Over the past six months, Match Group has been a great trade, beating the S&P 500 by 11%. Its stock price has climbed to $38.20, representing a healthy 20.3% increase. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Match Group, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

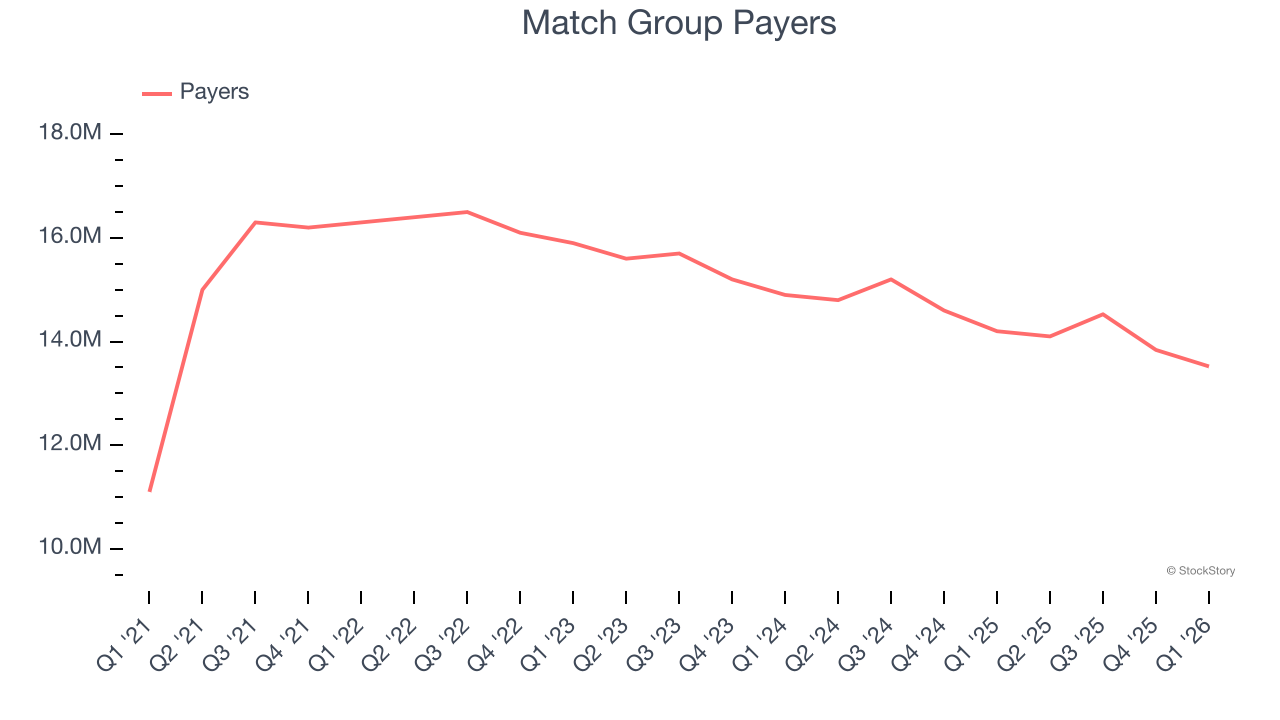

Why Is Match Group Not Exciting?

We’re happy investors have made money, but we’re swiping left on Match Group for now. Here are three reasons we avoid MTCH, plus one stock we’d rather own.

1. Declining Payers Reflect Product Weakness

As a subscription-based app, Match Group generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Match Group struggled with new customer acquisition over the last two years as its payers have declined by 4.5% annually to 13.52 million in the latest quarter. This performance isn’t ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Match Group wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

2. Customer Spending Decreases, Engagement Falling?

Average revenue per user (ARPU) is a critical metric to track because it measures how much the average user spends. ARPU is also a key indicator of how valuable its users are (and can be over time).

Match Group’s ARPU fell over the last two years, averaging 12.1% annual declines. This signals its platform’s value is eroding when paired with its declining payers. If Match Group wants to increase its users, it must either develop new features or provide some existing ones for free.

3. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Match Group’s revenue to drop by 1%, a decrease from This projection is underwhelming and indicates its products and services will see some demand headwinds.

Final Judgment

Match Group isn’t a terrible business, but it isn’t one of our picks. With its shares outperforming the market lately, the stock trades at 9.5× forward EV/EBITDA (or $38.20 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We’re fairly confident there are better investments elsewhere. Let us point you toward one of our top digital advertising picks.

Stocks We Like More Than Match Group

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.