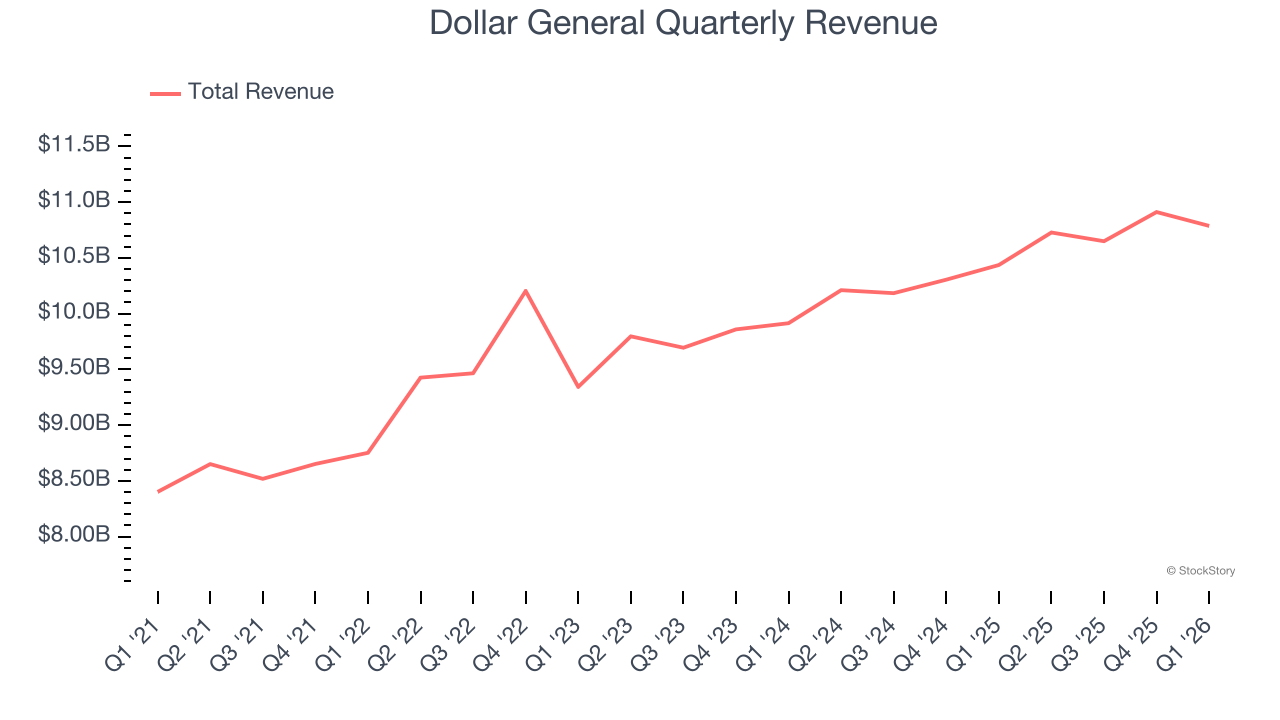

Discount retailer Dollar General (NYSE: DG) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 3.4% year on year to $10.79 billion. Its GAAP profit of $2 per share was 6.2% above analysts’ consensus estimates.

Is now the time to buy Dollar General? Find out by accessing our full research report, it’s free.

Dollar General (DG) Q1 CY2026 Highlights:

- Revenue: $10.79 billion vs analyst estimates of $10.82 billion (3.4% year-on-year growth, in line)

- EPS (GAAP): $2 vs analyst estimates of $1.88 (6.2% beat)

- EPS (GAAP) guidance for the full year is $7.33 at the midpoint, beating analyst estimates by 1%

- Operating Margin: 5.9%, in line with the same quarter last year

- Free Cash Flow Margin: 3.4%, down from 5.3% in the same quarter last year

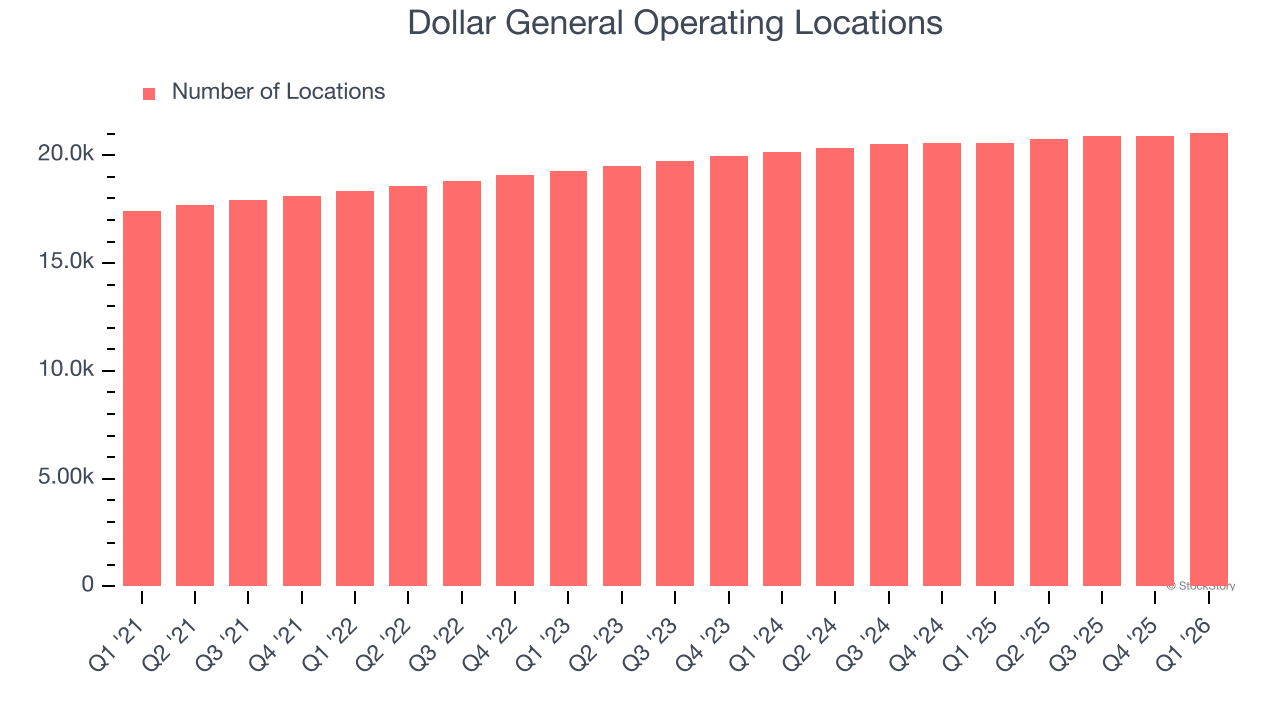

- Locations: 21,055 at quarter end, up from 20,582 in the same quarter last year

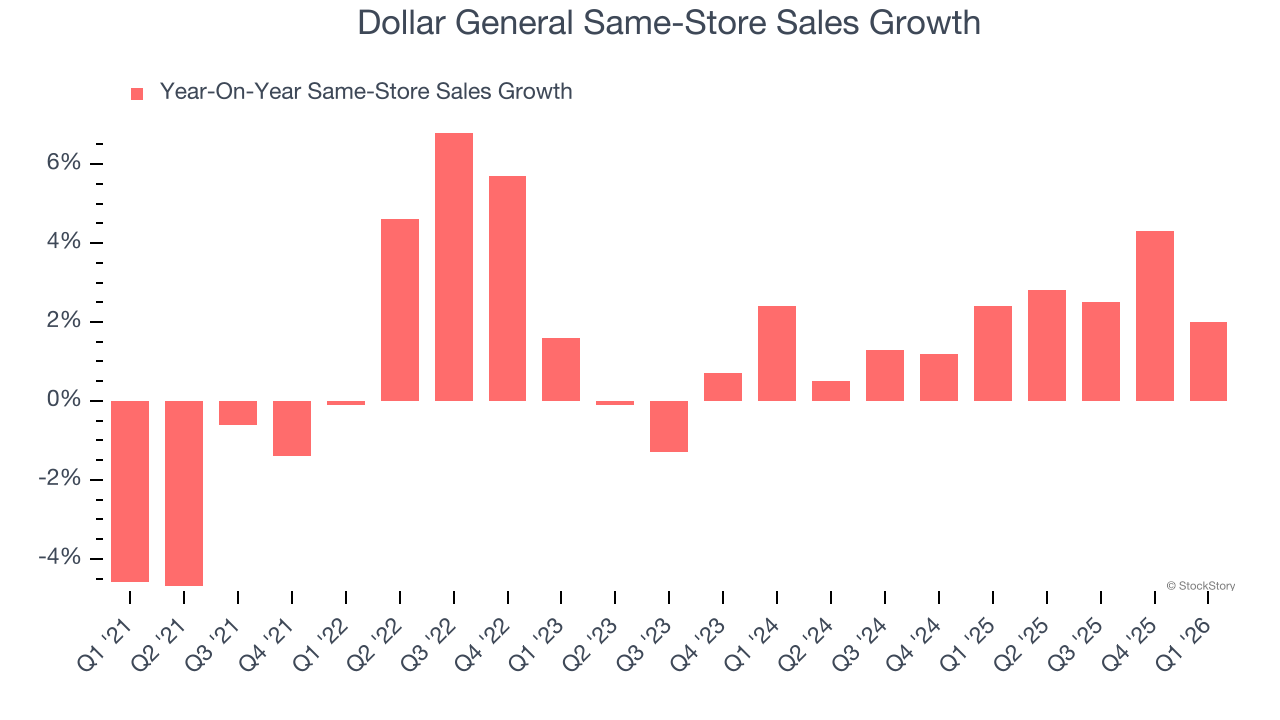

- Same-Store Sales rose 2% year on year, in line with the same quarter last year

- Market Capitalization: $24.21 billion

Company Overview

Appealing to the budget-conscious consumer, Dollar General (NYSE: DG) is a discount retailer that sells a wide range of household essentials, groceries, apparel/beauty products, and seasonal merchandise.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $43.08 billion in revenue over the past 12 months, Dollar General is larger than most consumer retail companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. This also gives it the flexibility to offer lower prices. However, its scale is a double-edged sword because there is only so much real estate to build new stores, placing a ceiling on its growth. To accelerate sales, Dollar General likely needs to optimize its pricing or lean into international expansion.

As you can see below, Dollar General’s sales grew at a sluggish 3.9% compounded annual growth rate over the last three years, but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, Dollar General grew its revenue by 3.4% year on year, and its $10.79 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.1% over the next 12 months, similar to its three-year rate. This projection is above average for the sector and indicates its newer products will help sustain its historical top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Dollar General sported 21,055 locations in the latest quarter. Over the last two years, it has opened new stores quickly, averaging 2.6% annual growth. This was faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

The change in a company’s store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer’s e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Dollar General’s demand rose over the last two years and slightly outpaced the industry. On average, the company’s same-store sales have grown by 2.1% per year. This performance suggests its rollout of new stores could be beneficial for shareholders. When a retailer has demand, more locations should help it reach more customers and boost revenue growth.

In the latest quarter, Dollar General’s same-store sales rose 2% year on year. This performance was more or less in line with its historical levels.

Key Takeaways from Dollar General’s Q1 Results

We enjoyed seeing Dollar General beat analysts’ EPS expectations this quarter. We were also glad its full-year EPS guidance slightly exceeded Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 3.6% to $114.25 immediately after reporting.

Dollar General had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).