With a market cap of $36.8 billion, Live Nation Entertainment, Inc. (LYV) is a global powerhouse in live entertainment, seamlessly blending concert promotion, ticketing, and artist management into one dynamic enterprise. Headquartered in Beverly Hills, California, Live Nation operates through key segments, Concerts, Ticketmaster, and Sponsorship & Advertising, positioning itself as the go-to platform for live experiences worldwide. It is all geared up to release its Q1 earnings results soon.

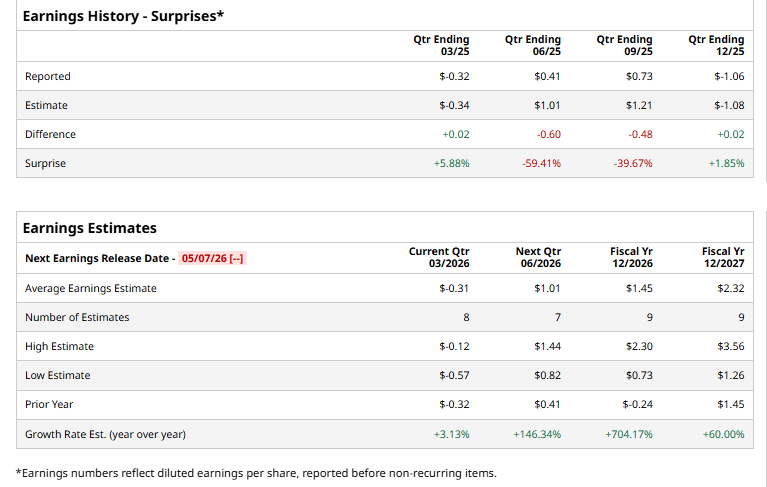

Ahead of this event, analysts expect the leading ticket seller to report a loss of $0.31 per share, down 3.1% from the loss of $0.32 per share in the year-ago quarter. The company has surpassed Wall Street's bottom-line estimates in two of the last four quarters while missing on two other occasions.

For fiscal 2026, analysts expect LYV to report EPS of $1.45, up 704.2% from a loss of $0.24 in fiscal 2025. Moreover, its EPS is expected to grow 60% in FY2027, reaching $2.32.

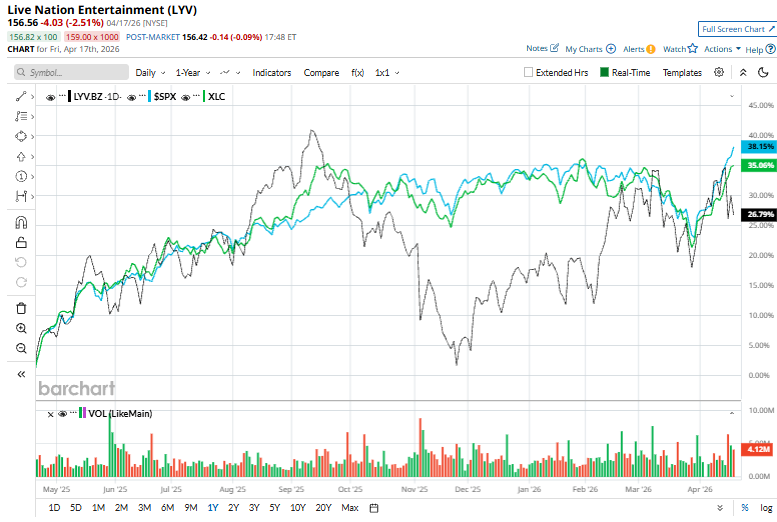

Live Nation Entertainment has surged 23.1% over the past 52 weeks, underperforming both the S&P 500 Index's ($SPX) 34.9% gain and the State Street Communication Services Select Sector SPDR ETF Fund's (XLC) 32% increase over the same period.

Live Nation Entertainment has lagged the broader market, primarily due to recent regulatory overhang and legal uncertainty tied to antitrust scrutiny of its Ticketmaster business and ongoing litigation. Investor sentiment has also been pressured by concerns about potential fines, structural remedies, or operational restrictions that could impact its high-margin ticketing segment.

While live event demand remains strong, the stock has faced multiple compressions after a strong prior run, alongside broader rotation away from reopening-driven plays into tech-led market leadership. Additionally, rising costs, execution risks around large-scale events, and headline sensitivity to political and consumer backlash over ticket pricing have weighed on performance.

Overall, analysts' consensus view on Live Nation Entertainment stock is very bullish, with a "Strong Buy" rating. Out of 24 analysts covering the stock, 20 recommend a "Strong Buy," one suggests a "Moderate Buy," two give a "Hold," and one gives a “Strong Sell” rating.

LYV’s mean analyst price target of $186.86 indicates an upswing potential of 19.4% from the prevailing price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Netflix Generates Massive FCF and FCF Margins - NFLX Price Targets Are Higher

- Alibaba Just Launched New AI Models for Video Games. Does That Make BABA Stock a Buy?

- Dear Seagate Technology Stock Fans, Mark Your Calendars for April 28

- Profit Jumped 58% at Taiwan Semi. Does That Make TSM Stock a Buy Here?