The dream of a "pivot" to lower interest rates in early 2026 has been dealt a staggering blow following the release of the latest Personal Consumption Expenditures (PCE) price index. On February 23, 2026, investors are grappling with data that confirms inflation is not merely "sticky" but potentially re-accelerating, forcing a massive repricing of risk across global markets. With the Federal Reserve's preferred inflation gauge coming in hotter than expected, the prospect of any meaningful relief from high borrowing costs this year is rapidly evaporating.

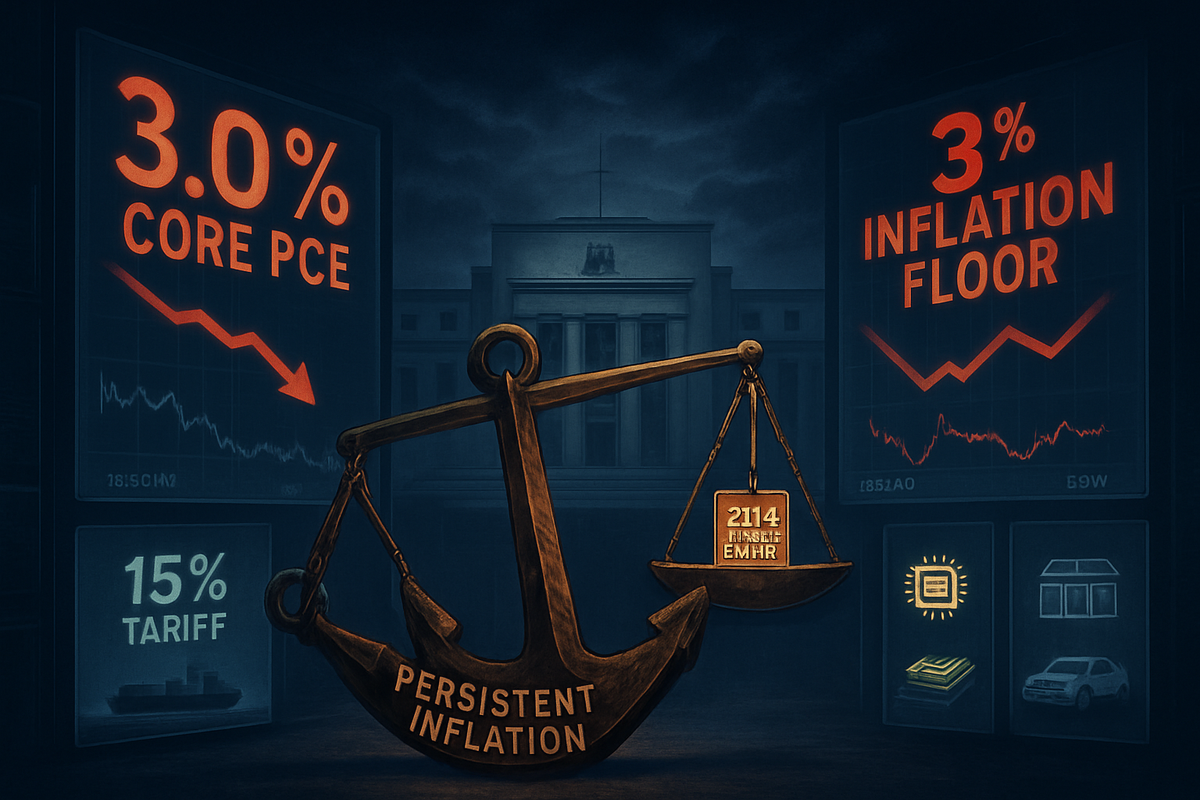

The fallout was immediate and severe. Equities tumbled, with the S&P 500 and the Dow Jones Industrial Average dropping approximately 1.5% in early trading, while the 10-year Treasury yield surged to 4.08%. The combination of persistent price pressures and a newly announced 15% global tariff policy has created a "stagflationary" cocktail that has left Wall Street scrambling to adjust its models for a "higher-for-even-longer" interest rate environment.

A Perfect Storm: Delayed Data and Rising Prices

The latest PCE report, released on February 20, 2026, arrived under unusual circumstances. Due to a 43-day federal government shutdown that paralyzed Washington in late 2025, the data released actually reflects figures for December 2025. Despite the delay, the numbers were sobering. The Core PCE Price Index, which excludes volatile food and energy costs, rose to 3.0% year-over-year, overshooting the 2.9% consensus forecast. Headline PCE followed suit, climbing to 2.9% from the previous quarter’s 2.6%.

Most concerning for policymakers was the "Supercore" inflation metric—services excluding energy and housing. This category surged by 0.6% in January 2026 alone, its sharpest monthly gain in nearly a year. A 6.5% spike in airline fares and climbing medical costs served as the primary drivers. This data suggests that while goods deflation helped lower headline numbers in 2025, the services sector remains overheated, creating a "3% inflation floor" that the Federal Reserve has struggled to break.

The timing of this data release coincides with a precarious leadership transition at the central bank. With Chairman Jerome Powell’s term set to expire in May 2026, the nomination of Kevin Warsh to succeed him has introduced a new layer of uncertainty. While Warsh is seen as market-oriented, his history of inflation hawkishness has led many to believe he will not be in a hurry to cut rates. Federal Reserve Governor Christopher Waller reinforced this sentiment on February 23, noting that a "pause" in March is increasingly likely given the strength of recent employment and inflation data.

Winners and Losers in the High-Rate Era

The persistence of inflation and the prospect of sustained high rates have created a sharp divide between market leaders and laggards. Companies with significant pricing power and fortress balance sheets are emerging as the "winners" of 2026. Berkshire Hathaway (NYSE: BRK.B) continues to benefit from its massive $380 billion cash reserve, which is generating substantial interest income at current yields. Similarly, consumer staples giants like Kraft Heinz (NASDAQ: KHC) and Hormel Foods (NYSE: HRL) have shown resilience; Hormel, with its low beta of 0.33, has become a defensive haven as consumers prioritize essential spending over discretionary items.

In the technology sector, NVIDIA (NASDAQ: NVDA) remains an outlier. Despite the broader market downturn, NVIDIA's role as the indispensable backbone of the AI infrastructure cycle allowed it to report 28% earnings growth in late 2025. Other "AI plumbers" such as Caterpillar (NYSE: CAT) and Eaton (NYSE: ETN) are also seeing continued demand as the construction of massive data centers remains a top priority for hyperscalers, regardless of the interest rate environment.

Conversely, the "losers" list is growing. Retailers like Walmart (NYSE: WMT) and Target (NYSE: TGT) are facing a "double whammy" of 15% global tariffs on imported goods and slowing middle-income spending. The automotive sector is also under fire; Toyota (NYSE: TM) and Stellantis (NYSE: STLA) have each seen earnings hits estimated at over $3 billion due to the combined impact of tariffs on global parts and vehicles. In the high-growth software space, companies like Cloudflare (NYSE: NET) and AppLovin (NASDAQ: APP) are struggling as the higher cost of capital forces investors to demand immediate profitability over future growth projections.

Tariffs, Stagflation, and Policy Shifts

The current economic landscape is being shaped by more than just domestic inflation. The White House's February 21 announcement of a 15% global tariff floor—following a Supreme Court ruling on reciprocal tax measures—has effectively acted as a consumer tax, further complicating the Fed's mission. These tariffs are expected to push costs higher for a wide range of imported goods, potentially fueling another wave of supply-side inflation just as the Fed was hoping to declare victory.

This shift fits into a broader global trend of protectionism and the "re-shoring" of supply chains, which historically leads to higher structural inflation. Compared to the low-inflation environment of the 2010s, the current era mirrors the late 1970s, where multiple "false dawns" of falling inflation were followed by sharp rebounds. The market's reaction today suggests a growing realization that the 2% inflation target may be an relic of the past, as a "3% world" becomes the new reality.

Financial institutions are already sounding the alarm. Analysts at J.P. Morgan (NYSE: JPM) have significantly revised their outlook, now predicting zero rate cuts for the entirety of 2026. This is a dramatic shift from early January, when futures markets were pricing in at least three cuts. The fear is no longer just high rates, but "stagflation"—the combination of slowing GDP (which fell to 1.4% in Q4 2025) and rising prices.

The Road Ahead: What to Watch in 2026

As we move toward the March FOMC meeting, the primary focus for investors will be whether the Fed officially shifts its "dot plot" to reflect a "no-cut" year. Short-term, we can expect continued volatility in the bond market as the 10-year Treasury yield tests the 4.25% resistance level. Companies that are heavily dependent on debt refinancing will likely see their credit spreads widen, potentially leading to a strategic pivot toward asset sales or cost-cutting measures to preserve liquidity.

Long-term, the focus will shift to the formal transition of Fed leadership in May. If Kevin Warsh takes the helm, the market will look for signals of how he intends to balance the President's desire for lower rates with the mandate to maintain price stability. Any attempt to politicize the central bank could lead to a crisis of confidence in the U.S. Dollar, further complicating the inflation outlook.

Summary of Market Implications

The latest PCE data has served as a wake-up call for an over-optimistic market. The combination of a 3.0% core inflation reading and the services-led "Supercore" spike has effectively neutralized the case for near-term interest rate cuts. With the added pressure of a 15% global tariff and a slowing GDP, the "soft landing" scenario is looking increasingly fragile.

Moving forward, investors should prioritize "quality" and "defensiveness." Companies with low debt, high cash flow, and the ability to pass on costs to consumers—such as J&J Snack Foods (NASDAQ: JJSF) or NVIDIA (NASDAQ: NVDA)—will likely outperform. In contrast, interest-rate-sensitive sectors and import-dependent retailers are facing a challenging uphill battle.

In the coming months, the key indicators to watch will be the January 2026 PCE data release on March 13 and the subsequent Fed policy statement. If these figures show no signs of cooling, the narrative of 2026 will not be about "when" the cuts are coming, but rather "how high" rates might still need to go to finally tame the inflationary beast.

This content is intended for informational purposes only and is not financial advice.