Hyatt Hotels has been treading water for the past six months, recording a small return of 3.8% while holding steady at $144.35.

Is there a buying opportunity in Hyatt Hotels, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Hyatt Hotels Will Underperform?

We're cautious about Hyatt Hotels. Here are three reasons we avoid H and a stock we'd rather own.

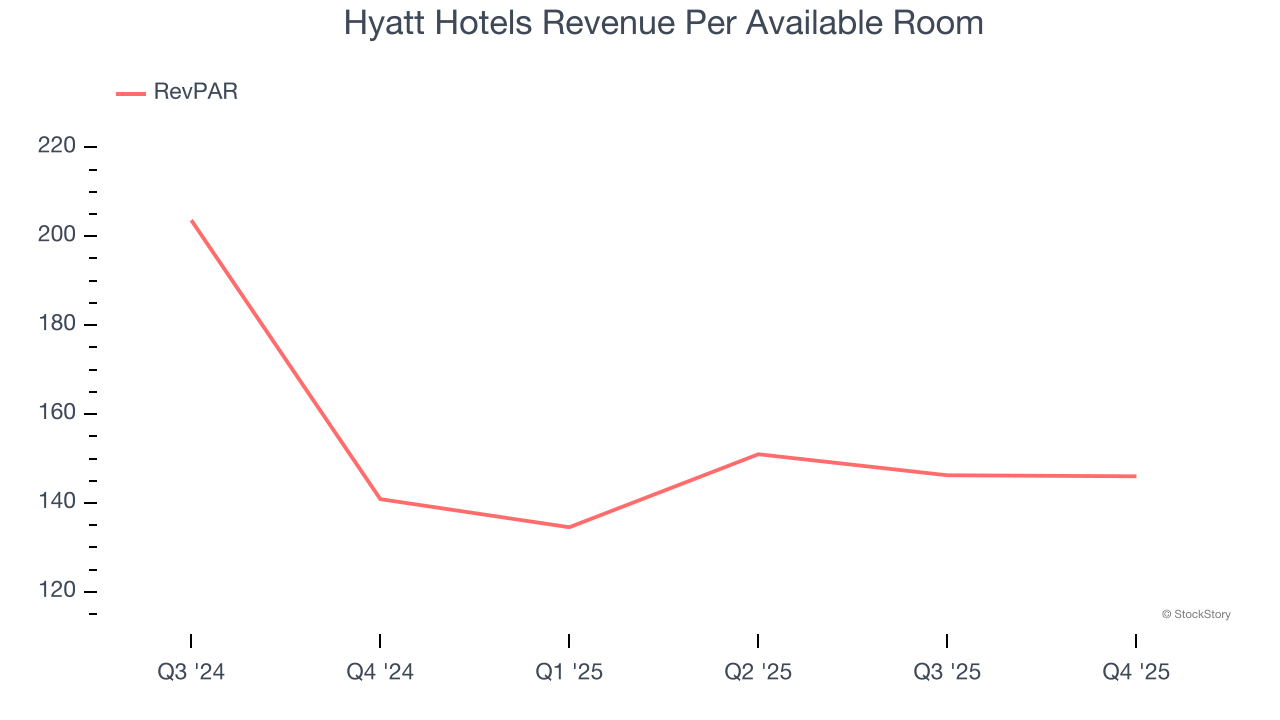

1. Declining RevPAR, Demand Takes a Hit

Investors interested in Consumer Discretionary - Travel and Vacation Providers companies should track RevPAR (revenue per available room) in addition to reported revenue. This metric accounts for daily rates and occupancy levels, painting a holistic picture of Hyatt Hotels’s demand characteristics.

Hyatt Hotels’s RevPAR came in at $146.01 in the latest quarter, and it averaged 12.3% year-on-year declines over the last two years. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Hyatt Hotels might have to invest in new amenities such as restaurants and bars to attract customers - this isn’t ideal because expansions can complicate operations and be quite expensive (i.e., renovations and increased overhead).

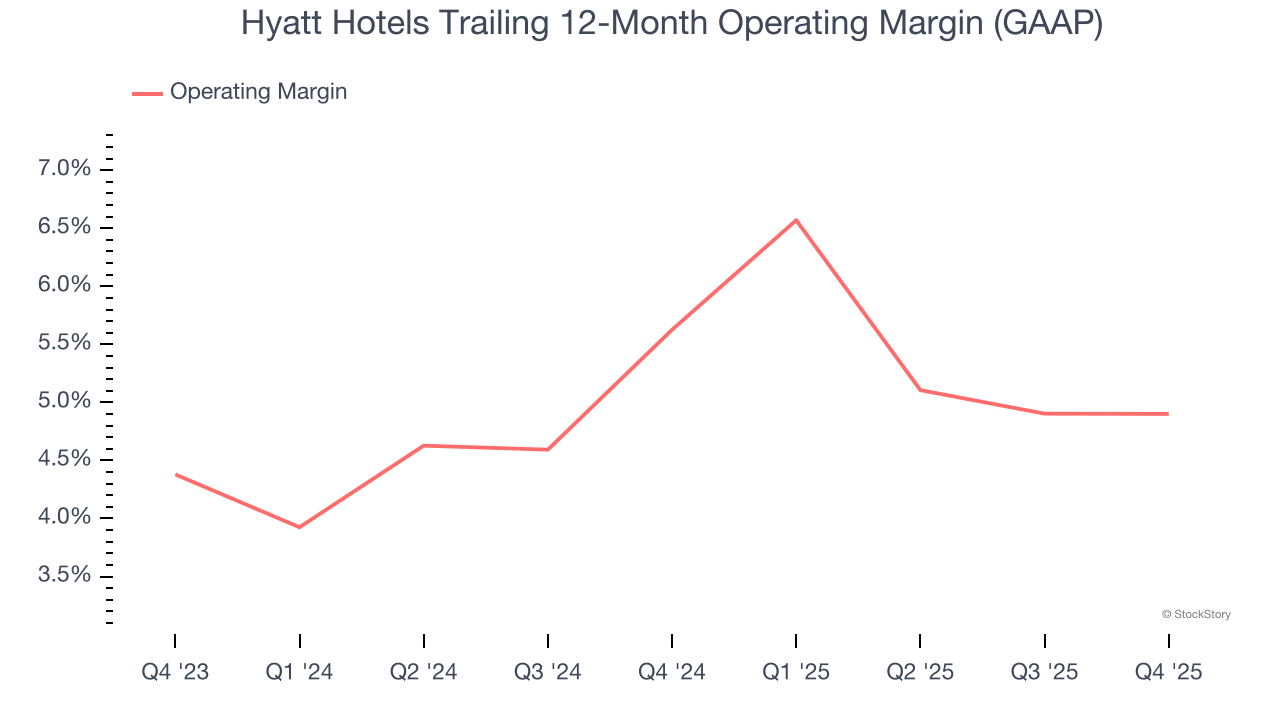

2. Weak Operating Margin Could Cause Trouble

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Hyatt Hotels’s operating margin has more or less stayed the same over the last 12 months , and we generally like to see margin increases due to economies of scale and cost efficiency over time.

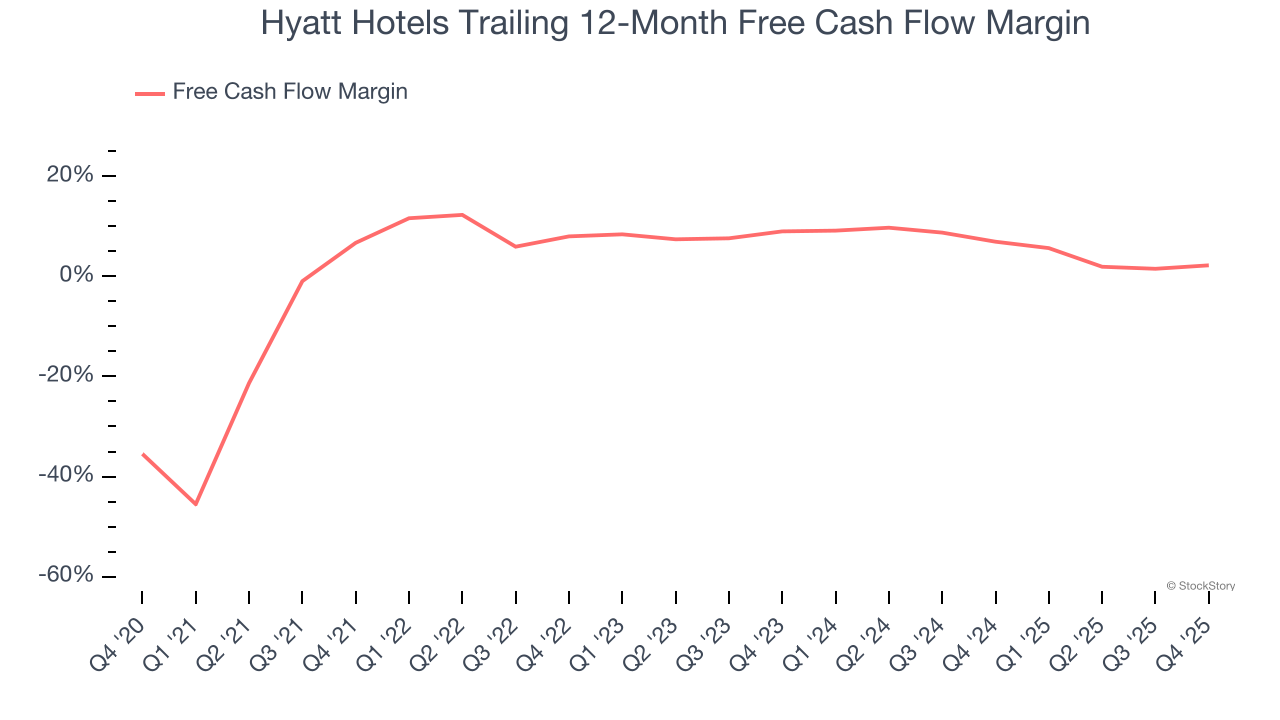

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Hyatt Hotels has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 4.5%, below what we’d expect for a consumer discretionary business.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Hyatt Hotels, we’ll be cheering from the sidelines. That said, the stock currently trades at 44.6× forward P/E (or $144.35 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Would Buy Instead of Hyatt Hotels

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.