Lifestyle clothing conglomerate VF Corp (NYSE: VFC) reported Q3 CY2024 results beating Wall Street’s revenue expectations, but sales fell 5.6% year on year to $2.76 billion. On the other hand, next quarter’s revenue guidance of $2.73 billion was less impressive, coming in 1.9% below analysts’ estimates. Its non-GAAP profit of $0.60 per share was also 60.4% above analysts’ consensus estimates.

Is now the time to buy VF Corp? Find out by accessing our full research report, it’s free.

VF Corp (VFC) Q3 CY2024 Highlights:

- Revenue: $2.76 billion vs analyst estimates of $2.71 billion (1.8% beat)

- Adjusted EPS: $0.60 vs analyst estimates of $0.37 (60.4% beat)

- EBITDA: $317.9 million vs analyst estimates of $281.2 million (13.1% beat)

- Revenue Guidance for Q4 CY2024 is $2.73 billion at the midpoint, below analyst estimates of $2.78 billion

- Gross Margin (GAAP): 52.2%, up from 49.4% in the same quarter last year

- Operating Margin: 9.9%, down from 12.4% in the same quarter last year

- EBITDA Margin: 11.5%, down from 14.6% in the same quarter last year

- Free Cash Flow was -$322.4 million compared to -$217.4 million in the same quarter last year

- Constant Currency Revenue fell 6% year on year (compared to -4% in the same quarter last year)

- Market Capitalization: $6.51 billion

Bracken Darrell, President and CEO, said: "Our results in the quarter met our expectations and reflect a sequential and broad-based improvement in year-on-year trends. At the same time, we made further progress on our four Reinvent priorities and we are on track to reach our previously announced $300 million savings target by the end of FY25. Following the completion of the Supreme divestiture on October 1, 2024, we delivered on our commitment to pay down VF’s $1 billion term loan due December 2024. Our Americas regional platform is fully operational and showing promising signs, while the performance at Vans is improving. In summary, we advanced our turnaround plan towards a return to growth and strong, sustainable value creation at VF."

Company Overview

Owner of The North Face, Vans, and Supreme, VF Corp (NYSE: VFC) is a clothing conglomerate specializing in branded lifestyle apparel, footwear, and accessories.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

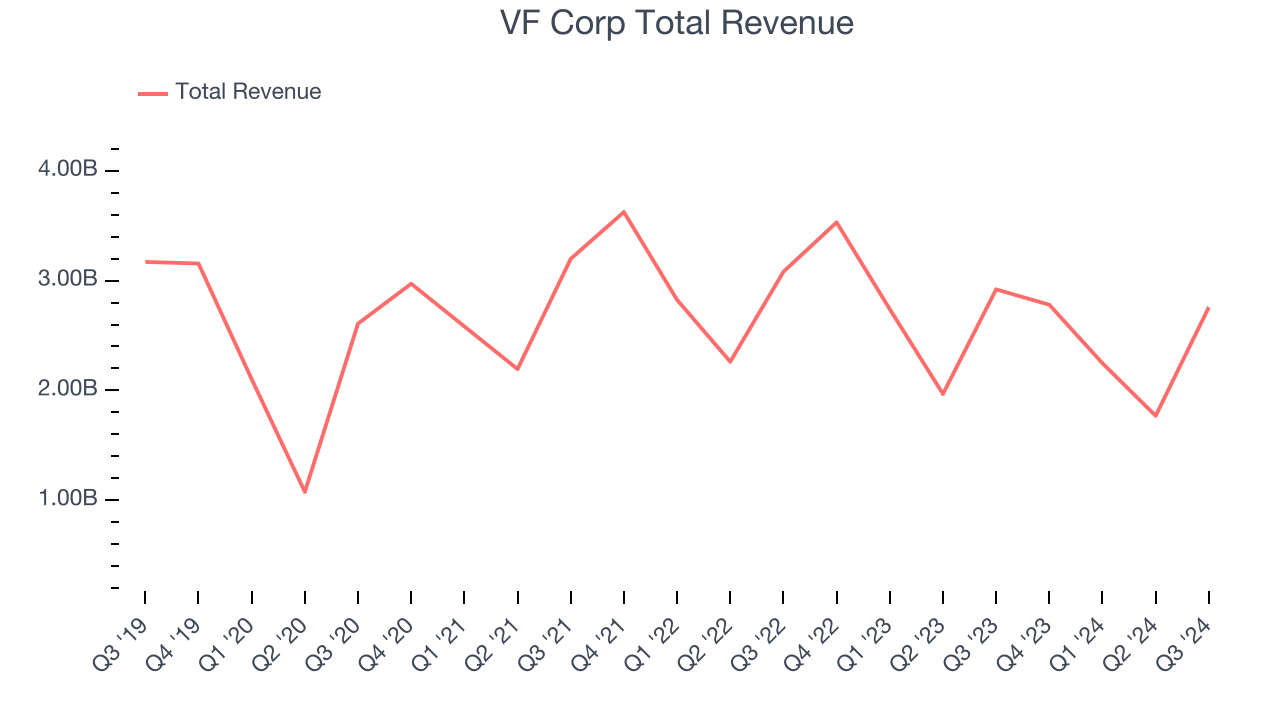

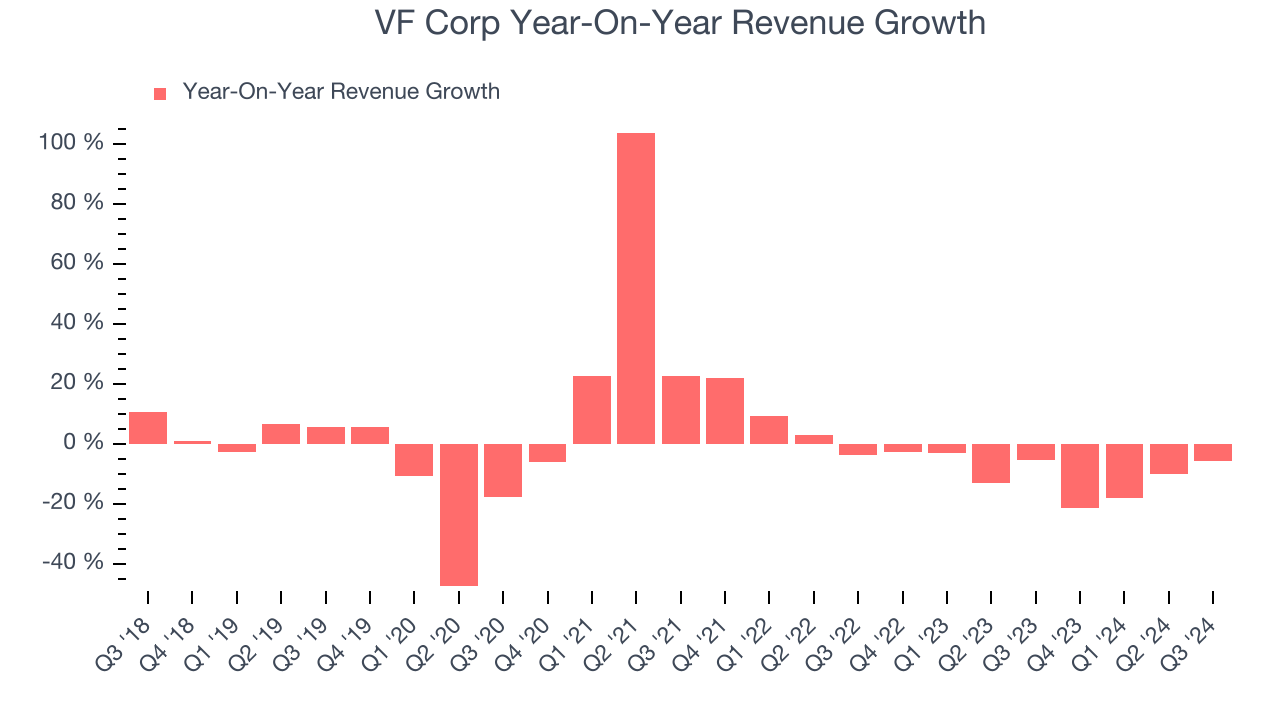

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. VF Corp struggled to generate demand over the last five years as its sales dropped by 2% annually, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. VF Corp’s recent history shows its demand has stayed suppressed as its revenue has declined by 10% annually over the last two years.

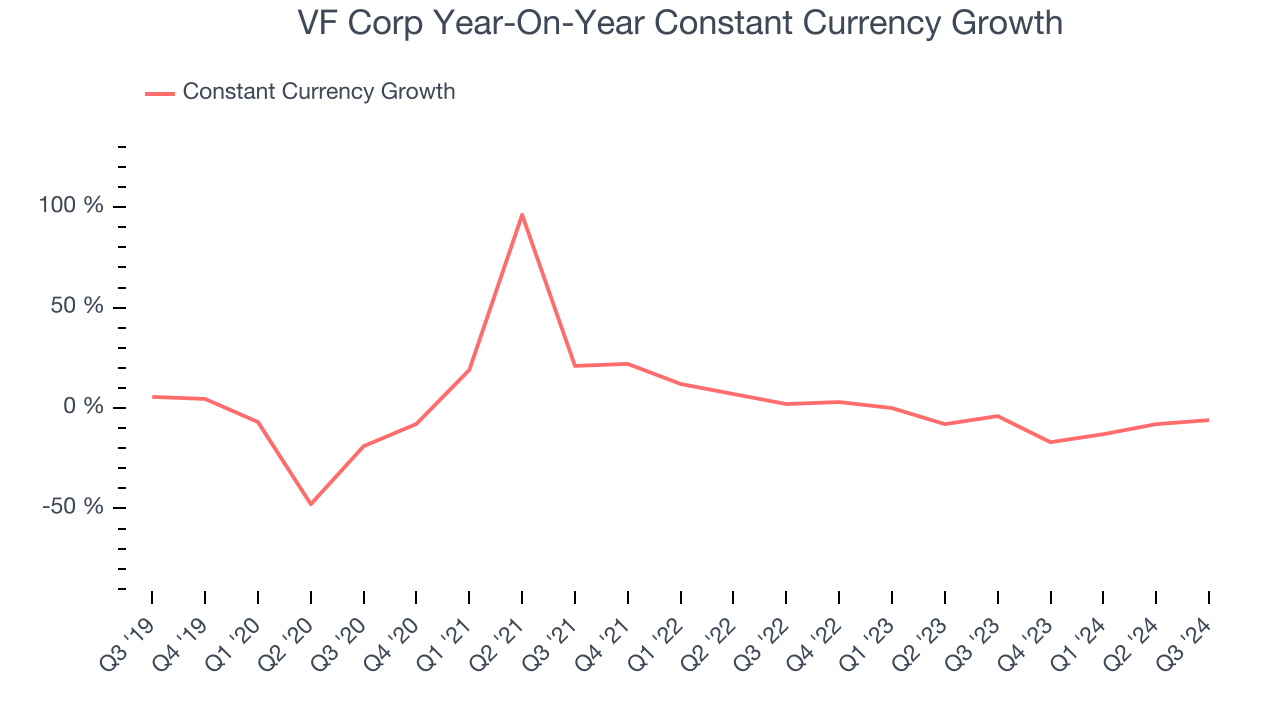

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 6.6% year-on-year declines. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for VF Corp.

This quarter, VF Corp’s revenue fell 5.6% year on year to $2.76 billion but beat Wall Street’s estimates by 1.8%. Management is currently guiding for a 2% year-on-year decline next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.4% over the next 12 months. While this projection indicates the market believes its newer products and services will spur better performance, it is still below the sector average.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

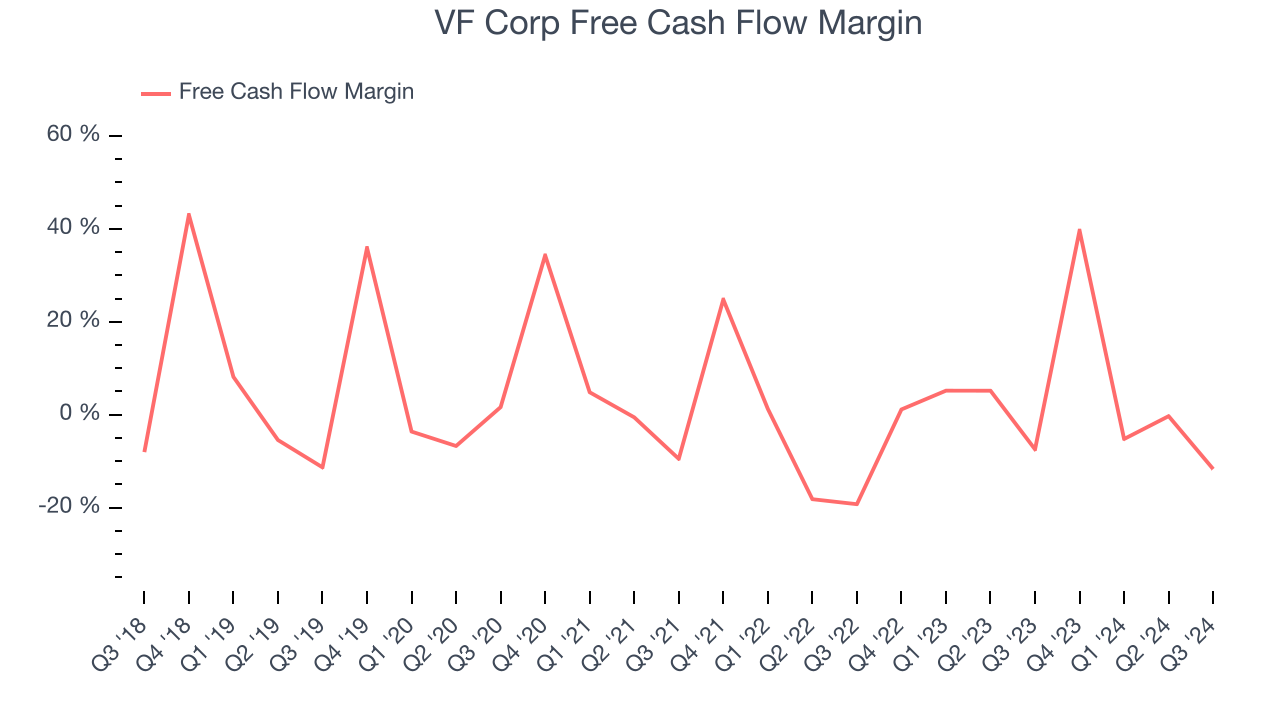

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

VF Corp has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.5%, lousy for a consumer discretionary business.

VF Corp burned through $322.4 million of cash in Q3, equivalent to a negative 11.7% margin. The company’s cash burn increased from $217.4 million of lost cash in the same quarter last year . These numbers deviate from its longer-term margin, raising some eyebrows.

Over the next year, analysts predict VF Corp will flip from cash-producing to cash-burning. Their consensus estimates imply its free cash flow margin of 6.9% for the last 12 months will decrease to negative 1.2%.

Key Takeaways from VF Corp’s Q3 Results

We were impressed by how significantly VF Corp blew past analysts’ EBITDA and EPS expectations this quarter. We were also glad its constant currency revenue outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter was underwhelming, but we still think this was a decent quarter with some key metrics above expectations. The stock traded up 12.9% to $19.22 immediately following the results.

VF Corp may have had a good quarter, but does that mean you should invest right now?We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.