Let’s dig into the relative performance of Expedia (NASDAQ: EXPE) and its peers as we unravel the now-completed Q1 consumer internet earnings season.

The ways people shop, transport, communicate, learn and play are undergoing a tremendous, technology-enabled change. Consumer internet companies are playing a key role in lives being transformed, simplified and made more accessible.

The 46 consumer internet stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 1.2% while next quarter’s revenue guidance was 0.6% below.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

Expedia (NASDAQ: EXPE)

Originally founded as a part of Microsoft, Expedia (NASDAQ: EXPE) is one of the world’s leading online travel agencies.

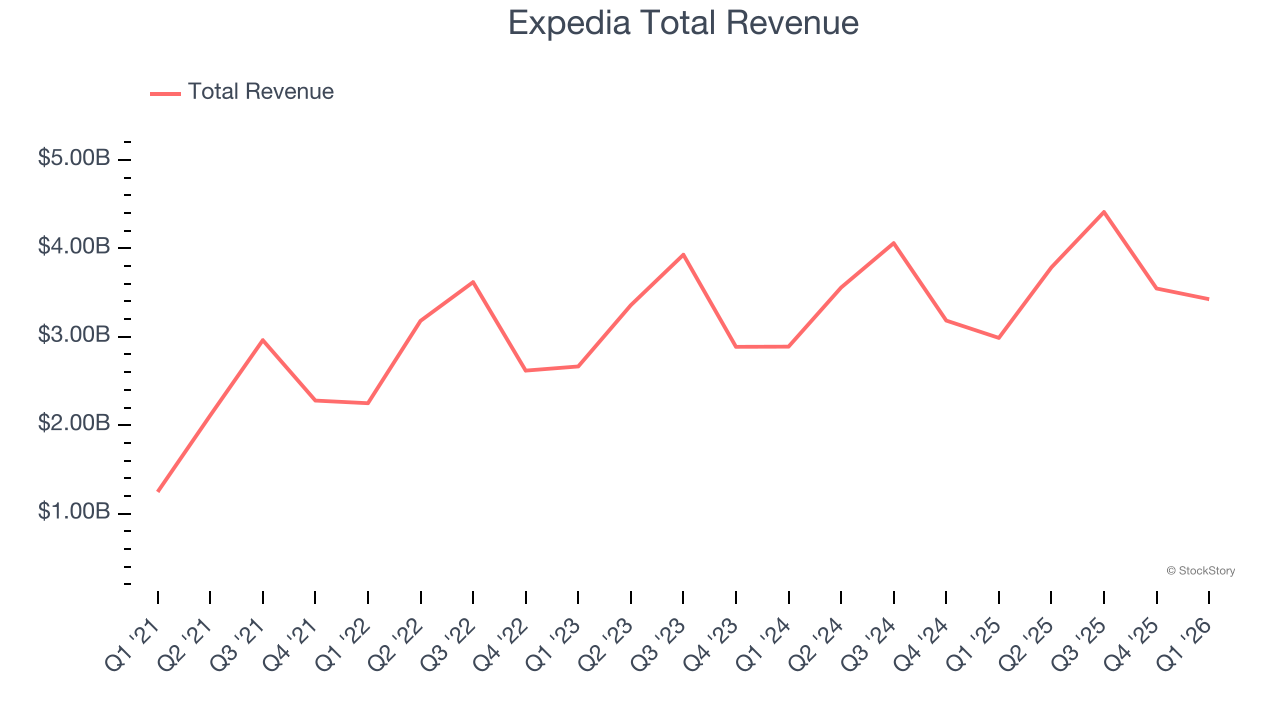

Expedia reported revenues of $3.43 billion, up 14.7% year on year. This print exceeded analysts’ expectations by 2.2%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ EBITDA estimates and revenue guidance for next quarter slightly topping analysts’ expectations.

Interestingly, the stock is up 3.6% since reporting and currently trades at $262.

Is now the time to buy Expedia? Access our full analysis of the earnings results here, it’s free.

Best Q1: Sea (NYSE: SE)

Founded in 2009 and a publicly traded company since 2017, Sea (NYSE: SE) started as a gaming platform and has since expanded to offer a variety of services such as e-commerce, digital payments, and financial services across Southeast Asia.

Sea reported revenues of $7.33 billion, up 43.2% year on year, outperforming analysts’ expectations by 10.1%. The business had a stunning quarter with an impressive beat of analysts’ EBITDA estimates and solid growth in its users.

Sea pulled off the biggest analyst estimate beat among its peers. The company reported 72.6 million users, up 12.4% year on year. The market seems happy with the results as the stock is up 7.7% since reporting. It currently trades at $91.40.

Is now the time to buy Sea? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Shutterstock (NYSE: SSTK)

Originally featuring a library that included many of founder Jon Oringer’s photos, Shutterstock (NYSE: SSTK) is now a digital platform where customers can license and use hundreds of millions of pieces of content.

Shutterstock reported revenues of $199.2 million, down 17.9% year on year, falling short of analysts’ expectations by 10.1%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA estimates.

Shutterstock delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 18.3% since the results and currently trades at $14.40.

Read our full analysis of Shutterstock’s results here.

ACV Auctions (NYSE: ACVA)

Founded in 2014, ACV Auctions (NYSE: ACVA) is an online auction marketplace for car dealers and wholesalers to buy and sell used cars.

ACV Auctions reported revenues of $204.2 million, up 11.8% year on year. This result beat analysts’ expectations by 1.1%. Taking a step back, it was a mixed quarter as it also produced an impressive beat of analysts’ EBITDA estimates but EBITDA guidance for next quarter missing analysts’ expectations significantly.

The stock is up 35.9% since reporting and currently trades at $7.09.

Read our full, actionable report on ACV Auctions here, it’s free.

Coupang (NYSE: CPNG)

Founded in 2010 by Harvard Business School student Bom Kim, Coupang (NYSE: CPNG) is an e-commerce giant often referred to as the "Amazon of South Korea".

Coupang reported revenues of $8.50 billion, up 7.5% year on year. This number lagged analysts’ expectations by 0.6%. More broadly, it was actually a satisfactory quarter as it recorded a solid beat of analysts’ EBITDA estimates.

The company reported 23.9 million active buyers, up 2.1% year on year. The stock is down 14.9% since reporting and currently trades at $17.68.

Read our full, actionable report on Coupang here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.