Shareholders of Parsons would probably like to forget the past six months even happened. The stock dropped 40.8% and now trades at $63.98. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Following the pullback, is now the time to buy PSN? Find out in our full research report, it’s free.

Why Does PSN Stock Spark Debate?

Delivering aerospace technology during the Cold War-era, Parsons (NYSE: PSN) offers engineering, construction, and cybersecurity solutions for the infrastructure and defense sectors.

Two Things to Like:

1. Skyrocketing Revenue Shows Strong Momentum

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Parsons grew its sales at an impressive 11.3% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

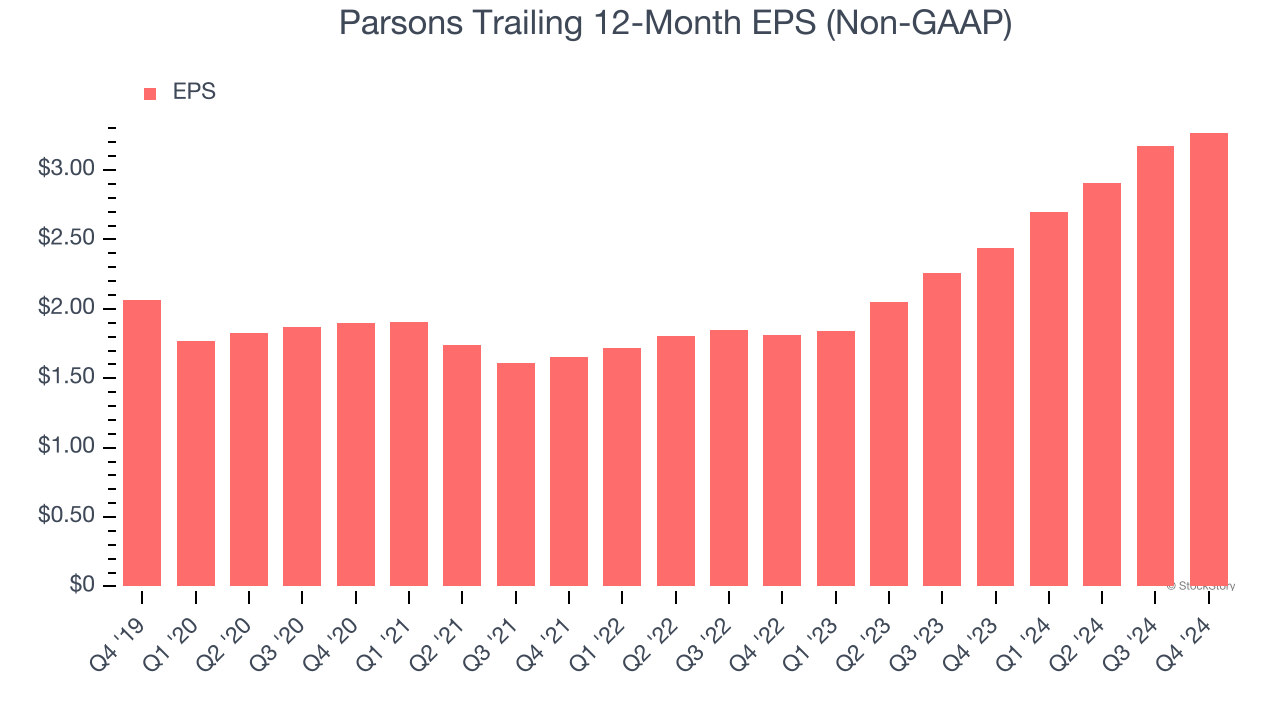

2. EPS Moving Up Steadily

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Parsons’s EPS grew at a decent 9.7% compounded annual growth rate over the last five years. This performance was better than most industrials businesses.

One Reason to be Careful:

Weak Backlog Growth Points to Soft Demand

We can better understand Defense Contractors companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Parsons’s future revenue streams.

Parsons’s backlog came in at $8.89 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 4%. This performance was underwhelming and suggests that increasing competition is causing challenges in winning new orders.

Final Judgment

Parsons’s merits more than compensate for its flaws. After the recent drawdown, the stock trades at 16.1× forward price-to-earnings (or $63.98 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Parsons

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.