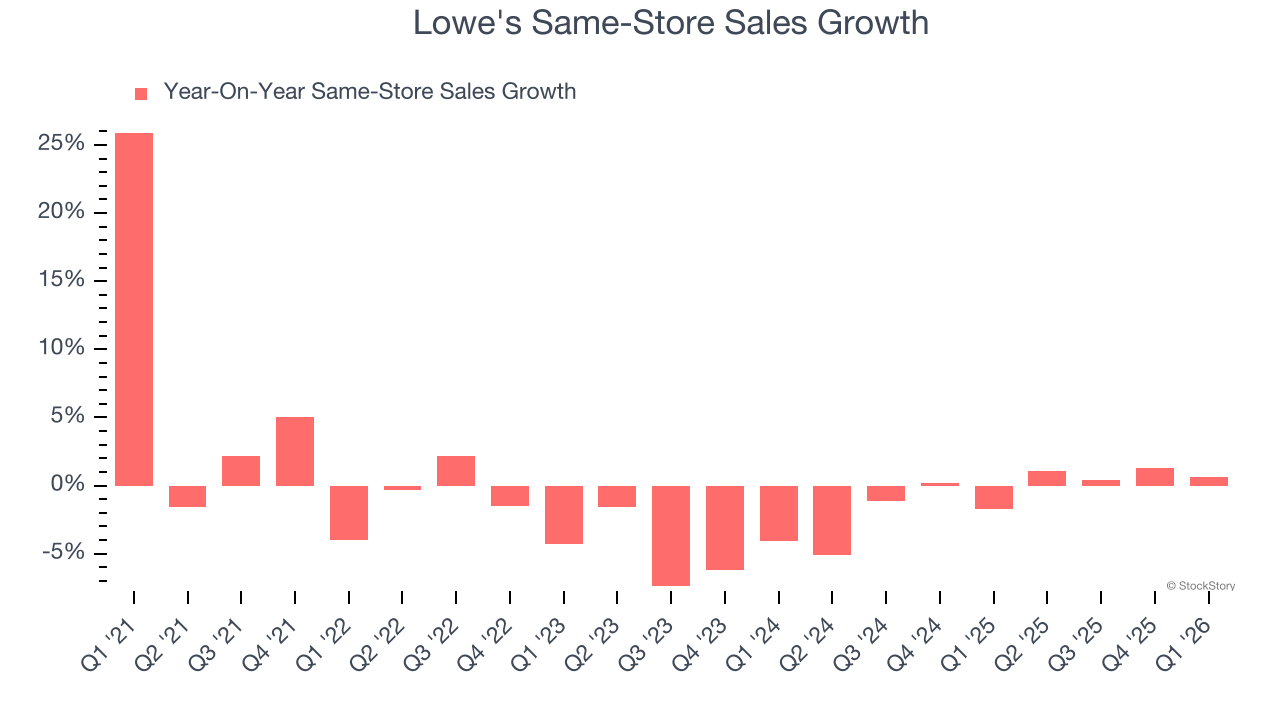

- Same-Store Sales were flat year on year (-1.7% in the same quarter last year)

- Market Capitalization: $122.3 billion

"Strong spring execution and continued momentum in Pro, Appliances, Online, and Home Services supported a solid start to the year as we delivered our fourth consecutive quarter of positive comp sales," said Marvin R. Ellison, Lowe's chairman, president and CEO.

Company Overview

Founded in North Carolina as Lowe's North Wilkesboro Hardware, the company is a home improvement retailer that sells everything from paint to tools to building materials.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $88.43 billion in revenue over the past 12 months, Lowe's is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because there is only so much real estate to build new stores, placing a ceiling on its growth. To accelerate sales, Lowe's likely needs to optimize its pricing or lean into international expansion.

As you can see below, Lowe's struggled to generate demand over the last three years. Its sales dropped by 2.6% annually as it didn’t open many new stores.

This quarter, Lowe's reported year-on-year revenue growth of 10.3%, and its $23.08 billion of revenue exceeded Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to grow 6.3% over the next 12 months, an acceleration versus the last three years. This projection is particularly healthy for a company of its scale and implies its newer products will catalyze better top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

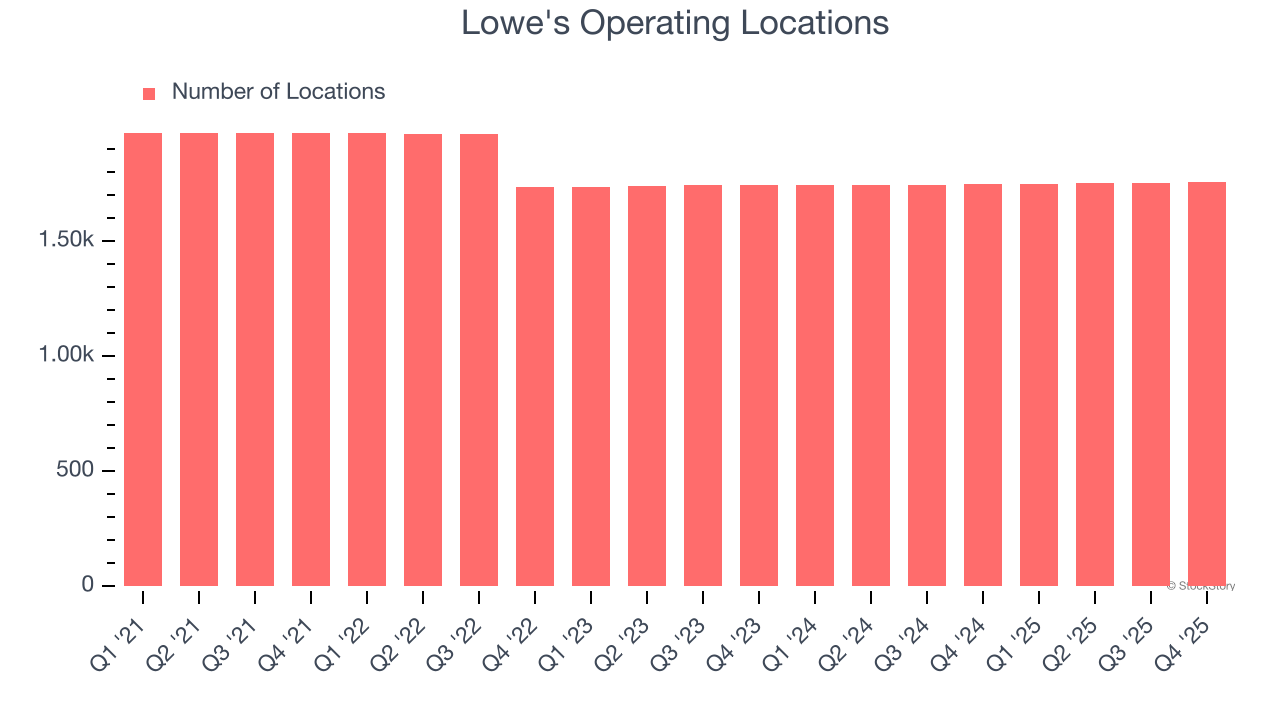

Store Performance

Number of Stores

Over the last two years, Lowe's has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Note that Lowe's reports its store count intermittently, so some data points are missing in the chart below.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Lowe’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if Lowe's starts opening new stores to artificially boost revenue growth.

In the latest quarter, Lowe’s year on year same-store sales were flat. This performance was more or less in line with its historical levels.

Key Takeaways from Lowe’s Q1 Results

We enjoyed seeing Lowe's beat analysts’ EPS expectations this quarter. We were also happy its revenue and gross margin both narrowly outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance slightly missed. This seems to be weighing on shares, and the stock traded down 2.5% to $213.00 immediately following the results.

So should you invest in Lowe's right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).