Amidst significant volatility, CrowdStrike (CRWD) stock has trended higher by 9% in the last 52 weeks. But this provides investors with an incomplete picture from the perspective of stock price action. Back in November 2025, CRWD stock touched a high of $566.90. From that level, the stock has seen a steep correction of 31%, largely on the back of an overreaction to the impact of AI on the cybersecurity industry.

As market participants analyze these developments, however, it’s relatively clear that CrowdStrike will continue to grow and create value. According to Wedbush, the growth in AI has translated into a major catalyst for the cybersecurity industry. CrowdStrike already has AI security as an integral part of its Falcon platform.

Wedbush estimates that cybersecurity will likely be 10% of IT budgets in the coming years from 5% currently. This will benefit industry leaders like CrowdStrike, Palo Alto Networks (PANW), and Zscaler (ZS), among others.

Wolfe Research also recently upgraded CrowdStrike to an “Outperform” rating with a price target of $450 on the back of AI benefits. As markets look beyond the initial knee-jerk reaction for CRWD stock, there seems to be potential for growth and stock upside.

About CrowdStrike Stock

Founded in 2011 and headquartered in Austin, Texas, Crowdstrike provides cybersecurity solutions both in the United States and internationally. The company claims to have one of the most advanced cloud-native platforms for the protection of endpoints and cloud workloads, identity and data. Currently, CrowdStrike offers 33 cloud modules on its Falcon Platform through the SaaS model.

CrowdStrike ended the fourth quarter with a record annual recurring revenue (ARR) of $5.25 billion, which was higher by 24% on a year-over-year (YOY) basis. Importantly, during the year, the company achieved $1 billion in net new ARR.

With an ever-expanding market for cybersecurity products, CrowdStrike is positioned for sustained growth. For calendar year 2026, the company expects the total addressable market to be $149 billion. Further, the TAM is expected to expand to $325 billion by the end of the decade.

Despite this swelling opportunity, CRWD stock has declined by 21% in the last six months. With impending benefits from AI growth, CRWD stock seems attractive.

Strong Guidance for Fiscal 2027

For fiscal 2027, CrowdStrike provided healthy ARR guidance of $6.5 billion. Further, the company expects total revenue of $5.9 billion. A free cash flow margin in the range of 34% to 38% will ensure strong financial flexibility for organic and acquisition-driven growth. It’s worth noting that the company already announced two acquisitions in early 2026 (Seraphic and SGNL). With healthy cash flows, further acquisitions are likely.

At the same time, CrowdStrike has guided for research and development expenses in the range of 15% to 20% of the revenue. Continued platform innovation will ensure that ARR swells further in the coming years.

Another important point to note is that, for Q4 2026, the company reported 66% revenue from the United States. On the other hand, Asia Pacific revenue accounted for just 11% of total revenue. Accordingly, there is ample scope for growth in emerging markets like Asia, Latin America, and Africa.

What Do Analysts Say About CRWD Stock?

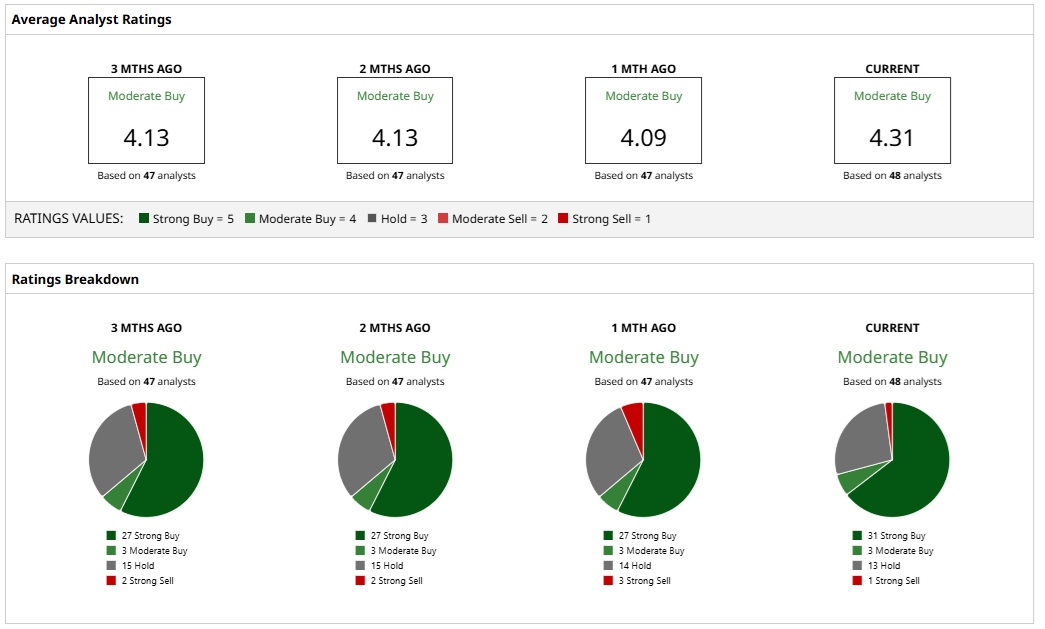

Based on 48 analysts with coverage, CRWD stock has a consensus “Moderate Buy” rating. While 32 analysts have a “Strong Buy” rating, three analysts have a “Moderate Buy,” 12 analysts have a “Hold” rating, and one analyst believes that the stock is a “Strong Sell.”

The mean price target of $491.48 represents potential upside of about 25% from current levels. Further, the most bullish price target of $706 suggests that CRWD stock could climb 70% from here.

All told, Crowdstrike stock remaining sideways in the last 52 weeks seems like a good buying opportunity. With analysts expecting earnings growth of 2,625% for fiscal 2027 and 67% for fiscal 2028, the stock is likely to breakout in the upside.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Boeing Jumps on New Pentagon Deal. Should You Buy BA Stock Here?

- This Tech Stock May Be About to Short Circuit Near 52-Week Highs

- A Giant Meatpacking Strike Isn’t Enough to Dent the Bull Case for JBS Stock, According to Bank of America

- TotalEnergies Is ‘Dominating’ Amidst Iran War Oil Disruptions. Should You Buy TTE Stock Now?