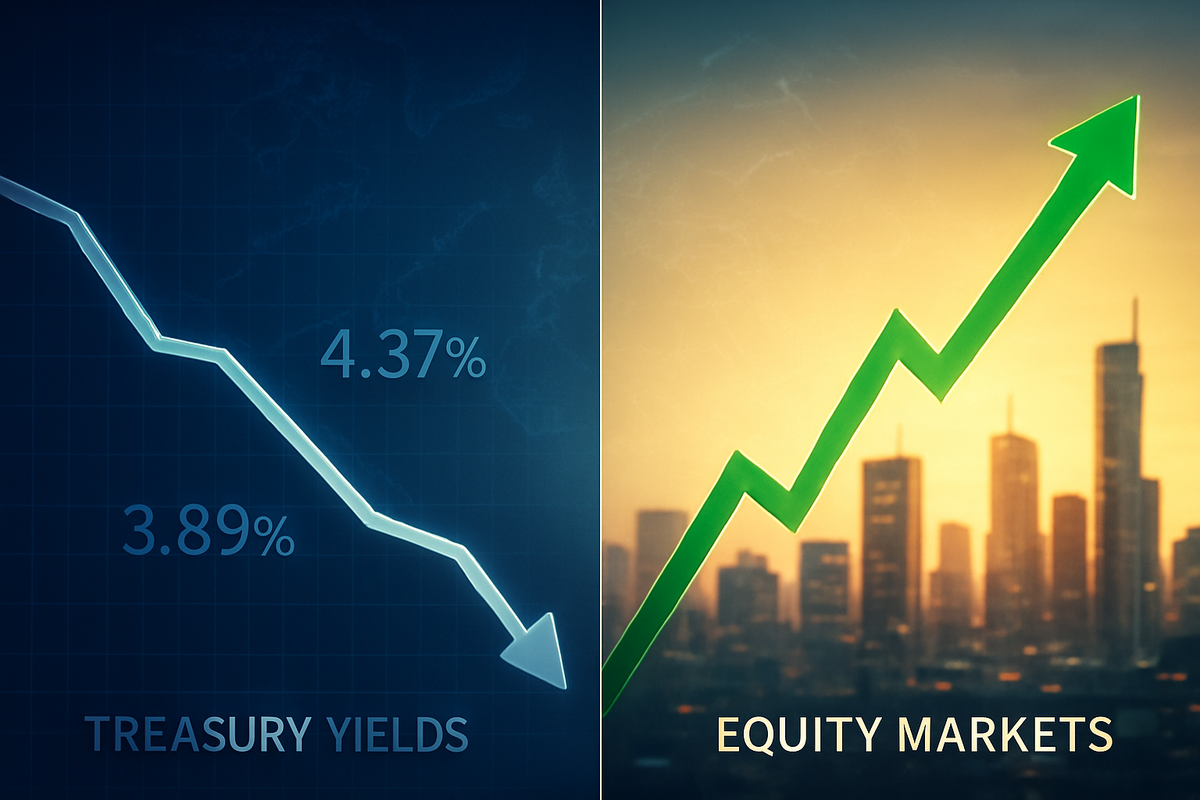

On March 23, 2026, the global financial landscape underwent a dramatic recalibration as a sudden easing of geopolitical tensions in the Middle East and a cooling of trade rhetoric between the United States and China triggered a "risk-on" rally. Treasury yields, which had been pressured upward by inflation fears and a "war premium," fell sharply across the curve. The benchmark 10-year Treasury yield slipped to 4.37%, down from its recent peak of 4.42%, while the 2-year yield dropped to 3.89%. This shift signals a pivot away from the safe-haven "bunker" mentality that dominated the first quarter of 2026, as investors aggressively rotated capital back into equities and high-growth sectors.

The immediate implications are profound: the drop in yields provides much-needed relief to corporate balance sheets and valuation models, particularly for the mega-cap technology firms that have led the AI-driven market cycle. As the threat of a prolonged blockade in the Strait of Hormuz fades and oil prices retreat from their $110-per-barrel highs, the "inflationary spike" narrative that haunted the Federal Reserve's March meeting appears to be dissipating, opening the door for a more accommodative monetary stance in the second half of the year.

The Peace Dividend: How Geopolitics Reshaped the Curve

The market movements on March 23 were a direct response to a rapid de-escalation of hostilities that many analysts had feared would spiral into a global energy crisis. For the past several weeks, the bond market had been pricing in a "worst-case scenario" involving a sustained conflict in the Middle East, which had driven the 10-year yield toward the 4.5% psychological barrier. However, the announcement of a multi-day postponement of military strikes and the initiation of "productive talks" regarding the Strait of Hormuz provided a catalyst for the bond market's reversal.

This timeline of events began with the "Operation Epic Fury" campaign earlier in the month, which initially sent oil prices surging and yields climbing as investors fled to the safety of cash and short-term Treasuries. By the morning of March 23, however, the tone shifted from escalation to diplomacy. Key stakeholders, including officials from the U.S. Treasury and major institutional players like JPMorgan Chase (NYSE: JPM), noted that the "inflation premium" embedded in the bond market was beginning to evaporate. The initial market reaction was swift: the S&P 500 futures jumped 1.2% in pre-market trading, and the yield curve, which had been stubbornly flat, began to show signs of a "bull steepening" as expectations for long-term inflation cooled.

Winners and Losers in the Great Rotation

The primary beneficiaries of this shift are the high-growth technology giants, whose valuations are historically sensitive to fluctuations in the discount rate. Companies like Meta Platforms (NASDAQ: META), Alphabet (NASDAQ: GOOGL), and Amazon (NASDAQ: AMZN) saw immediate buying interest as the 10-year yield fell to 4.37%. For these firms, lower yields translate to higher present values for future earnings, especially as they continue to pour billions into AI infrastructure. Nvidia (NASDAQ: NVDA), the bellwether for the AI supercycle, also saw a rebound as the "macro-drag" of rising rates was lifted, allowing investors to focus once again on the company’s structural growth.

Conversely, the defense and energy sectors are facing a challenging pivot. Major defense contractors like Lockheed Martin (NYSE: LMT) and Northrop Grumman (NYSE: NOC), which had traded at a premium due to heightened global conflict, faced selling pressure as the "war bid" exited the market. Similarly, energy giants such as ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) saw their margins squeezed by the 10% crash in Brent crude prices, which tumbled back toward the $100 level. Financial institutions like BlackRock (NYSE: BLK) may see a mixed impact; while their equity portfolios will benefit from the rally, their fixed-income desks must now navigate a rapidly changing yield environment where "durable income" is no longer the only game in town.

The Wider Significance: A Return to Fundamentals

This shift fits into a broader industry trend where the market is attempting to decouple from geopolitical noise and return to the fundamentals of corporate earnings and the "AI productivity miracle." Historically, periods of intense geopolitical tension often lead to an "overshooting" of bond yields, which then correct sharply once a resolution appears on the horizon. The events of March 23, 2026, mirror the post-Cold War "Peace Dividend" of the 1990s, albeit on a much faster, high-frequency scale.

The regulatory and policy implications are also significant. With inflation expectations cooling alongside oil prices, the Federal Reserve may find it easier to justify a pause or an eventual cut to the federal funds rate, which currently sits at 3.50%–3.75%. Furthermore, the proposed "U.S.-China Board of Trade" suggests a shift toward a more predictable, "managed trade" environment, which could reduce the volatility that has plagued global supply chains since 2024. This de-escalation reduces the "tail risk" for global trade, potentially leading to a more stable environment for multi-national corporations to deploy capital.

What Comes Next: Scenarios and Strategic Pivots

In the short term, market participants should expect continued volatility as the "risk-on" sentiment tests the durability of this peace-driven rally. A key scenario to watch is whether the 10-year yield can hold the 4.30% support level or if it will continue to slide toward 4.15% as the Fed’s next move becomes clearer. For many companies, the strategic pivot will involve shifting away from "defensive" positioning and toward "growth-oriented" capital expenditure. We may see a renewed wave of corporate bond issuances as firms look to lock in these lower yields to fund their 2026 and 2027 expansion plans.

Long-term, the challenge remains the "stickiness" of core inflation. While oil prices have provided immediate relief, the labor market remains relatively tight, and AI-driven demand for energy and high-tech components could create new inflationary pressures. Investors must remain vigilant; if the peace talks in the Middle East or the trade negotiations with China hit a stalemate, the "flight to safety" could return just as quickly as it left, sending yields back toward the 4.5% mark.

Summary and Market Outlook

The retreat in Treasury yields on March 23, 2026, marks a pivotal moment for the markets this year. By falling to 4.37% (10-year) and 3.89% (2-year), yields have signaled a collective sigh of relief from an investment community that was previously braced for a "forever war" scenario. The transition from safe havens like Treasury bonds into the equity markets reflects a renewed confidence in the underlying strength of the US economy and its dominant technology players.

Moving forward, the market will likely be characterized by a "wait-and-see" approach as the diplomatic breakthroughs are formalized. The key takeaways for investors are clear: the "risk-off" trade has lost its momentum, and the "AI growth" story has regained its footing. In the coming months, the most important metrics to watch will be the stability of oil prices, the official communique from the U.S.-China trade summit, and the Fed’s rhetoric regarding the "neutral rate" in a post-conflict environment. For now, the "Peace Dividend" of 2026 has provided the spark for what could be a significant spring rally.

This content is intended for informational purposes only and is not financial advice.