Regional banking company WSFS Financial (NASDAQ: WSFS) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 7.3% year on year to $275.3 million. Its non-GAAP profit of $1.68 per share was 11.9% above analysts’ consensus estimates.

Is now the time to buy WSFS Financial? Find out by accessing our full research report, it’s free.

WSFS Financial (WSFS) Q1 CY2026 Highlights:

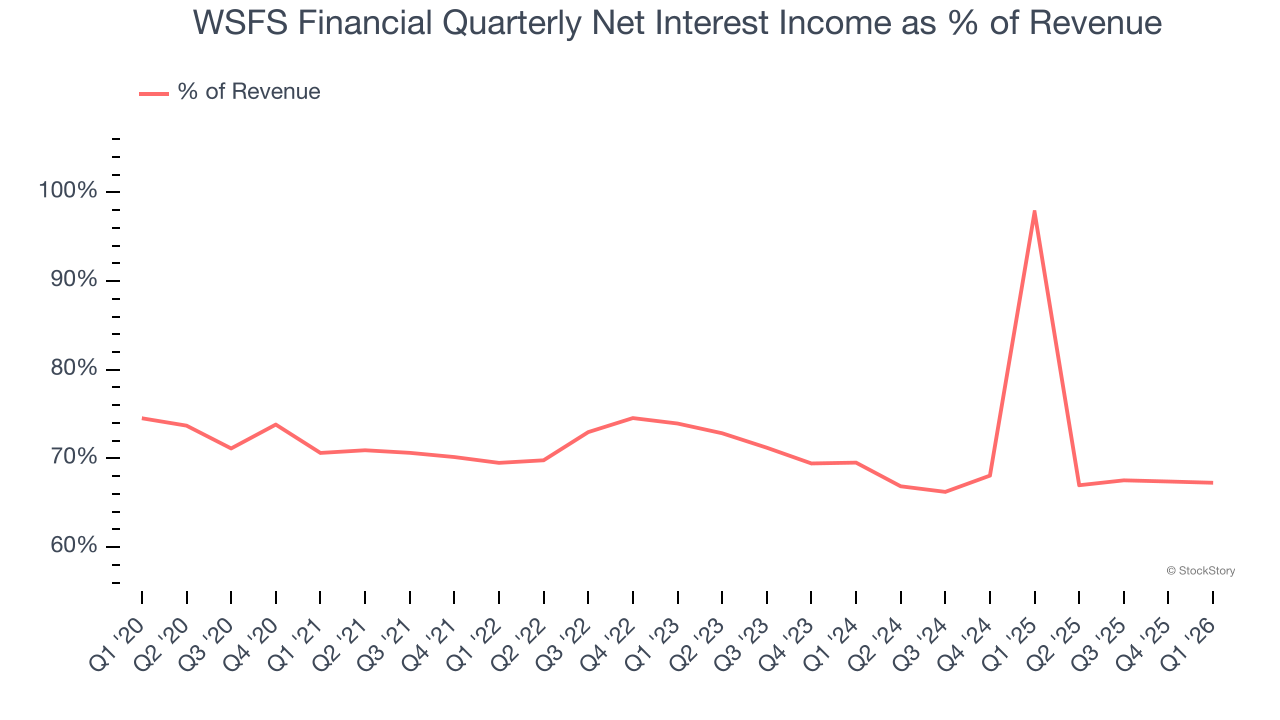

- Net Interest Income: $185.1 million vs analyst estimates of $181.7 million (26.2% year-on-year decline, 1.9% beat)

- Net Interest Margin: 3.8% vs analyst estimates of 3.8% (2.8 basis point beat)

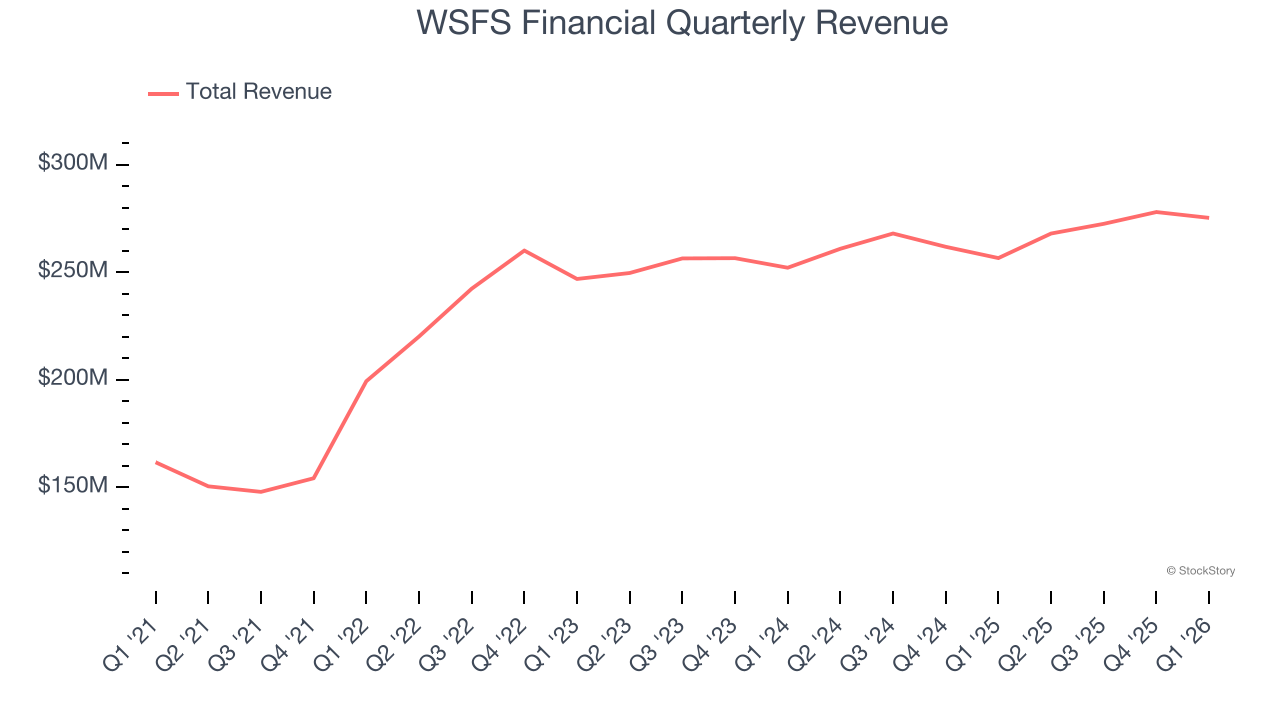

- Revenue: $275.3 million vs analyst estimates of $268.9 million (7.3% year-on-year growth, 2.4% beat)

- Efficiency Ratio: 58% vs analyst estimates of 59.4% (143.3 basis point beat)

- Adjusted EPS: $1.68 vs analyst estimates of $1.50 (11.9% beat)

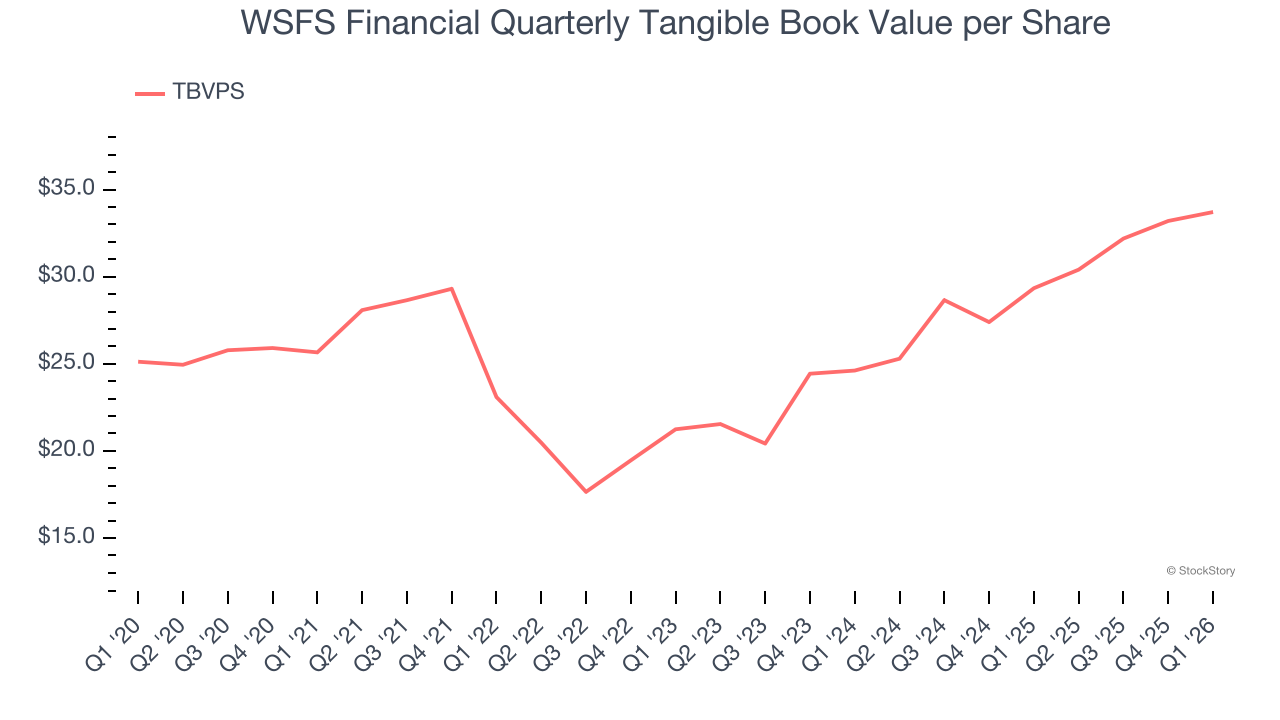

- Tangible Book Value per Share: $33.71 vs analyst estimates of $33.96 (14.9% year-on-year growth, 0.7% miss)

- Market Capitalization: $3.62 billion

Company Overview

Founded in 1832 as Wilmington Savings Fund Society and one of the oldest banks in America still operating under its original name, WSFS Financial (NASDAQ: WSFS) operates a community banking and wealth management franchise primarily serving customers in the Mid-Atlantic region through its main subsidiary, WSFS Bank.

Sales Growth

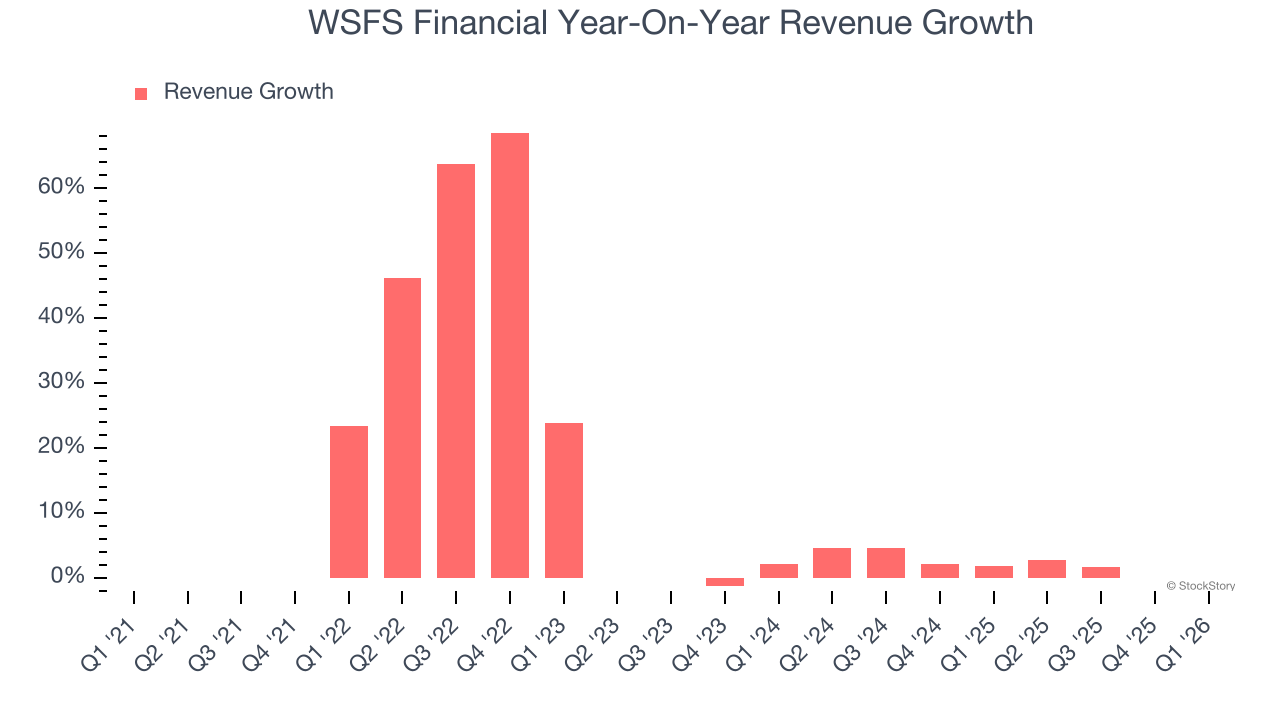

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities. Luckily, WSFS Financial’s revenue grew at a decent 11.3% compounded annual growth rate over the last five years. Its growth was slightly above the average banking company and shows its offerings resonate with customers.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. WSFS Financial’s recent performance shows its demand has slowed as its annualized revenue growth of 3.8% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, WSFS Financial reported year-on-year revenue growth of 7.3%, and its $275.3 million of revenue exceeded Wall Street’s estimates by 2.4%.

Net interest income made up 71.2% of the company’s total revenue during the last five years, meaning lending operations are WSFS Financial’s largest source of revenue.

While banks generate revenue from multiple sources, investors view net interest income as the cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of non-interest income.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Tangible Book Value Per Share (TBVPS)

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to M&A or accounting rules allowing for loan losses to be spread out.

WSFS Financial’s TBVPS grew at a decent 5.6% annual clip over the last five years. TBVPS growth has accelerated recently, growing by 17% annually over the last two years from $24.61 to $33.71 per share.

Over the next 12 months, Consensus estimates call for WSFS Financial’s TBVPS to grow by 14.7% to $38.67, decent growth rate.

Key Takeaways from WSFS Financial’s Q1 Results

It was encouraging to see WSFS Financial beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its tangible book value per share slightly missed. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $70.23 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).