Hiring the wrong financial advisor doesn't just cost money — it costs time, momentum, and sometimes the trust of your own leadership team. Yet many business owners still choose an advisor the same way they'd choose a barber: based on a referral, a friendly first meeting, and a bit of hope. That approach might work out fine. It might also leave you with a mismatched advisor for two or three years before anyone notices the fit was wrong.

Choosing a financial advisor for your business is a different exercise than choosing one for your personal retirement account. The stakes are higher, the scope is broader, and the wrong advice can ripple through cash flow, tax exposure, and growth decisions for years. This guide walks through exactly what to look for, what to ask, and how to vet a candidate before you sign anything — so the decision holds up under scrutiny, not just under a good first impression.

What Does a Business Financial Advisor Actually Do?

A business financial advisor's core job is to help you make informed decisions about money — not just track it, but plan around it. That typically includes cash flow strategy, financial forecasting, capital structuring (how you fund growth, whether through debt, equity, or reinvested profit), and risk management around things like currency exposure, interest rate changes, or concentration risk in your client base.

Coleman Financial Group, for example, is structured around this combined advisory-and-consulting model, giving business owners a single point of contact for both financial strategy and day-to-day accounting needs in Australia. That kind of continuity can matter significantly during periods of transition, when a business needs its financial and operational advice to be consistent rather than pieced together from multiple sources.

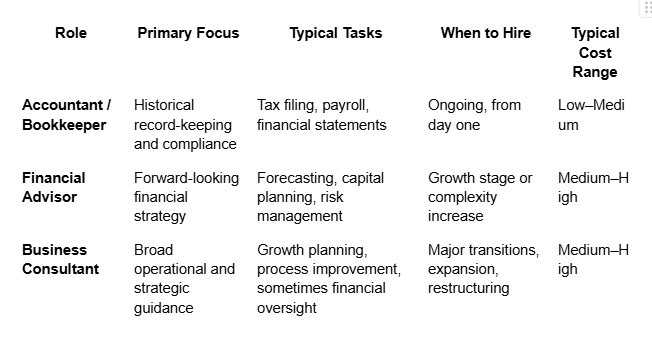

What a financial advisor is not is often just as important to understand. A financial advisor is not the same as an accountant, and it's not the same as a general business consultant, even though the roles overlap and the titles get used loosely in casual conversation.

In practice, many businesses eventually need all three, though rarely at the same time or in the same proportions.

Signs Your Business Needs a Financial Advisor

Not every business needs a financial advisor immediately, and there's no shame in running lean with just an accountant early on. But certain signals tend to show up consistently right before businesses realize they've outgrown that setup.

Revenue growth is outpacing your internal financial controls. If your spreadsheets can't keep up with your bank statements, that's a signal.

You're preparing for a raise, loan application, or acquisition. Lenders and investors want forecasts, not just history.

Succession or exit planning is on the horizon, even years away.

Cash flow is unpredictable despite steady or growing revenue.

You're expanding into new markets, entities, or jurisdictions and the tax and structuring questions have gotten more complex than a general accountant typically handles.

If two or more of these apply to your business right now, it's a reasonable moment to start the search — not necessarily to hire tomorrow, but to begin vetting candidates before the need becomes urgent.

Types of Financial Advisors for Businesses

Not all financial advisors operate the same way, and the differences matter more than most first-time buyers of these services realize.

Fee-Only Fiduciary Advisors

These advisors charge a flat fee, hourly rate, or retainer, and are legally obligated to act in your best interest. There's no product they're incentivized to sell you.

Commission-Based Advisors

These advisors earn income from the financial products they recommend — insurance policies, investment vehicles, certain lending products. This isn't automatically a red flag, but it introduces a conflict of interest worth understanding upfront.

Fractional CFOs

A fractional CFO acts as a part-time, outsourced version of a full-time Chief Financial Officer. This model has grown quickly among mid-sized businesses that need CFO-level strategy without a six-figure full-time salary commitment.

Business Consulting Firms with Financial Specialization

Some firms combine financial advisory work with broader business consulting — useful for businesses that want one relationship covering both financial strategy and operational guidance, rather than juggling multiple vendors.

A useful (anonymized) example: a mid-sized services business with roughly $2 million in annual revenue discovered, after two years, that their advisor's product recommendations consistently favored a small number of investment vehicles that paid the advisor a commission — regardless of whether those products were the best fit for the business's actual risk profile. It wasn't a fraud. It was simply a conflict of interest that had never been disclosed clearly, and it went unnoticed until a second opinion flagged it. That kind of story is common enough that it's worth building your vetting process around avoiding it entirely.

Key Credentials and Qualifications to Look For

Credentials aren't everything, but they're a fast way to filter out unqualified candidates before you invest time in interviews.

CFP (Certified Financial Planner) — broad financial planning credential, often more common in personal finance but relevant for owner-operator businesses.

CFA (Chartered Financial Analyst) — rigorous investment and financial analysis credential, useful for businesses with significant capital allocation decisions.

CPA (Certified Public Accountant) — technically an accounting credential, but many CPAs move into advisory roles and bring strong compliance knowledge with them.

Beyond the letters after someone's name, ask about fiduciary duty specifically. A fiduciary is legally required to act in your best interest; a non-fiduciary is only held to a "suitability" standard, which is a meaningfully lower bar. Regulatory bodies such as ASIC in Australia and the CFP Board in the United States publish clear guidance on what fiduciary standards actually require, and it's worth reading that guidance directly rather than taking an advisor's word for it.

Industry-specific experience also matters more than generic credentials in many cases. An advisor who has spent a decade working with hospitality businesses will understand seasonal cash flow patterns in a way a generalist advisor simply won't.

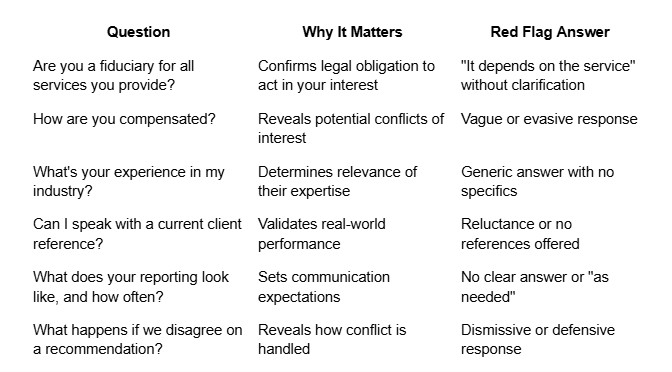

How to Vet a Financial Advisor: A Step-by-Step Process

Step 1 — Define your business's specific financial goals before searching. Are you trying to stabilize cash flow, prepare for a raise, plan an exit, or manage rapid growth? The answer changes who you should be looking for.

Step 2 — Shortlist advisors with relevant industry experience. Ask directly: "How many businesses like mine have you advised in the last three years?" Vague answers here are worth noting.

Step 3 — Verify credentials and check for disciplinary history. Most credentialing bodies maintain public registries. It takes ten minutes and can save years of regret.

Step 4 — Ask about fee structure and potential conflicts of interest. Get this in writing, not just in conversation.

Step 5 — Request references from similar businesses. Ask references specifically how the advisor handled a disagreement or a mistake — not just how the relationship started.

Step 6 — Evaluate communication style and reporting cadence. A brilliant advisor who's impossible to reach quarterly isn't much use to a business that needs regular financial visibility.

Questions to Ask a Financial Advisor Before Hiring

Understanding Advisor Fee Structures

Fee structures vary widely, and the right one often depends on your business's size and stage.

Flat fee — a fixed amount for a defined scope of work; predictable and easy to budget.

Hourly — billed per hour of consultation; can work well for one-off projects but is harder to predict for ongoing relationships.

Percentage-of-assets — common for advisors managing investment portfolios; less common for pure business advisory work.

Retainer — a recurring fee for ongoing access and advisory support; common for fractional CFO arrangements.

Smaller businesses often do better with flat-fee or hourly arrangements for defined projects, while larger or fast-growing businesses tend to benefit from retainer models that provide continuous access rather than piecemeal engagement.

Red Flags to Watch For When Choosing a Financial Advisor

Vague or shifting answers about how they're compensated.

Reluctance to put fiduciary status in writing.

One-size-fits-all product recommendations regardless of your specific situation.

No verifiable references, or references that seem rehearsed.

Pressure tactics or urgency ("this rate is only available if you sign this week").

Any one of these alone might have an innocent explanation. Two or more together is usually a sign to keep looking.

Researching an Advisor's Online Presence and Reputation

Vetting an advisor doesn't stop at credentials and references — a growing part of due diligence now happens online, before you ever get on a call. Reviews, published commentary, professional profiles, and how an advisor's firm shows up in search results all contribute to a clearer picture of their credibility and how seriously they're taken within the industry.

This matters more than it used to, because search behavior itself has changed. Business owners increasingly rely on AI-driven search tools and summarized results to do this kind of background research quickly, rather than clicking through a dozen individual websites. A firm with a thin or outdated online footprint isn't automatically untrustworthy, but a well-maintained, accurately represented online presence — the kind supported by proper AI Optimization — does make it easier to verify credentials, read genuine client feedback, and confirm that a firm is who it claims to be before you ever sit down for a first meeting.

When to Consider Working With a Business Consulting Firm Instead of an Individual Advisor

For businesses that need more than isolated financial advice — say, support across tax strategy, forecasting, and long-term growth planning — a consulting firm structure can offer more continuity than a solo practitioner. These firms typically pair financial oversight with broader operational guidance, which can be especially useful for businesses navigating multiple growth stages at once, since it removes the need to coordinate between several disconnected vendors.

How to Evaluate Your Financial Advisor After Hiring

Hiring the right advisor isn't the end of the process — it's the start of an ongoing relationship that needs periodic evaluation.

Set clear KPIs early. These might include forecast accuracy, response time to requests, or measurable improvement in cash flow predictability.

Schedule regular reviews. Quarterly check-ins are common; annual reviews at minimum.

Know when to switch. If communication has degraded, advice has become generic, or you sense a conflict of interest has crept in, it's reasonable to start a new search — even mid-relationship.

Common Mistakes Businesses Make When Choosing a Financial Advisor

Hiring based on referral alone, without independently verifying credentials or references.

Not clarifying scope of engagement in writing, which leads to mismatched expectations later.

Ignoring fee-conflict red flags because the advisor was personable in the first meeting.

Choosing based on price instead of fit, which often costs more in poor advice than it saves in fees.

Frequently Asked Questions

What's the difference between a financial advisor and an accountant?

An accountant primarily handles historical record-keeping, tax filing, and compliance. A financial advisor focuses on forward-looking strategy — forecasting, capital planning, and risk management. Many businesses need both, often at different stages of growth.

How much does a business financial advisor cost?

Costs vary widely based on fee structure and scope, ranging from a few hundred dollars for a single project under an hourly arrangement to several thousand dollars per month for an ongoing retainer or fractional CFO arrangement.

Do small businesses really need a financial advisor?

Not always, and not immediately. Many small businesses operate well with just an accountant in the early stages. The need for a dedicated advisor typically emerges as revenue, complexity, or growth ambitions increase.

What qualifications should a business financial advisor have?

Look for recognized credentials such as CFP, CFA, or CPA, along with confirmed fiduciary status and demonstrable experience in your specific industry.

Is it better to hire an individual advisor or a consulting firm?

It depends on your needs. An individual advisor can offer a more personal relationship, while a consulting firm often provides broader service coverage and continuity if a single advisor leaves or is unavailable.

How often should I meet with my business financial advisor?

Quarterly is a common minimum for active engagements, though fast-growing or complex businesses often benefit from monthly check-ins.

What's a fiduciary advisor, and why does it matter for my business?

A fiduciary is legally obligated to act in your best interest, rather than simply recommending "suitable" products. This distinction significantly reduces the risk of conflict-of-interest-driven advice.

Can my accountant also act as my financial advisor?

Some accountants do expand into advisory services, particularly CPAs with additional financial planning credentials. It's worth asking directly whether they hold fiduciary status for the advisory portion of their work, since accounting and advisory responsibilities carry different standards.

Final Thoughts

Choosing a financial advisor for your business is a decision that deserves the same rigor you'd apply to hiring a senior employee — because in practice, that's exactly what it is. The right advisor will understand your industry, disclose conflicts of interest openly, communicate on a schedule that actually works for your business, and hold a fiduciary standard that keeps their incentives aligned with yours.

Take the time to define your goals before you start searching, ask the harder questions early, and don't be afraid to walk away from a personable advisor whose fee structure or credentials don't hold up to scrutiny. A strong advisory relationship, built the right way, tends to pay for itself many times over — and a rushed one rarely does.