S&T Bancorp has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 15.3% to $43.31 per share while the index has gained 13.3%.

Is now the time to buy S&T Bancorp, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is S&T Bancorp Not Exciting?

We're swiping left on S&T Bancorp for now. Here are three reasons you should be careful with STBA and a stock we'd rather own.

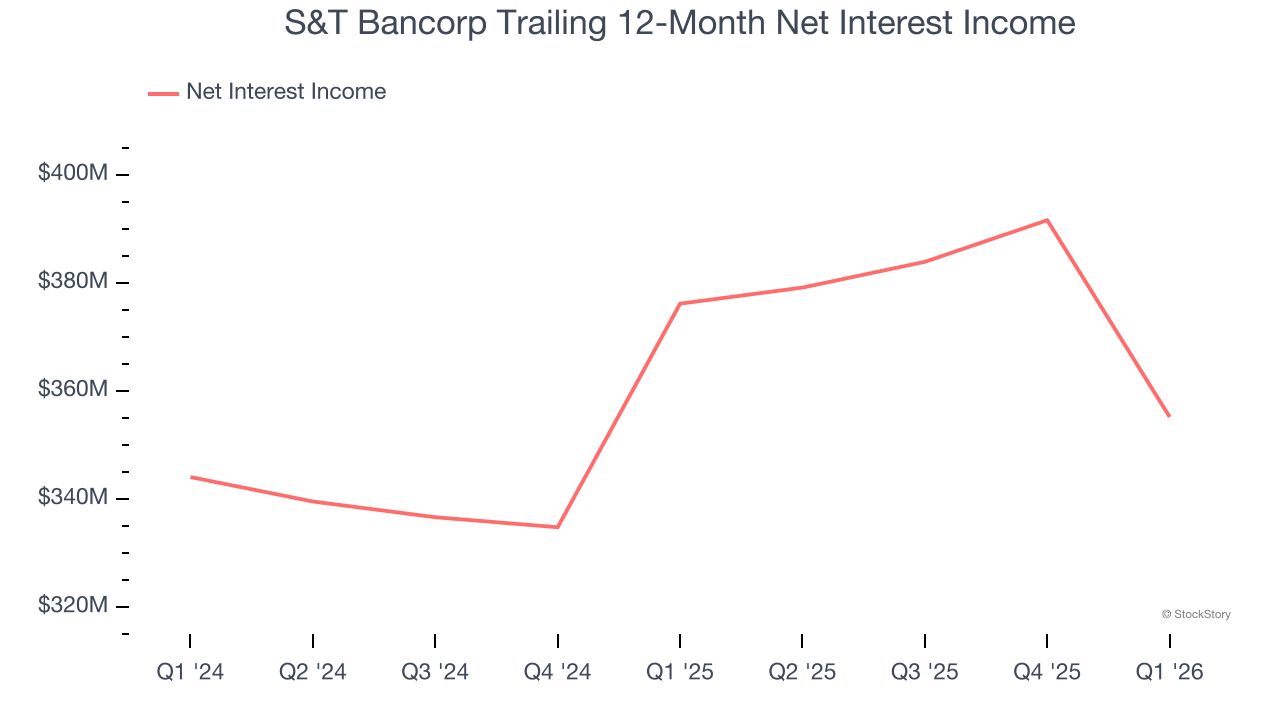

1. Net Interest Income Points to Soft Demand

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

S&T Bancorp’s net interest income has grown at a 4.9% annualized rate over the last five years, much worse than the broader banking industry.

2. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect S&T Bancorp’s net interest income to rise by 3.8%.

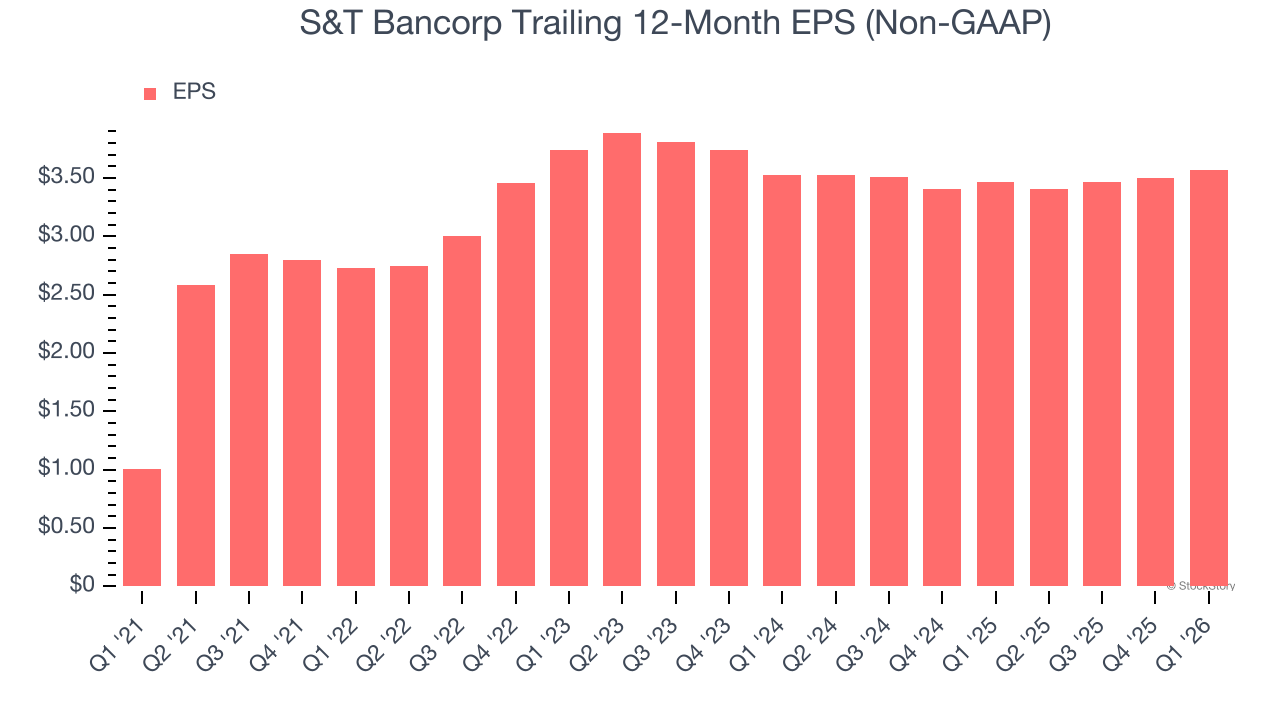

3. EPS Growth Has Stalled Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

S&T Bancorp’s flat EPS over the last two years was worse than its 1.1% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

S&T Bancorp’s business quality ultimately falls short of our standards. That said, the stock currently trades at 1.1× forward P/B (or $43.31 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward one of our top digital advertising picks.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month - FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.