Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Ryan Specialty (NYSE: RYAN) and the best and worst performers in the insurance brokers industry.

The insurance brokerage industry, while influenced by insurance pricing cycles, benefits from durable secular tailwinds as rising risk complexity (climate, data privacy), regulatory scrutiny, and insurance pricing inflation. These increase demand for professional risk-management advice. Brokers operate models that rely on commissions and fees tied to premium volumes and growing contributions from recurring advisory, benefits, and compliance services. Scale is a key advantage, enabling better carrier access, stronger data and benchmarking, and efficient deployment of technology and compliance investments, which in turn supports ongoing industry consolidation. The headwinds are labor intensity and wage inflation for producers, regulatory complexity (this cuts both ways, as you can see), and execution risk when integrating new digital tools into legacy workflows.

The 5 insurance brokers stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 1.7%.

While some insurance brokers stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 3.8% since the latest earnings results.

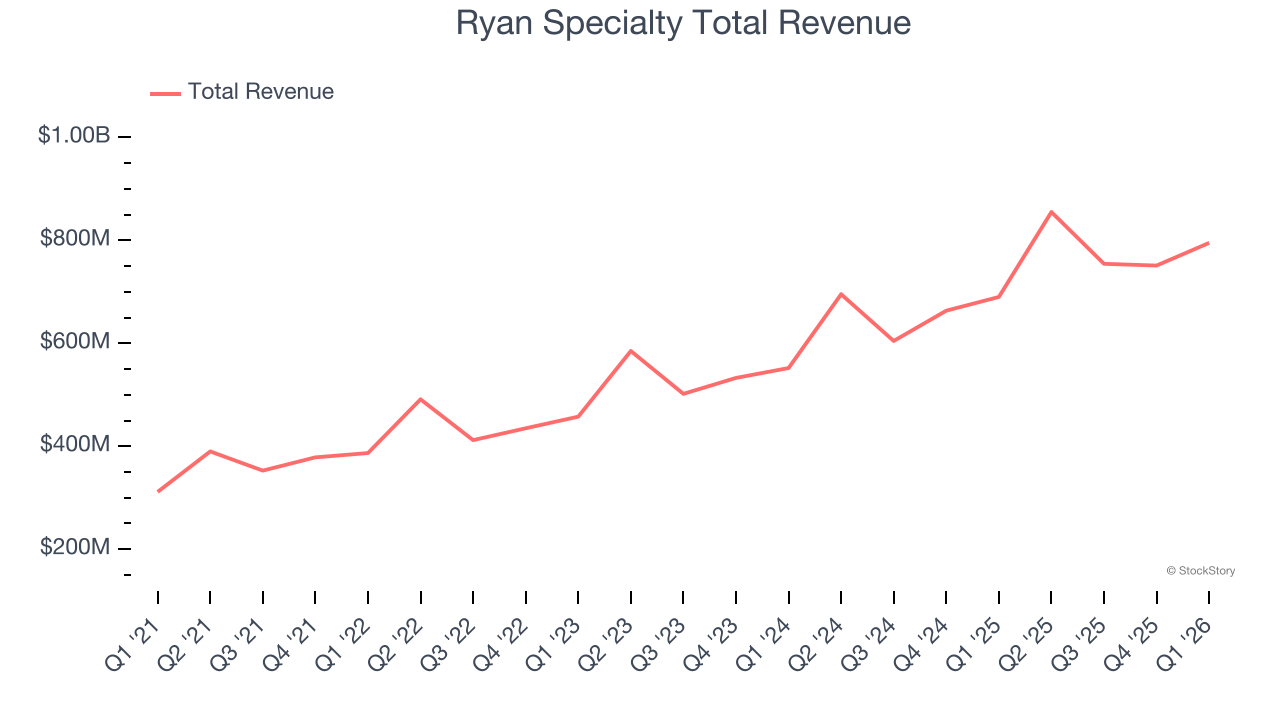

Best Q1: Ryan Specialty (NYSE: RYAN)

Founded in 2010 by insurance industry veteran Patrick Ryan, Ryan Specialty (NYSE: RYAN) is a wholesale insurance broker and underwriting manager that helps retail brokers place complex or hard-to-place risks with insurance carriers.

Ryan Specialty reported revenues of $795.2 million, up 15.2% year on year. This print exceeded analysts’ expectations by 2.1%. Overall, it was a very strong quarter for the company with a beat of analysts’ EPS estimates.

The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $34.97.

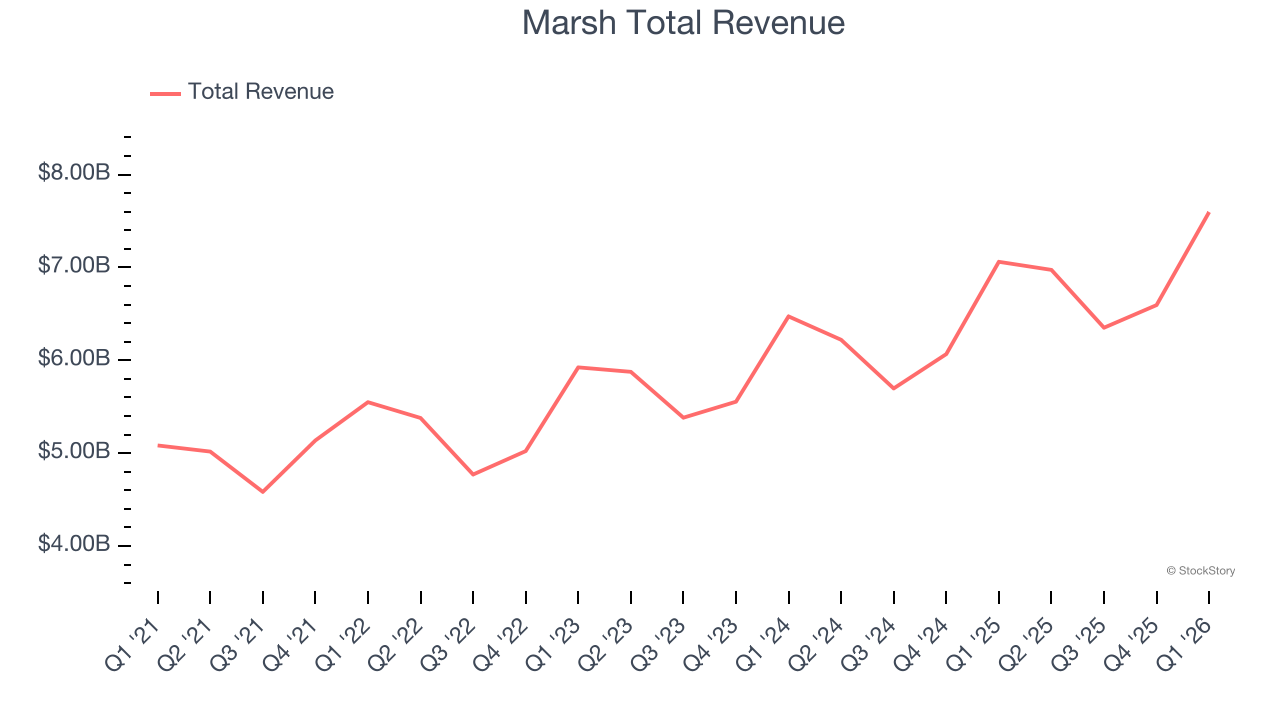

Marsh (NYSE: MRSH)

With roots dating back to 1871 and a presence in over 130 countries, Marsh (NYSE: MRSH) is a global professional services firm that helps organizations manage risk, strategy, and workforce challenges through its four specialized businesses.

Marsh reported revenues of $7.60 billion, up 7.6% year on year, outperforming analysts’ expectations by 2.9%. The business had a strong quarter with a narrow beat of analysts’ organic revenue and EPS estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 7.2% since reporting. It currently trades at $162.35.

Is now the time to buy Marsh? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Brown & Brown (NYSE: BRO)

With roots dating back to 1939 and operations spanning 44 U.S. states and 14 countries, Brown & Brown (NYSE: BRO) is an insurance brokerage and risk management firm that markets and sells insurance products across property, casualty, and employee benefits sectors.

Brown & Brown reported revenues of $1.90 billion, up 35.4% year on year, in line with analysts’ expectations. It was a slower quarter as it posted a significant miss of analysts’ organic revenue estimates.

As expected, the stock is down 12.1% since the results and currently trades at $58.15.

Read our full analysis of Brown & Brown’s results here.

Arthur J. Gallagher (NYSE: AJG)

Founded in 1927 and operating in approximately 130 countries through direct operations and correspondent networks, Arthur J. Gallagher (NYSE: AJG) provides insurance brokerage, reinsurance, consulting, and third-party claims settlement services to businesses and individuals worldwide.

Arthur J. Gallagher reported revenues of $4.75 billion, up 27.7% year on year. This result was in line with analysts’ expectations. Aside from that, it was a mixed quarter as its performance in some other areas of the business was disappointing.

Arthur J. Gallagher had the weakest performance against analyst estimates among its peers. The stock is up 4% since reporting and currently trades at $214.75.

Read our full, actionable report on Arthur J. Gallagher here, it’s free.

Baldwin Insurance Group (NASDAQ: BWIN)

Rebranded from BRP Group in May 2024, Baldwin Insurance Group (NASDAQ: BWIN) is an independent insurance distribution company that provides tailored insurance, risk management, and employee benefits solutions to businesses and individuals.

Baldwin Insurance Group reported revenues of $532.2 million, up 28.7% year on year. This print surpassed analysts’ expectations by 3.2%. Taking a step back, it was a satisfactory quarter as it also recorded EPS in line with analysts’ estimates but a slight miss of analysts’ organic revenue estimates.

Baldwin Insurance Group delivered the biggest analyst estimate beat among its peers. The stock is down 4.3% since reporting and currently trades at $21.02.

Read our full, actionable report on Baldwin Insurance Group here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.