Cathie Wood’s ARK Invest has been steadily dialing down its exposure to mega-cap tech, trimming names like Nvidia (NVDA), Meta (META), AMD (AMD), and Tesla (TSLA) amid valuation and regulatory concerns. But at the same time, the firm is rotating capital into smaller, high-upside opportunities. Recently, it added nearly 48,700 shares of Arcturus Therapeutics (ARCT) worth roughly $344,505.

Let’s find out why.

Why Might ARK Be Buying Arcturus Stock Now?

Arcturus Therapeutics is a biotech company that operates in the mRNA space, developing therapies and vaccines using its proprietary RNA platform. This is quite similar to the concept of what powered the Covid-era success of companies like Moderna (MRNA).

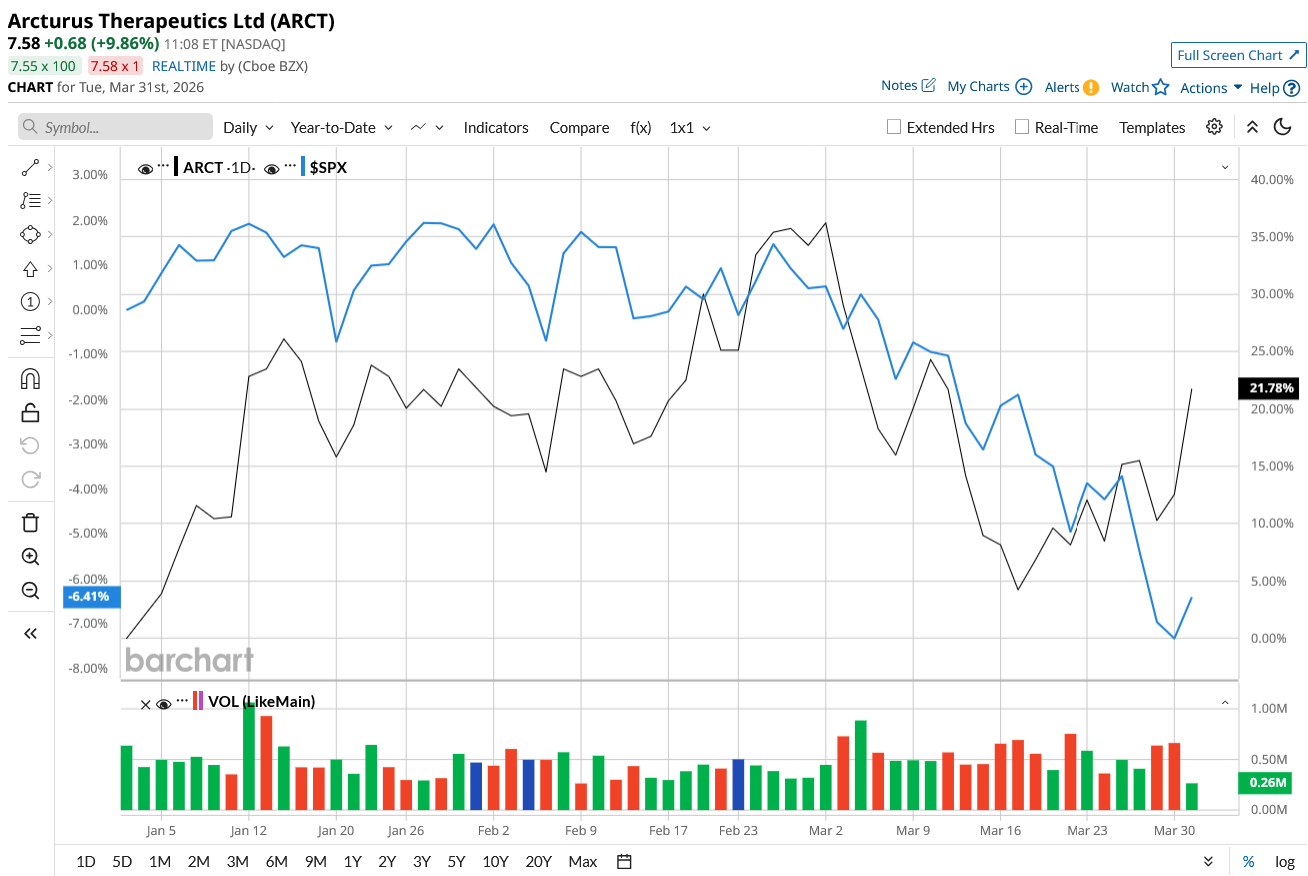

However, Arcturus is a smaller player with a market cap of just $196.1 million. The stock has been under pressure this last month. While ARCT is up 22% year-to-date (YTD), compared to the S&P 500 Index ($SPX) dip of 6%, the stock has fallen over 6% in March alone. For contrarian investors like Cathie Wood, this is an opportunity to buy high-conviction stocks during a market sell-off. Arcturus now holds 1.8% weightage in the ARK Genomic Revolution ETF (ARKG).

ARK’s investment strategy has always centered on disruptive growth opportunities, particularly in areas like biotech. Arcturus develops mRNA-based medicines and vaccines, mainly targeting rare diseases like cystic fibrosis and liver disorders, along with infectious diseases. The company’s two lead programs, ARCT-032 for cystic fibrosis and ARCT-810 for ornithine transcarbamylase deficiency, are central to its growth strategy. Notably, in the first half of 2026, the company plans to launch a 12-week Phase 2 trial for high-dose testing of ARCT-032, an inhaled mRNA treatment for cystic fibrosis. This study will assess both safety and early indicators of clinical benefit over a longer time frame than previous cohorts.

Furthermore, Arcturus is developing ARCT-810, an mRNA therapy for ornithine transcarbamylase deficiency, a rare and dangerous liver condition. It plans to treat both adults and young children, particularly those who now rely on liver transplants to survive. It will also collaborate with regulators in 2026 to decide the next steps in clinical testing and development.

In vaccines, its self-amplifying mRNA Covid-19 vaccine, KOSTAIVE, has already been authorized and commercialized. It is also developing ARCT-2304, a next-generation pandemic influenza vaccine candidate in Phase 1 trials, funded by BARDA. Arcturus generates revenue primarily through licensing and consultancy fees, as well as any collaborative revenue generated by its agreements with other biotech companies. Total revenue for 2025 fell to $82.0 million, down from $152.3 million in 2024, due to lower activity in its CSL cooperation as the Covid vaccination program moved from development to commercialization, resulting in fewer milestone payments and supply-related sales.

For now, Arcturus remains unprofitable due to rising R&D expenses related to the clinical trials. However, net loss improved to $29.1 million in Q4 from $30.0 million in the prior-year period. For the full year, net loss improved to $65.8 million, compared to $80.9 million in 2024. At the end of the quarter, it had $232.8 million in cash, cash equivalents, and restricted cash. The company anticipates that this cash will finance its operations until the second quarter of 2028. Arcturus thinks that the start of the 12-week Phase II cystic fibrosis study, regulatory alignment for ARCT-810, and sustained success across its vaccination initiatives will drive value creation in the coming years.

A High-Risk, High-Reward Bet

Arcturus Therapeutics fits perfectly into Wood’s investment strategy, which focuses on disruptive innovation, notably in genomics, AI, and next-generation healthcare. However, investors should be aware that the company is not yet profitable. Its future is greatly dependent on clinical trial results, regulatory approvals, and funding conditions.

Arcturus' focus on precision medicine, innovative delivery technologies, and long-term clinical achievements qualifies it as the type of early-stage, high-risk, high-reward biotech story that Cathie Wood is betting on.

Wall Street Expects ARCT Stock to Skyrocket

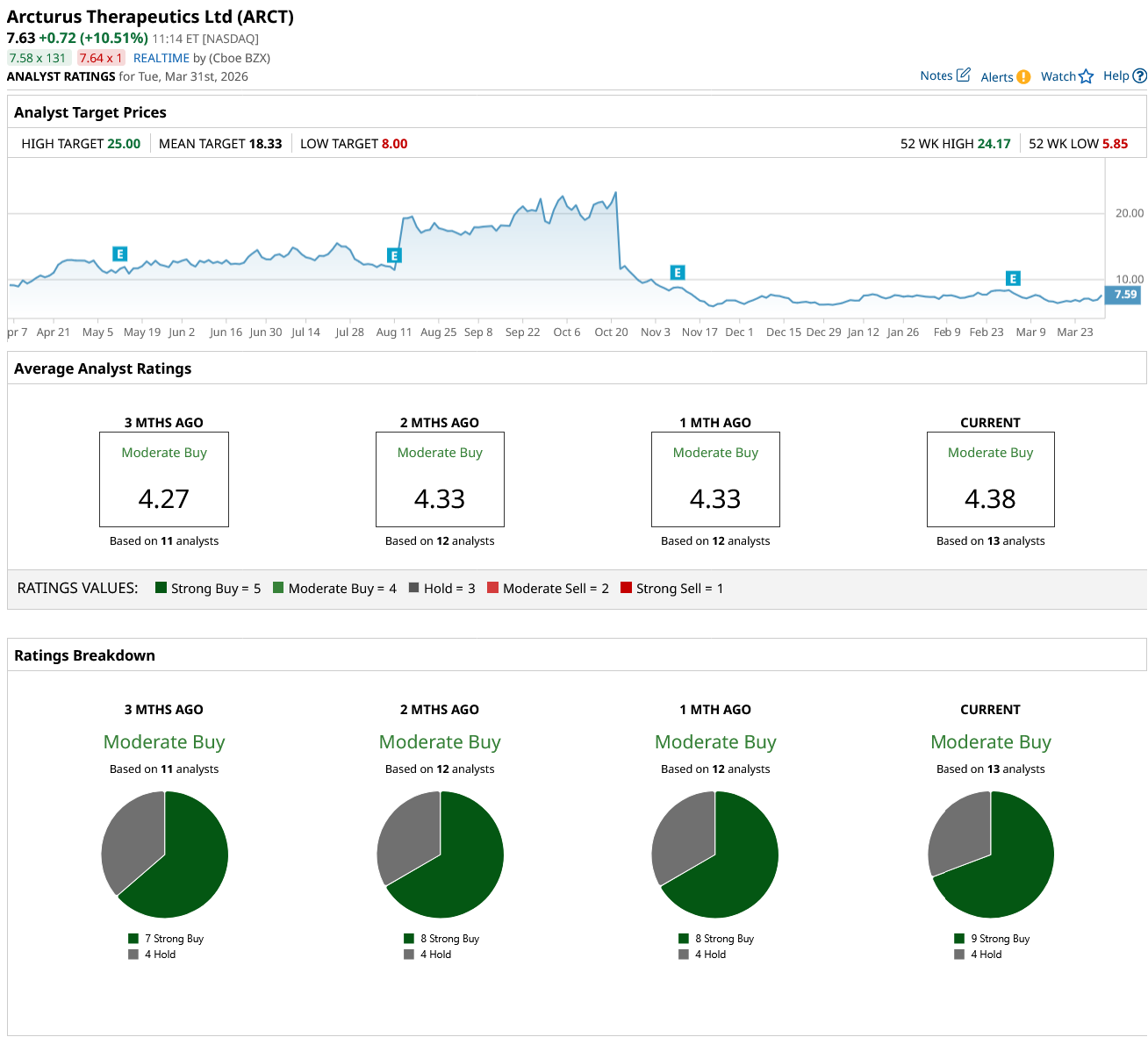

Overall, Wall Street rates ARCT stock a “Moderate Buy.” Out of the 13 analysts covering the stock, nine rate it a “Strong Buy” and four rate it a “Hold.” The average target price of $18.33 suggests the stock can rally as much as 140% over current levels. Plus, the high target price of $25 proposes upside potential of 227% over the next 12 months.

While the upside may seem far-fetched, ARCT stock already reached a 52-week high of $24.17 back on Oct. 21, 2025.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Ignore the Panic and Buy the Dip in Micron Stock, Says Bank of America

- Ignore the TurboQuant Panic and Keep Buying Seagate Technology Stock, Says JPMorgan

- Constellation Energy Just Broke Below Its 50-Day Moving Average. Should You Buy the CEG Stock Dip as Company Misses Guidance?

- Energy Prices Could Soon ‘Skyrocket.’ Why Cheniere Is One of the Top-Rated Stocks to Buy Now.