What a time it’s been for Nabors Industries. In the past six months alone, the company’s stock price has increased by a massive 95.4%, reaching $80.12 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Nabors Industries, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Nabors Industries Not Exciting?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons there are better opportunities than NBR and a stock we'd rather own.

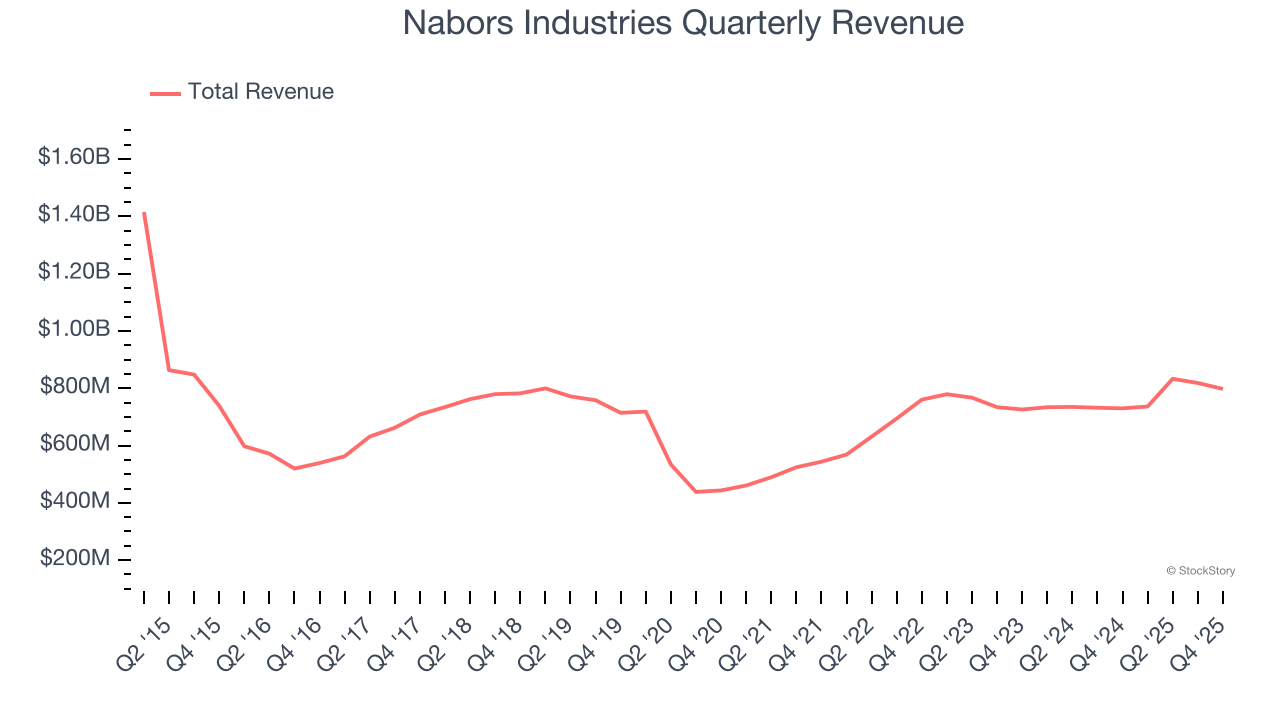

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Unfortunately, Nabors Industries’s 8.3% annualized revenue growth over the last five years was tepid. This fell short of our benchmark for the energy upstream and integrated energy sector.

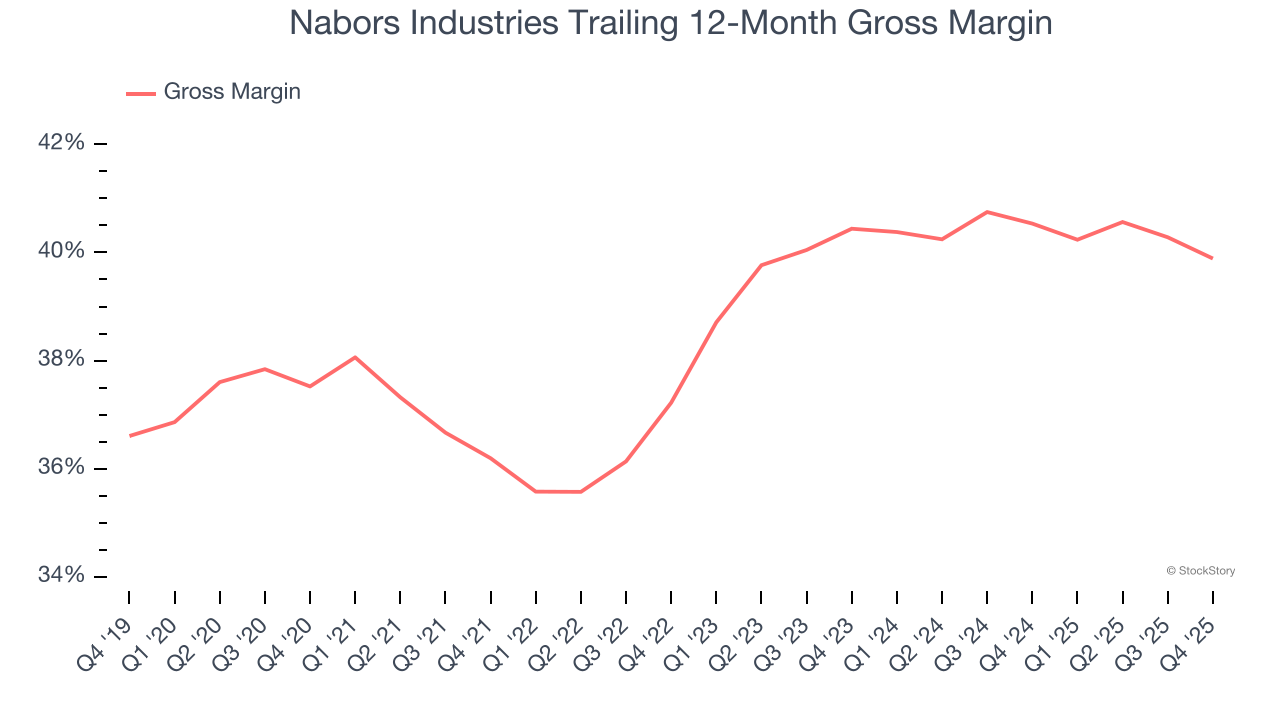

2. Low Gross Margin Reveals Weak Structural Profitability

In any given year, energy gross margins are heavily influenced by prices, hedging, and cost inflation, but over a full cycle these gross margins reveal which producers are structurally advantaged through superior “rock” quality, infrastructure access, and cost position.

Nabors Industries, which averaged 39.1% gross margin over the last five years, exhibits poor unit economics in the sector. It means the company will struggle more at lower commodity prices than peers with better gross margins.

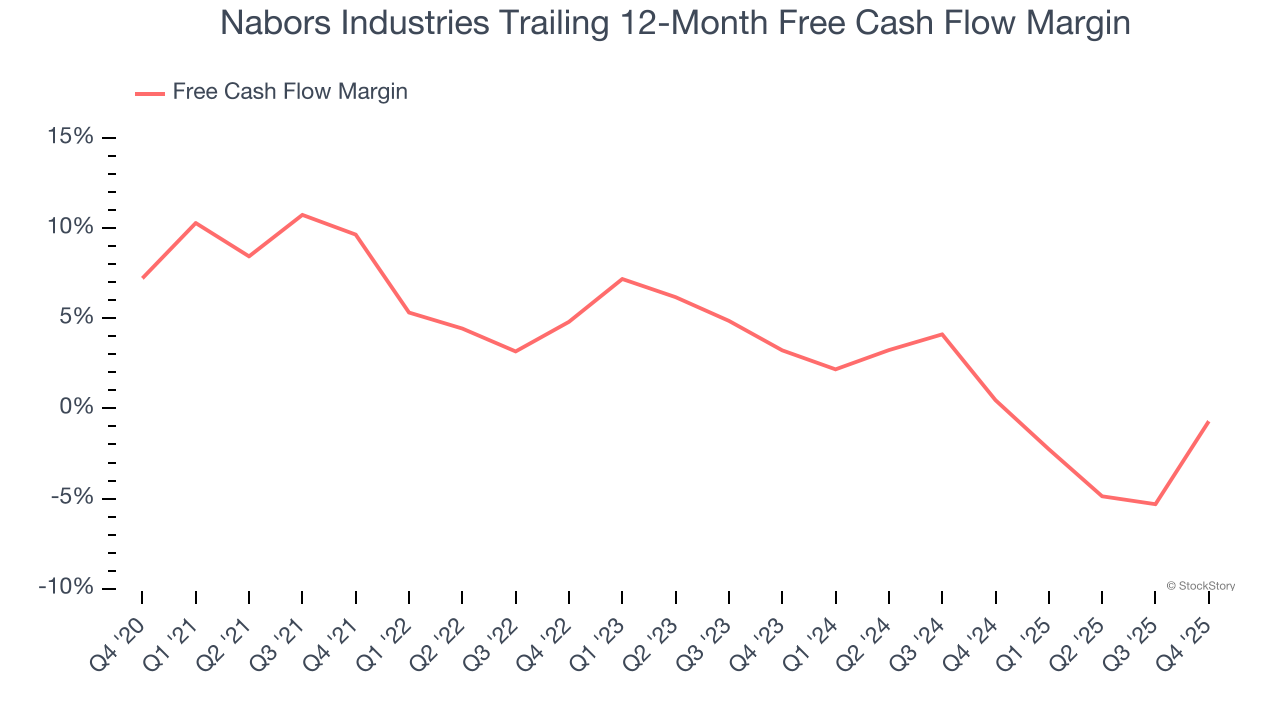

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Nabors Industries has shown weak cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 3%, below what we’d expect for an upstream and integrated energy business.

Final Judgment

Nabors Industries isn’t a terrible business, but it doesn’t pass our quality test. After the recent rally, the stock trades at 3.1× forward EV-to-EBITDA (or $80.12 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better investments elsewhere. Let us point you toward one of our top digital advertising picks.

Stocks We Like More Than Nabors Industries

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.