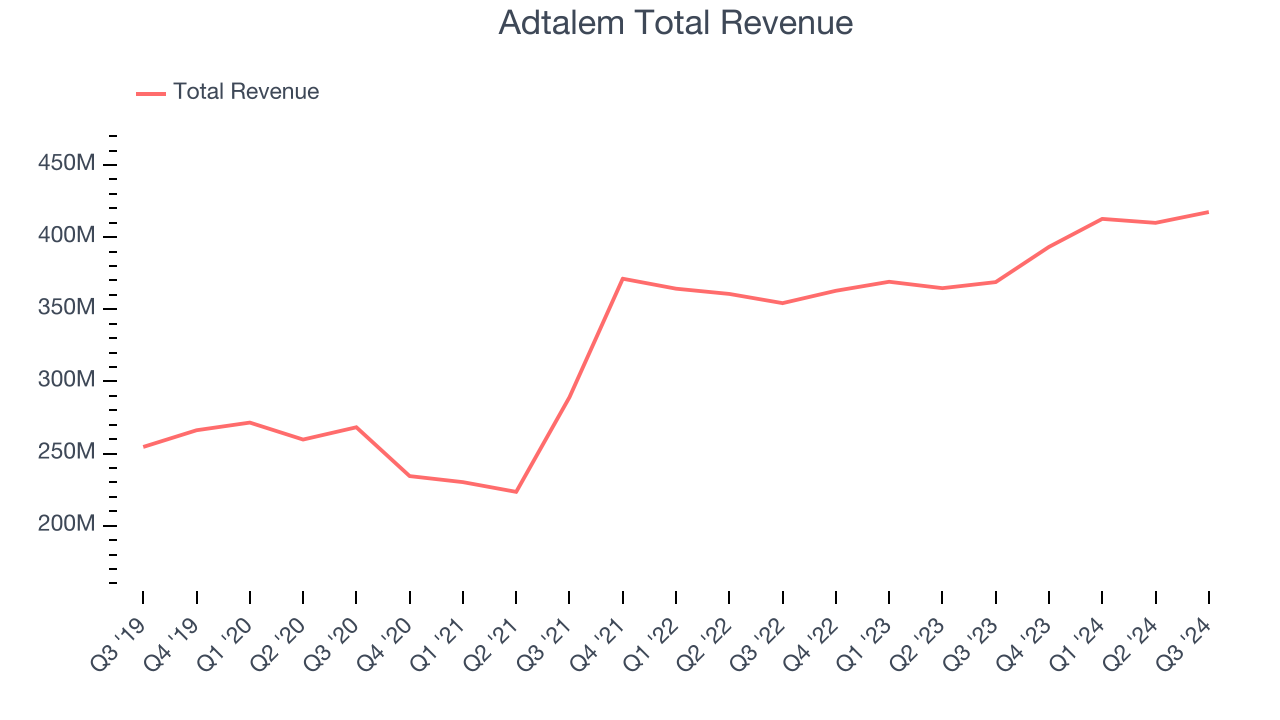

Vocational education company Adtalem Global Education (NYSE: ATGE) reported Q3 CY2024 results topping the market’s revenue expectations, with sales up 13.2% year on year to $417.4 million. The company’s full-year revenue guidance of $1.71 billion at the midpoint also came in 1.4% above analysts’ estimates. Its non-GAAP profit of $1.29 per share was also 13.8% above analysts’ consensus estimates.

Is now the time to buy Adtalem? Find out by accessing our full research report, it’s free.

Adtalem (ATGE) Q3 CY2024 Highlights:

- Revenue: $417.4 million vs analyst estimates of $397.5 million (5% beat)

- Adjusted EPS: $1.29 vs analyst estimates of $1.13 (13.8% beat)

- EBITDA: $96.7 million vs analyst estimates of $86.65 million (11.6% beat)

- The company lifted its revenue guidance for the full year to $1.71 billion at the midpoint from $1.68 billion, a 1.8% increase

- Gross Margin (GAAP): 55.4%, up from 54.3% in the same quarter last year

- Operating Margin: 16.8%, up from 14.3% in the same quarter last year

- EBITDA Margin: 23.2%, up from 21.8% in the same quarter last year

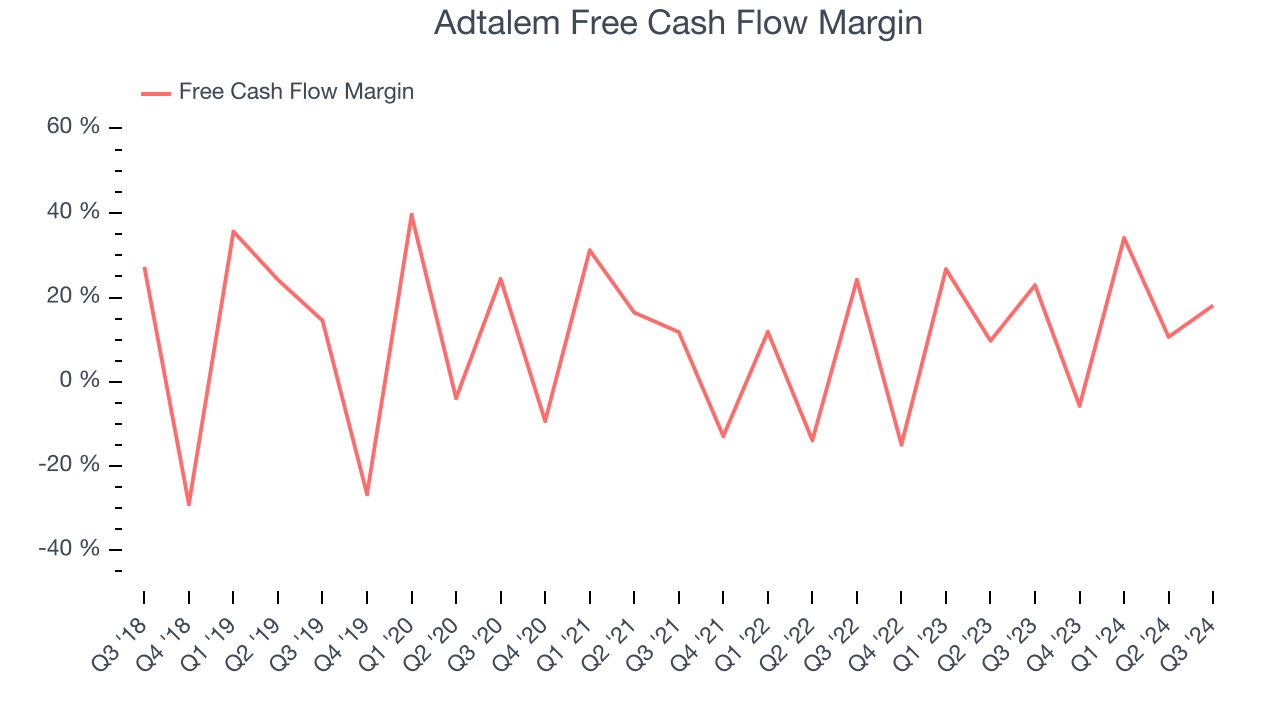

- Free Cash Flow Margin: 18.1%, down from 22.9% in the same quarter last year

- Market Capitalization: $2.77 billion

“We entered year two of our three-year Growth with Purpose strategy with strong momentum, further integrating our tech-enabled platform and expanding our impact through innovative partnerships,” said Steve Beard, President and CEO, Adtalem Global Education.

Company Overview

Formerly known as DeVry Education Group, Adtalem Global Education (NYSE: ATGE) is a global provider of workforce solutions and educational services.

Education Services

A whole industry has emerged to address the problem of rising education costs, offering consumers alternatives to traditional education paths such as four-year colleges. These alternative paths, which may include online courses or flexible schedules, make education more accessible to those with work or child-rearing obligations. However, some have run into issues around the value of the degrees and certifications they provide and whether customers are getting a good deal. Those who don’t prove their value could struggle to retain students, or even worse, invite the heavy hand of regulation.

Sales Growth

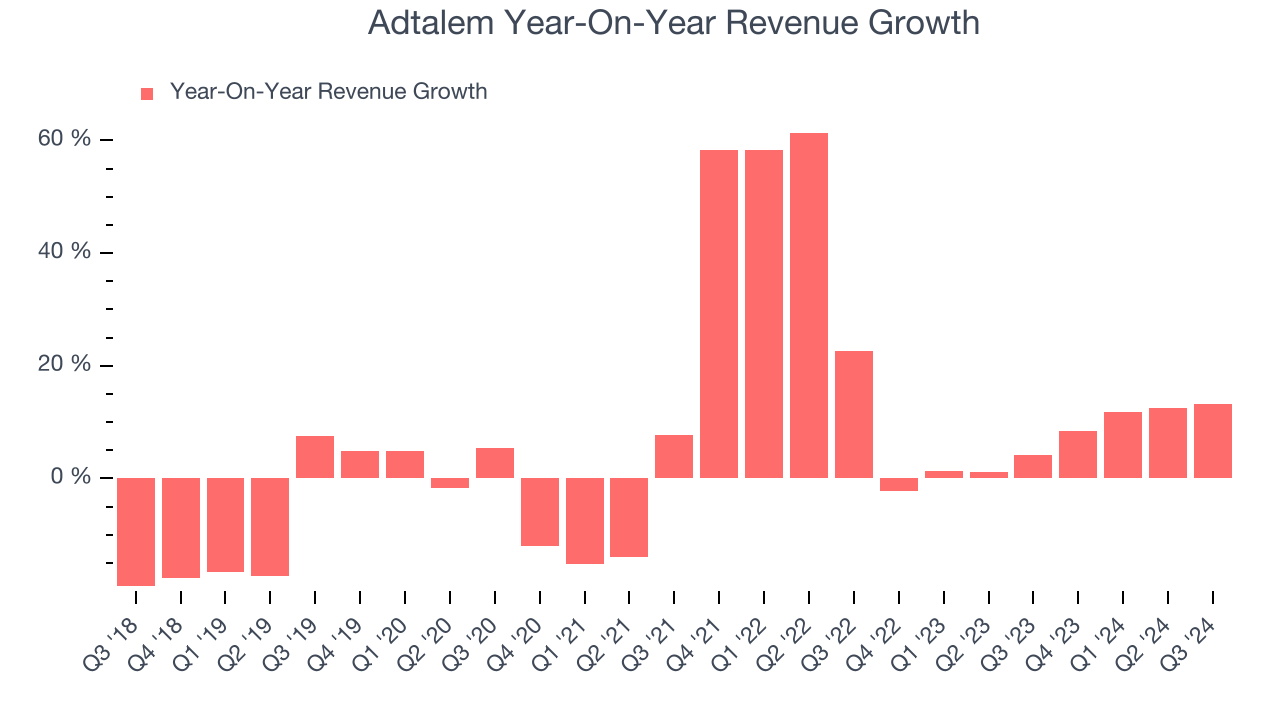

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Adtalem grew its sales at a tepid 9.6% compounded annual growth rate. This shows it failed to expand in any major way, a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Adtalem’s recent history shows its demand slowed as its annualized revenue growth of 6.1% over the last two years is below its five-year trend.

This quarter, Adtalem reported year-on-year revenue growth of 13.2%, and its $417.4 million of revenue exceeded Wall Street’s estimates by 5%.

Looking ahead, sell-side analysts expect revenue to grow 3.9% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and illustrates the market believes its products and services will see some demand headwinds.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Adtalem has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 13% over the last two years, slightly better than the broader consumer discretionary sector.

Adtalem’s free cash flow clocked in at $75.68 million in Q3, equivalent to a 18.1% margin. The company’s cash profitability regressed as it was 4.8 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends trump temporary fluctuations.

Over the next year, analysts’ consensus estimates show they’re expecting Adtalem’s free cash flow margin of 14.6% for the last 12 months to remain the same.

Key Takeaways from Adtalem’s Q3 Results

We enjoyed seeing Adtalem exceed analysts’ revenue, EBITDA, and EPS expectations this quarter. We were also excited it lifted its full-year revenue guidance. Overall, this quarter had some key positives. The stock traded up 2.7% to $77.01 immediately following the results.

So should you invest in Adtalem right now?The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.