Over the past six months, Alarm.com’s shares (currently trading at $43.44) have posted a disappointing 16.1% loss, well below the S&P 500’s 5% gain. This might have investors contemplating their next move.

Is now the time to buy Alarm.com, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Alarm.com Will Underperform?

Even though the stock has become cheaper, we don't have much confidence in Alarm.com. Here are three reasons there are better opportunities than ALRM and a stock we'd rather own.

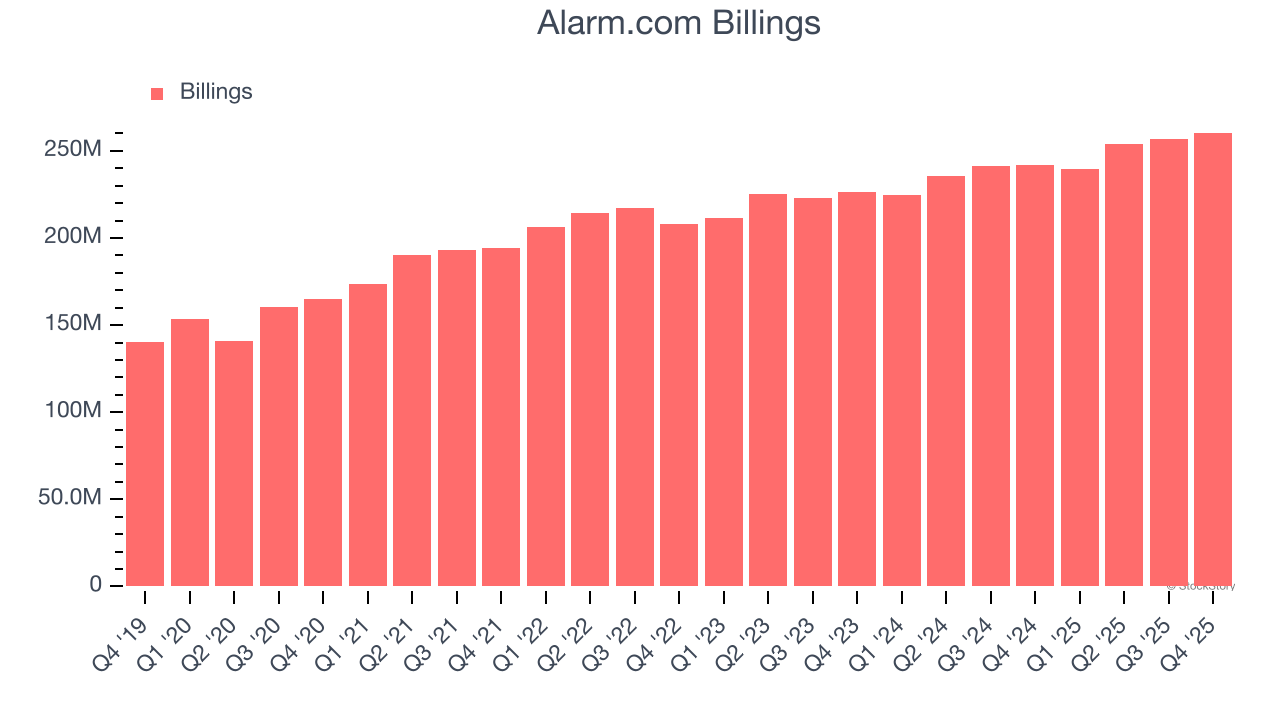

1. Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Alarm.com’s billings came in at $260.5 million in Q4, and over the last four quarters, its year-on-year growth averaged 7.2%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Alarm.com’s revenue to rise by 5%, a slight deceleration versus its 10.3% annualized growth for the past five years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

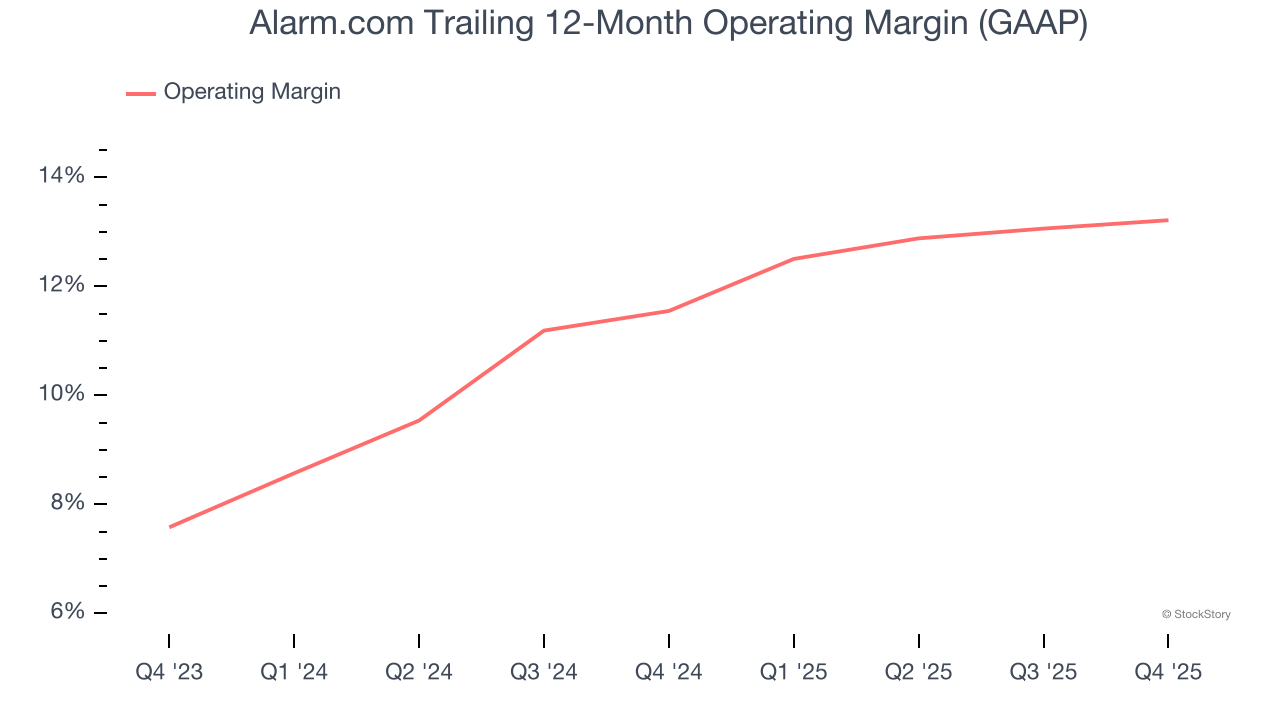

3. Operating Margin Rising, Profits Up

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Analyzing the trend in its profitability, Alarm.com’s operating margin rose by 1.7 percentage points over the last two years, as its sales growth gave it operating leverage. Its operating margin for the trailing 12 months was 13.2%.

Final Judgment

We see the value of companies addressing major business pain points, but in the case of Alarm.com, we’re out. After the recent drawdown, the stock trades at 2.5× forward price-to-sales (or $43.44 per share). This valuation multiple is fair, but we don’t have much confidence in the company. There are more exciting stocks to buy at the moment. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.