| |||||||||

|  |  |  |  | |||||

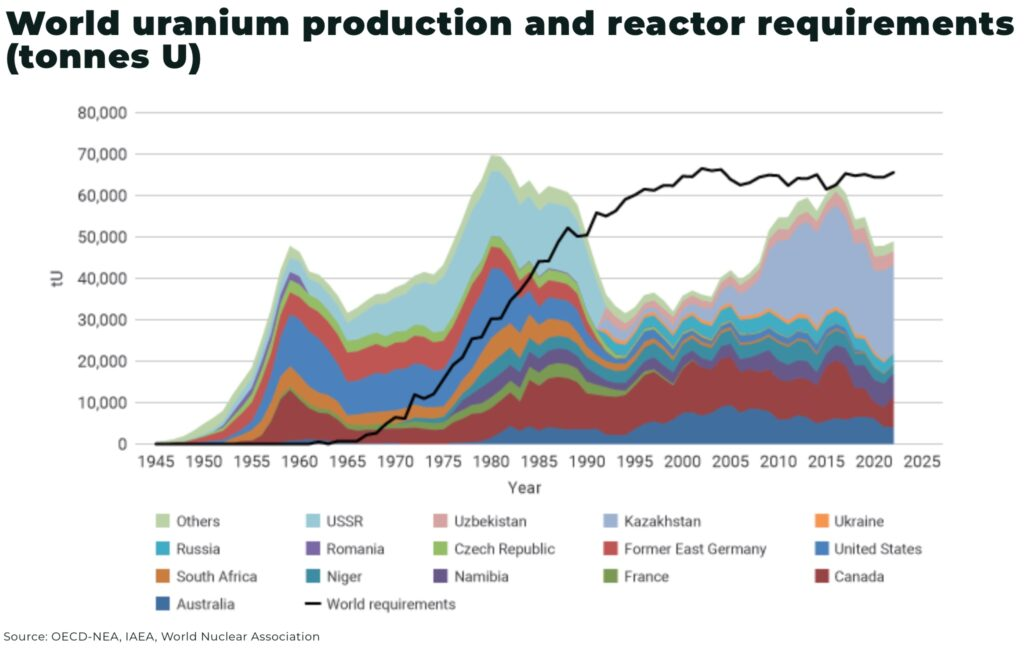

Click Image To View Full Size

Toronto – TheNewswire - September 23, 2025 — The Oregon Group today commented on Cameco’s recent decision to reduce its 2025 uranium production forecast at the McArthur River/Key Lake operation — cutting output to 14–15 million pounds U₃O₈, down from prior guidance of 18 million pounds. The ~22% decrease at the world’s largest high-grade uranium mine underscores tightening global supply and puts fresh attention on other uranium developers and explorers in Canada’s Athabasca Basin. (Read The Oregon Group’s full commentary here: Cameco’s tightening production puts spotlight on the rest of Athabasca Basin).

Until recently, Cameco was still guiding to 18 million pounds at McArthur/Key Lake and Cigar Lake, while raising its expected realized uranium price to ~$87/lb. Development delays, including slower-than-expected ground freezing, forced the revision.

The reduction comes as global supply already trails reactor demand by an estimated 10–20%. Utilities have yet to fully re-enter the market, while demand drivers continue to accelerate:

-

China has 30 reactors under construction and nearly 200 more planned or proposed.

-

The U.S., EU, and Japan are extending reactor lifespans, including restarts at facilities such as the Palisades (U.S.) and Kashiwazaki-Kariwa (Japan).

-

In May, U.S. President Trump signed four executive orders to overhaul the American nuclear sector, expedite reactor approvals, and secure uranium supply chains tied to national security and AI infrastructure.

Click Image To View Full Size

Meanwhile, supply is shrinking. Kazatomprom cut guidance by 5,000 tU citing reagent shortages, Niger’s military junta seized control of Orano’s mine (24% of EU imports), and geopolitical uncertainty clouds Kazakh joint ventures that represent 43% of global output. Cameco itself is expected to buy up to 9–10 million pounds this year to meet deliveries.

Spotlight on the Athabasca Basin

Cameco’s challenges highlight the strategic importance of the Athabasca Basin, home to the world’s highest-grade uranium deposits — in some cases 100x the global average. For the U.S. in particular, Canada remains one of the only reliable partners to secure future uranium supply.

With more than 60 junior companies active in the Basin, investor and utility interest is expected to intensify. Leading developers and explorers include:

-

Denison Mines (TSX:DML | NYSE: DNN): advancing Wheeler River, with provincial EA approval in place and CNSC hearings scheduled for fall 2025.

-

NexGen Energy (TSX:NXE | NYSE: NXE): added a new 5-Mlb offtake to a U.S. utility in August; awaiting a February 2026 Commission Hearing for Rook I.

-

Paladin Energy (ASX:PDN): now controls Patterson Lake South/Triple R following its acquisition of Fission Uranium.

-

F3 Uranium (TSXV:FUU | OTCQB:FUUFF): continues drilling success at Patterson Lake North, with recent high-grade intercepts and a C$7M financing closed.

-

IsoEnergy (NYSE: ISOU | TSX:ISO): expanded its 2025 drill program at Larocque East, reporting assays up to 5.4% U₃O₈; began trading on the NYSE American in May.

-

Geology dictates timing: even with experienced operators, development can slip due to freezing rates, equipment commissioning, and labour constraints.

-

Processing remains a chokepoint: with Cigar Lake ore processed at McClean Lake, mill access is central to Basin development plans.

“Cameco’s revised guidance may appear modest in absolute terms, but it’s significant at the margin — where uranium pricing and contracting are set,” said Anthony Milewski, Chairman of The Oregon Group. “The announcement reinforces what many in the sector already know: the global uranium deficit has no near-term solution, and smaller producers in the Athabasca Basin will be critical to meeting future demand.”

This environment fundamentally alters the risk-reward profile for emerging producers, with three key implications:

-

Price support: higher sustained uranium prices improve project economics.

-

Operational flexibility: smaller operators can adapt more quickly to shifting market dynamics.

-

Strategic premium: new, reliable supply sources will command higher valuations.

The Oregon Group is an independent investment research firm focused on identifying key trends in commodities and energy.

For more information, and to read the full commentary, please visit the Oregon Group’s uranium insights page or email info@oregongroup.com.

Legal Notice

The Oregon Group’s publications are informational and should not be construed as financial or investment advice. Readers are encouraged to conduct their own research and consult with financial professionals before making any investment decisions.

For more information, please visit theoregongroup.com or email info@oregongroup.com

SOURCE The Oregon Group

Disclaimer

The Oregon Group maintains full editorial control over all content published on this website. While sponsored and advertised placements may be featured, the content remains the sole opinion of The Oregon Group. The author may receive compensation or remuneration for providing content, but all statements and expressions are made independently and are not influenced by sponsors or advertisers. From time to time, The Oregon Group and its directors, officers, partners, employees, authors, or members of their families, as well as persons who are interviewed for articles on this website, may have a long or short position in securities or commodities mentioned and may make purchases and/or sales of those securities or commodities in the open market or otherwise. By accessing and using this website, readers are cautioned to assume that each of the foregoing persons may have a financial interest in all companies and sectors mentioned on this website. Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable., and any such statements are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities or commodities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and The Oregon Group undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material. The information provided on this website is for informational purposes only and is not, directly or indirectly, an offer, solicitation of an offer and/or a recommendation to buy or sell any security or commodity, and the information provided on this website should not be construed as any advice or an opinion as to the price at which the securities of any company or commodity may trade at any time. The Oregon Group is a publisher of financial information, not an investment advisor. We do not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient, and the information provided on this website is not and should not be construed as personal, financial, investment or professional advice. Readers are cautioned to always do their own research and review of publicly available information and to consult their professional and registered advisors before purchasing or selling any securities or commodities and should not rely on the information contained herein. Neither The Oregon Group nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein. By using the Site or any affiliated social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Copyright (c) 2025 TheNewswire - All rights reserved.