Malibu Boats has been treading water for the past six months, recording a small return of 0.9% while holding steady at $28.66. The stock also fell short of the S&P 500’s 9.1% gain during that period.

Is now the time to buy Malibu Boats, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Malibu Boats Will Underperform?

We're swiping left on Malibu Boats for now. Here are three reasons we avoid MBUU and a stock we'd rather own.

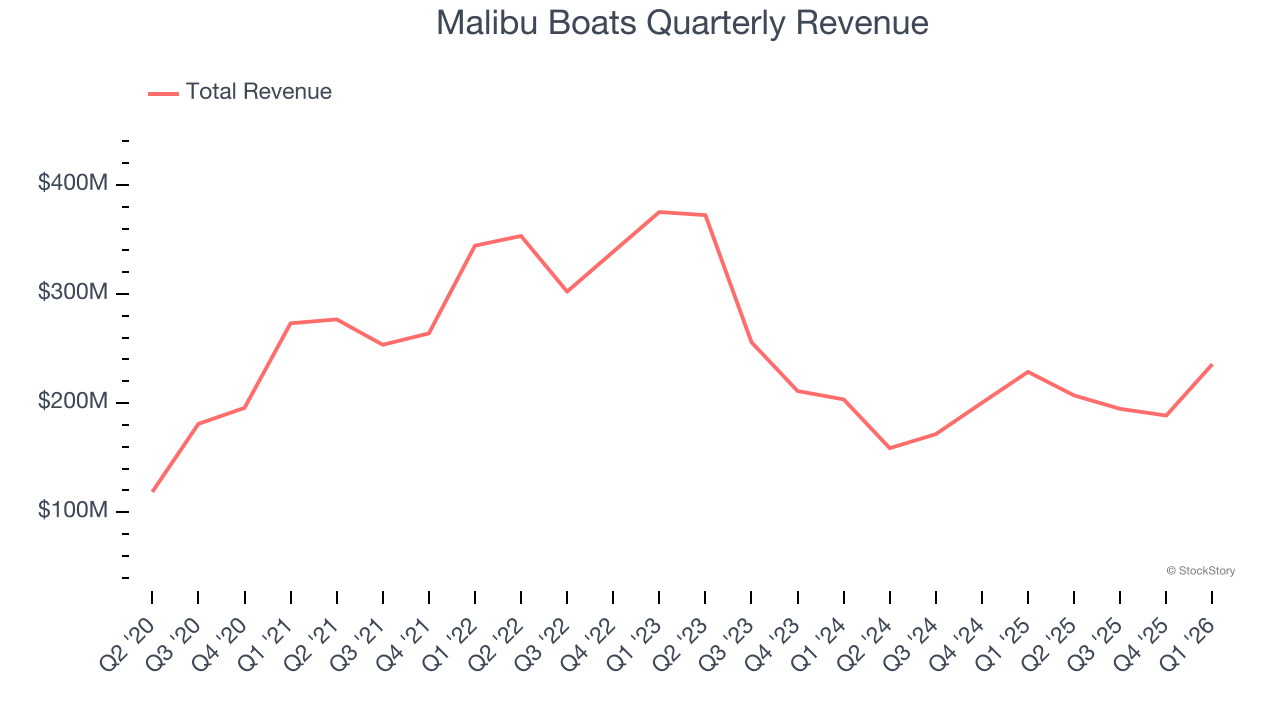

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Malibu Boats grew its sales at a weak 1.5% compounded annual growth rate. This was below our standards.

2. Projected Free Cash Flow Gains to Pump Profits

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict Malibu Boats’s cash conversion will slightly improve. Their consensus estimates imply its free cash flow margin of 4.8% for the last 12 months will increase to 4.4%, giving it more flexibility for investments, share buybacks, and dividends.

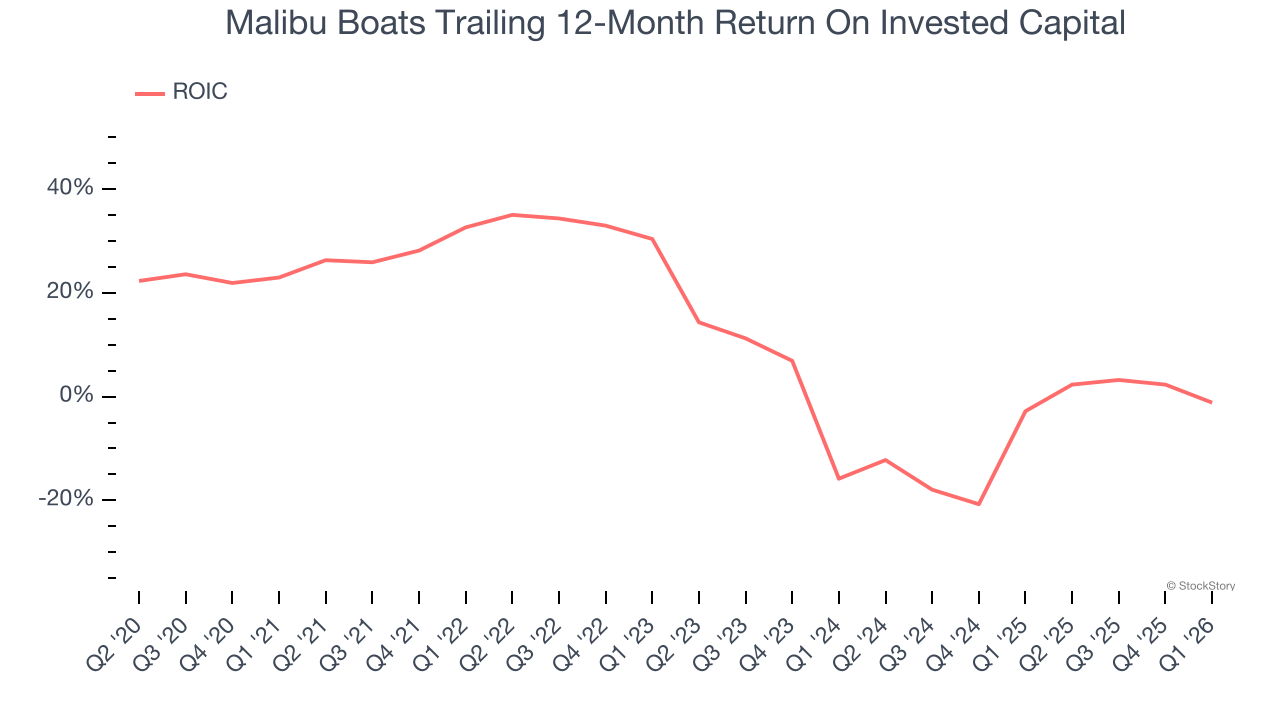

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Malibu Boats’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

Malibu Boats falls short of our quality standards. With its shares lagging the market recently, the stock trades at 13× forward P/E (or $28.66 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better stocks to buy right now. We’d recommend looking at one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month - FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.