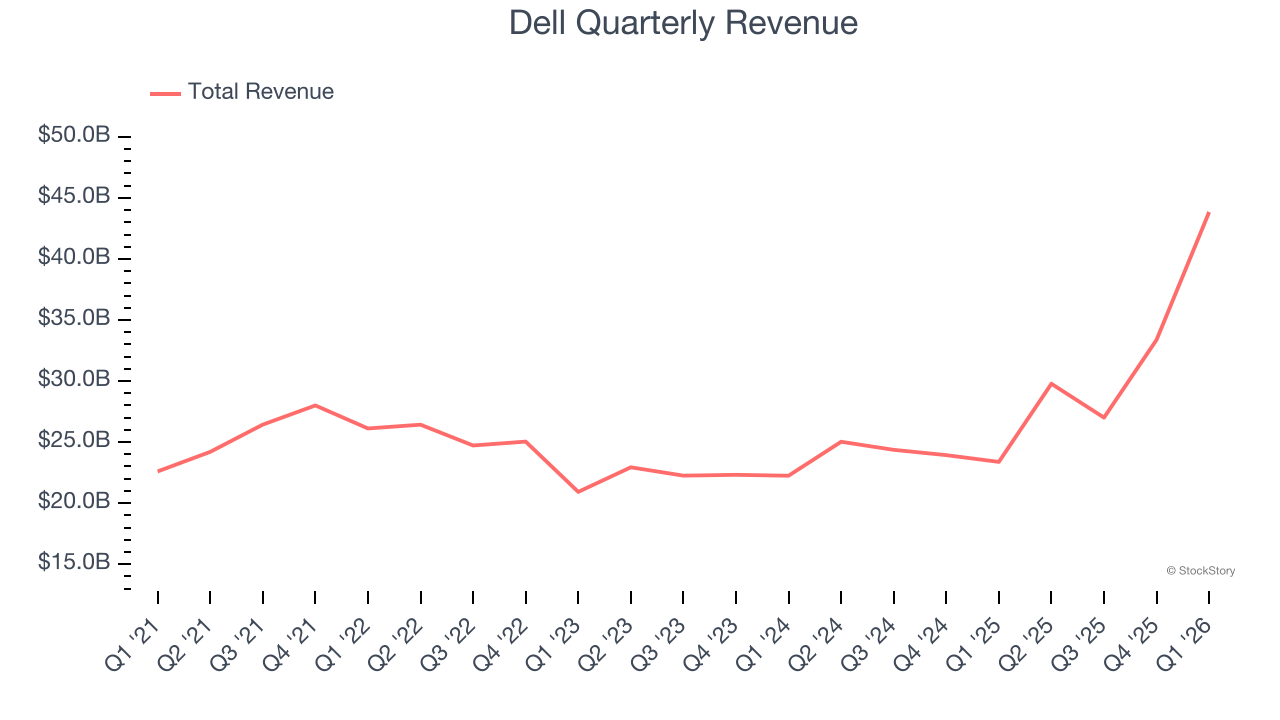

Computer hardware and IT solutions company Dell (NYSE: DELL) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 87.5% year on year to $43.84 billion. On top of that, next quarter’s revenue guidance ($44.5 billion at the midpoint) was surprisingly good and 25.5% above what analysts were expecting. Its non-GAAP profit of $4.80 per share was 62% above analysts’ consensus estimates.

Is now the time to buy Dell? Find out by accessing our full research report, it’s free.

Dell (DELL) Q1 CY2026 Highlights:

- Revenue: $43.84 billion vs analyst estimates of $36.1 billion (87.5% year-on-year growth, 21.5% beat)

- Adjusted EPS: $4.80 vs analyst estimates of $2.96 (62% beat)

- The company lifted its revenue guidance for the full year to $167 billion at the midpoint from $140 billion, a 19.3% increase

- Management raised its full-year Adjusted EPS guidance to $17.90 at the midpoint, a 55.4% increase

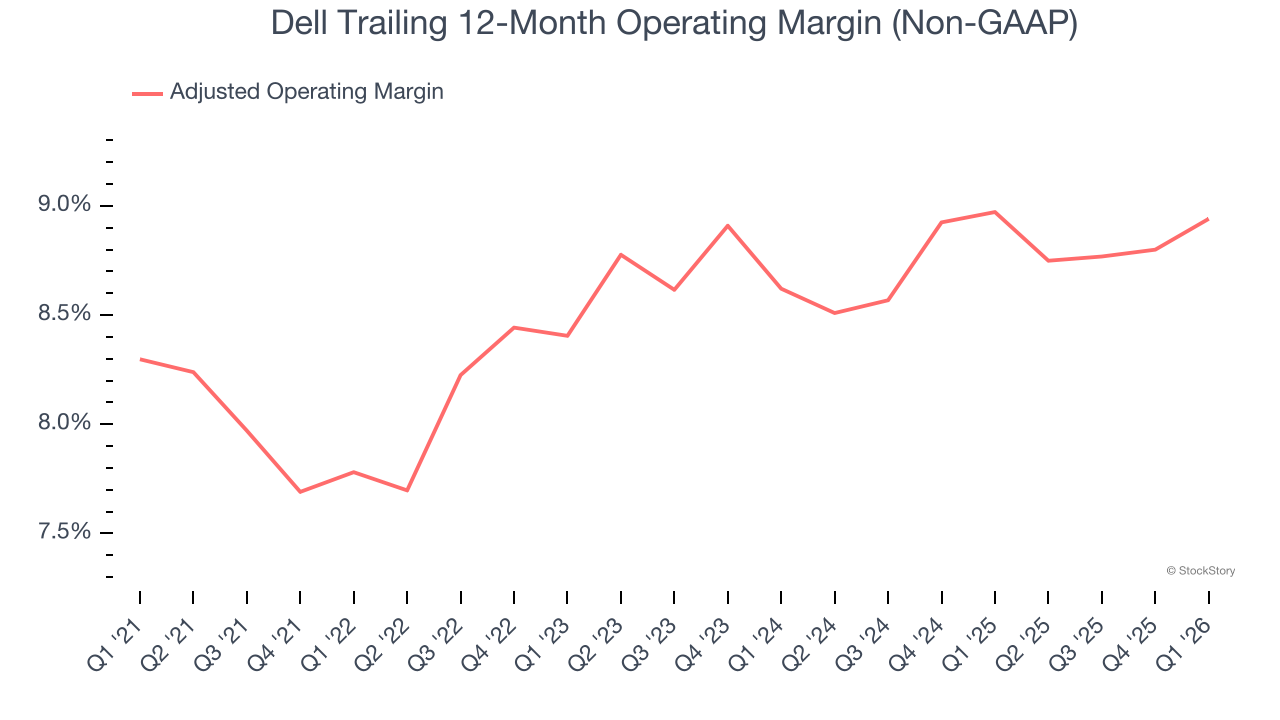

- Operating Margin: 8.3%, up from 5% in the same quarter last year

- Free Cash Flow Margin: 7.1%, down from 9.5% in the same quarter last year

- Market Capitalization: $198.3 billion

“Our record Q1 performance reflects strong in-quarter demand, as well as our pace of innovation across the full stack of PCs, compute and storage,” said Jeff Clarke, vice chairman and chief operating officer, Dell Technologies.

Company Overview

Founded by Michael Dell in his University of Texas dorm room in 1984 with just $1,000, Dell Technologies (NYSE: DELL) provides hardware, software, and services that help organizations build their IT infrastructure, manage cloud environments, and enable digital transformation.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $134 billion in revenue over the past 12 months, Dell is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices.

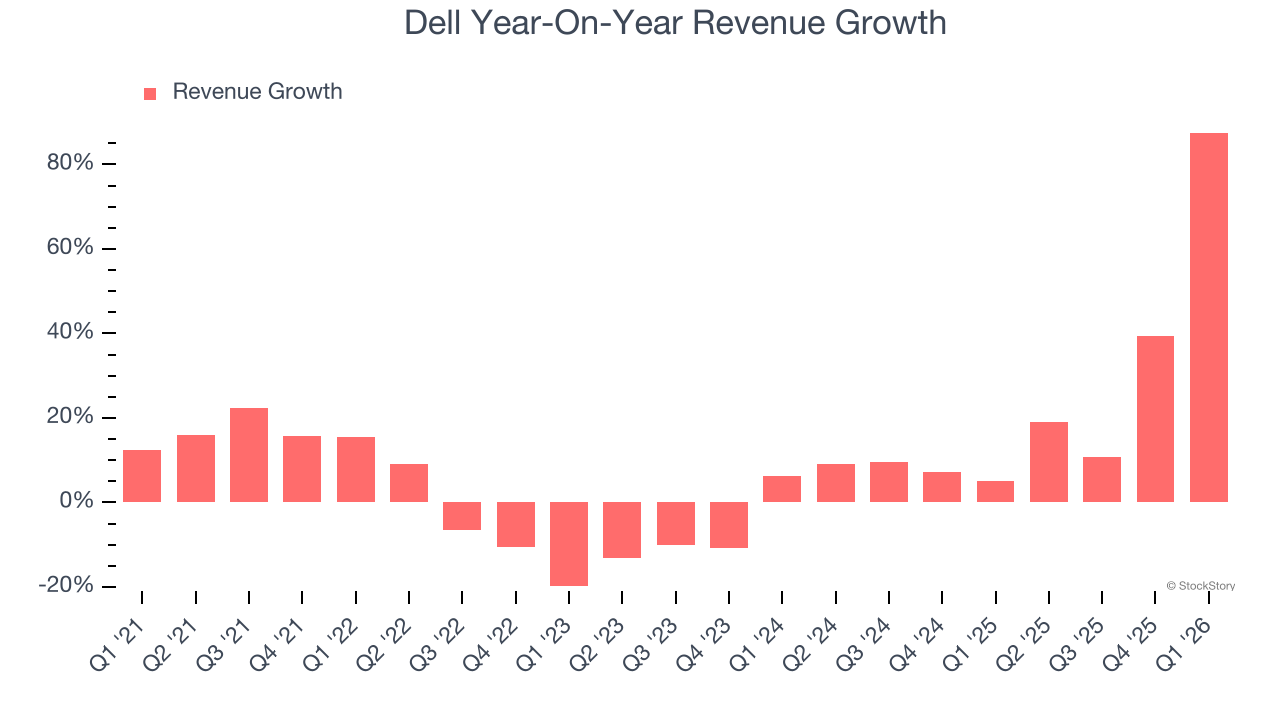

As you can see below, Dell’s 8.5% annualized revenue growth over the last five years was solid. This is a good starting point for our analysis because it shows Dell’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Dell’s annualized revenue growth of 22.2% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Dell reported magnificent year-on-year revenue growth of 87.5%, and its $43.84 billion of revenue beat Wall Street’s estimates by 21.5%. Company management is currently guiding for a 49.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.6% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is attractive given its scale and suggests the market sees success for its products and services.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

Dell was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 8.6% was weak for a business services business.

On the plus side, Dell’s adjusted operating margin rose by 1.2 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, Dell generated an adjusted operating margin profit margin of 8.3%, up 1.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

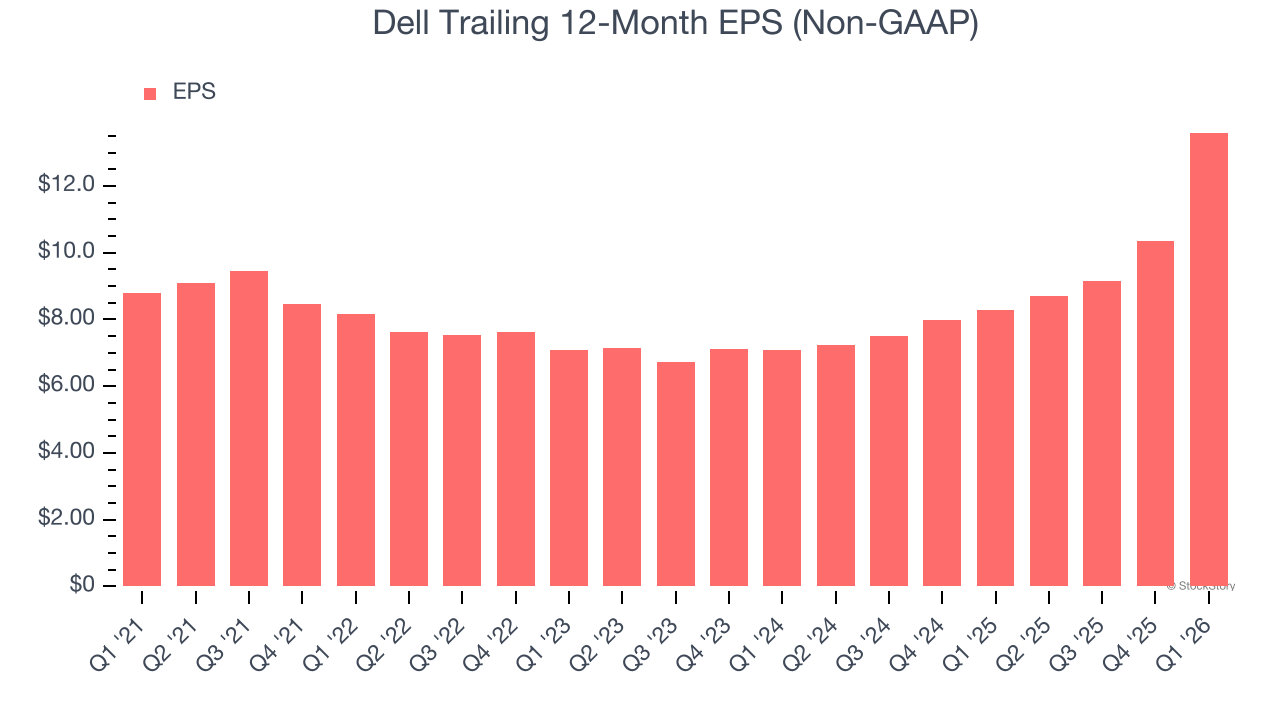

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Dell’s solid 9.1% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Dell’s two-year annual EPS growth of 38.5% was fantastic and topped its 22.2% two-year revenue growth.

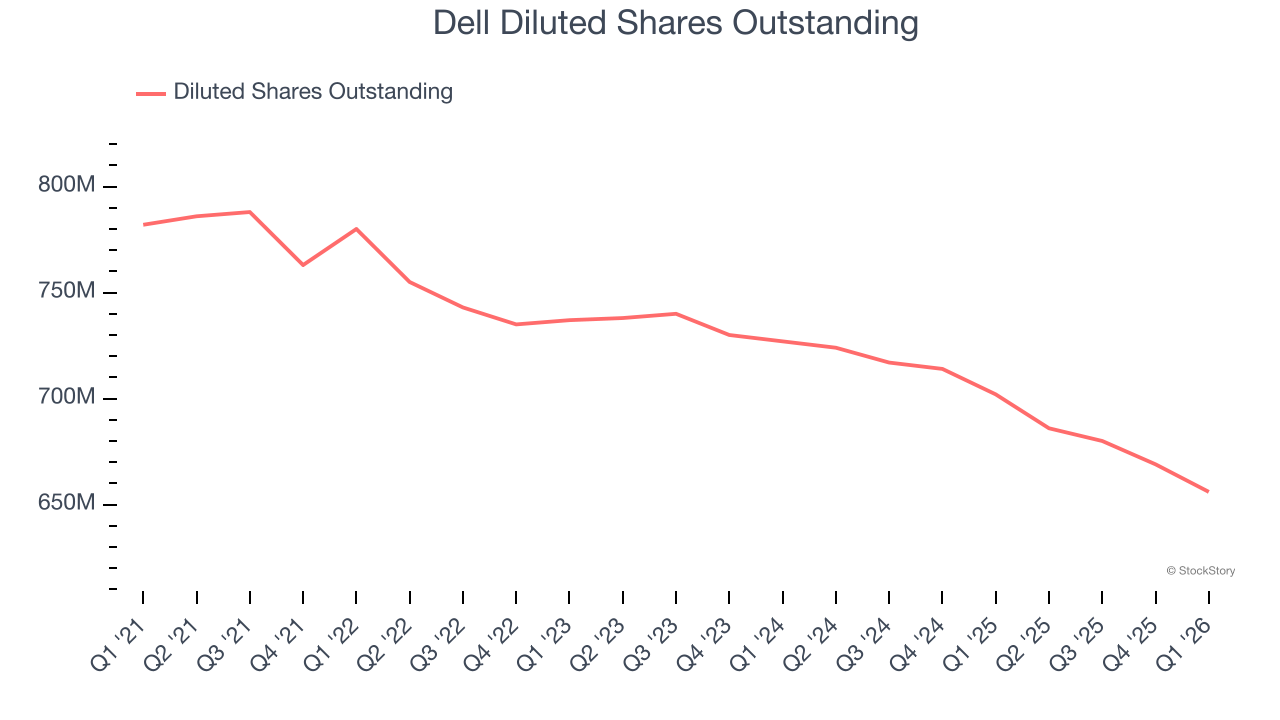

We can take a deeper look into Dell’s earnings to better understand the drivers of its performance. Dell’s adjusted operating margin has expanded over the last two yearswhile its share count has shrunk 9.8%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q1, Dell reported adjusted EPS of $4.80, up from $1.55 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Dell’s full-year EPS to shrink by 2.6% from $13.60 to $13.25.

Key Takeaways from Dell’s Q1 Results

It was good to see Dell beat analysts’ EPS expectations this quarter. We were also excited its EPS guidance for next quarter outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 14.9% to $366.98 immediately after reporting.

Dell had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).