Broadcom (AVGO), an innovator in the semiconductor solutions industry, has been a value creator with returns of more than 145% in the last 52 weeks. This rally has arrived on the back of AI-driven demand which has translated into top-line growth acceleration coupled with cash flow upside.

Recently, Mizuho Securities reiterated an “Outperform” rating for AVGO stock after a meeting with Broadcom executives. A key reason for the bullish outlook was estimates related to the company's AI revenue trajectory. From consensus estimates of $100 billion for 2027, the AI revenue potential has increased to $120 billion. Further, AI revenue is expected to swell to $132 billion by 2028, implying a three-year compound annual growth rate (CAGR) of 87%.

JPMorgan analyst Harlan Sur has similar views on AVGO stock. With the Meta Platforms (META) agreement, Harlan opines that Broadcom can “significantly exceed $120B+” of AI revenue in fiscal 2027. The business momentum is therefore positive and backed by structural industry tailwinds.

About Broadcom Stock

Headquartered in Palo Alto, California, Broadcom is a developer, designer, and supplier of semiconductor and software technologies. With innovation as the core growth engine, Broadcom has a portfolio of 19,000 patents. Further, in fiscal 2025, the company invested $11 billion in R&D.

Over the years, Broadcom has grown both organically and through acquisitions. For fiscal 2025, the company clocked revenue of $63.9 billion with infrastructure software and semiconductor solutions being the two business segments. For the year, adjusted EBITDA and free cash flow also came in at $43 billion and $26.9 billion, respectively.

With accelerating AI-driven semiconductor revenue coupled with multi-year deals with hyperscalers, Broadcom is positioned for sustained growth and value creation.

In the last six months, AVGO stock has trended higher by 23%. Considering the impending growth, it’s likely that the stock uptrend will sustain. Broadcom has also created value through dividends and, between fiscal 2016 and fiscal 2026, the company’s dividend payout has grown at a CAGR of 30%.

Clear Revenue Visibility

Long-term chip supply agreements remain a key bullish factor for Broadcom. The agreements provide clear revenue and cash flow visibility. In April 2026, Broadcom and Alphabet's (GOOGL) Google signed an agreement to supply custom AI chips and other components through 2031. Additionally, Google and Broadcom will be facilitating Anthropic’s access to 3.5 gigawatts of TPU capacity expected to come online in 2027.

More recently, Broadcom announced an extended partnership with Meta for technology deployment to support multiple gigawatts of “Meta Training and Inference Accelerator (MTIA) chips” through 2029. As Broadcom partners with some of the biggest hyperscalers, there is visibility for accelerated top-line growth in the next few years.

From a financial perspective, Broadcom also reported free cash flow of $8 billion in the first quarter of fiscal 2026. This implies an annualized FCF potential of $32 billion. With robust growth, it’s likely that FCF will be in excess of $50 billion in the next few years. This will position Broadcom for continued dividend growth coupled with aggressive share repurchases.

What Do Analysts Think About AVGO Stock?

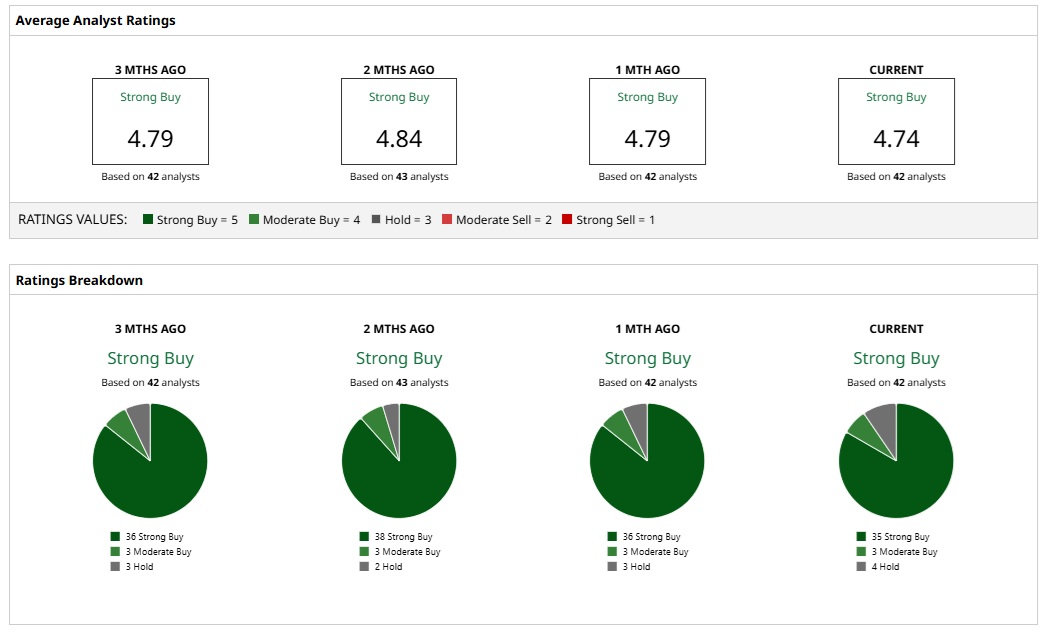

Based on 42 analysts with coverage, AVGO stock has a consensus “Strong Buy” rating. An overwhelming majority of 35 analysts have a “Strong Buy” rating for AVGO stock. Further, three analysts have a “Moderate Buy” while four analysts have a “Hold” rating. Currently, there are no bearish analyst views on the stock.

The mean price target of $469.94 represents potential upside of about 12% from current levels. The most bullish price target of $630 suggests that AVGO stock could climb 50% from here.

From a valuation perspective, AVGO stock trades at a forward price-to-earnings (P/E) ratio of 40.1 times. Valuations might seem stretched, but a P/E-to-growth ratio of 0.83 times points to robust earnings growth potential and headroom for stock upside.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Dividend Stock Keeps Hitting It Out of the Park: Should You Buy?

- Should You Buy the Dip in United Airlines Stock?

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?