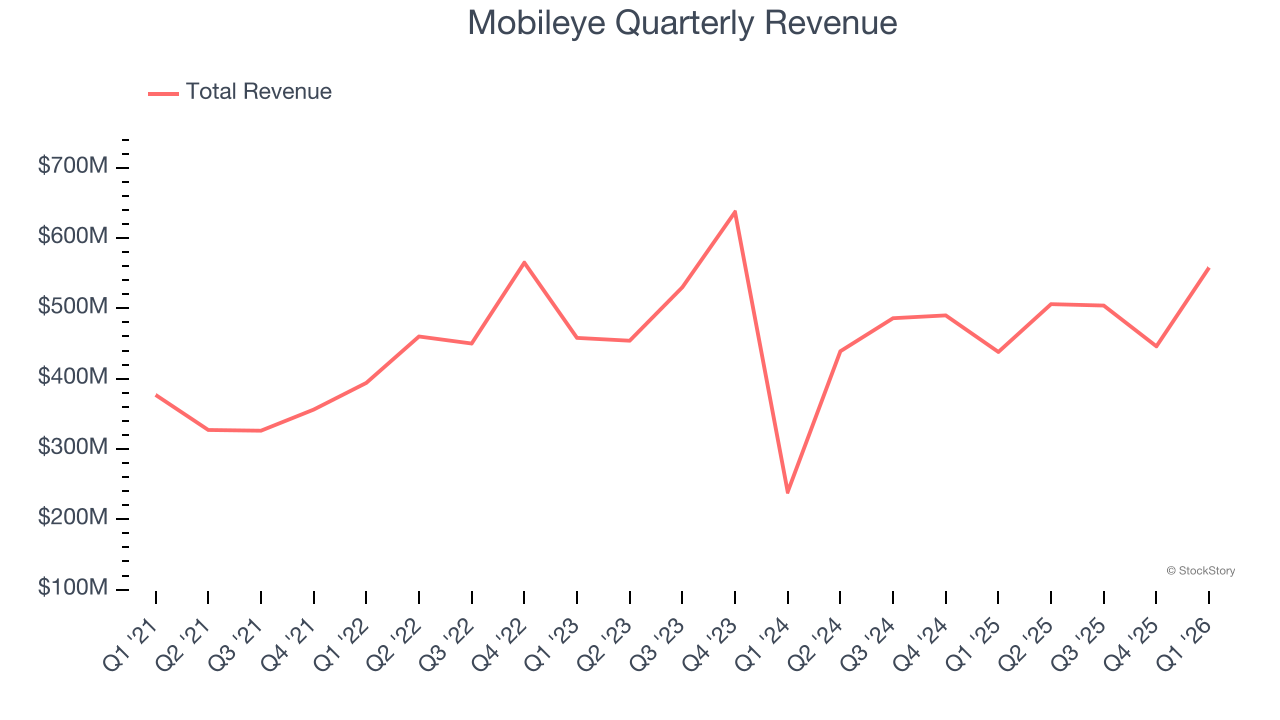

Autonomous driving technology company Mobileye (NASDAQ: MBLY) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 27.4% year on year to $558 million. The company’s full-year revenue guidance of $1.98 billion at the midpoint came in 1.3% above analysts’ estimates. Its non-GAAP profit of $0.12 per share was 38.5% above analysts’ consensus estimates.

Is now the time to buy Mobileye? Find out by accessing our full research report, it’s free.

Mobileye (MBLY) Q1 CY2026 Highlights:

- Revenue: $558 million vs analyst estimates of $517.6 million (27.4% year-on-year growth, 7.8% beat)

- Adjusted EPS: $0.12 vs analyst estimates of $0.09 (38.5% beat)

- Adjusted Operating Income: -$3.82 billion vs analyst estimates of $68.96 million (-684% margin, significant miss)

- The company lifted its revenue guidance for the full year to $1.98 billion at the midpoint from $1.94 billion, a 1.8% increase

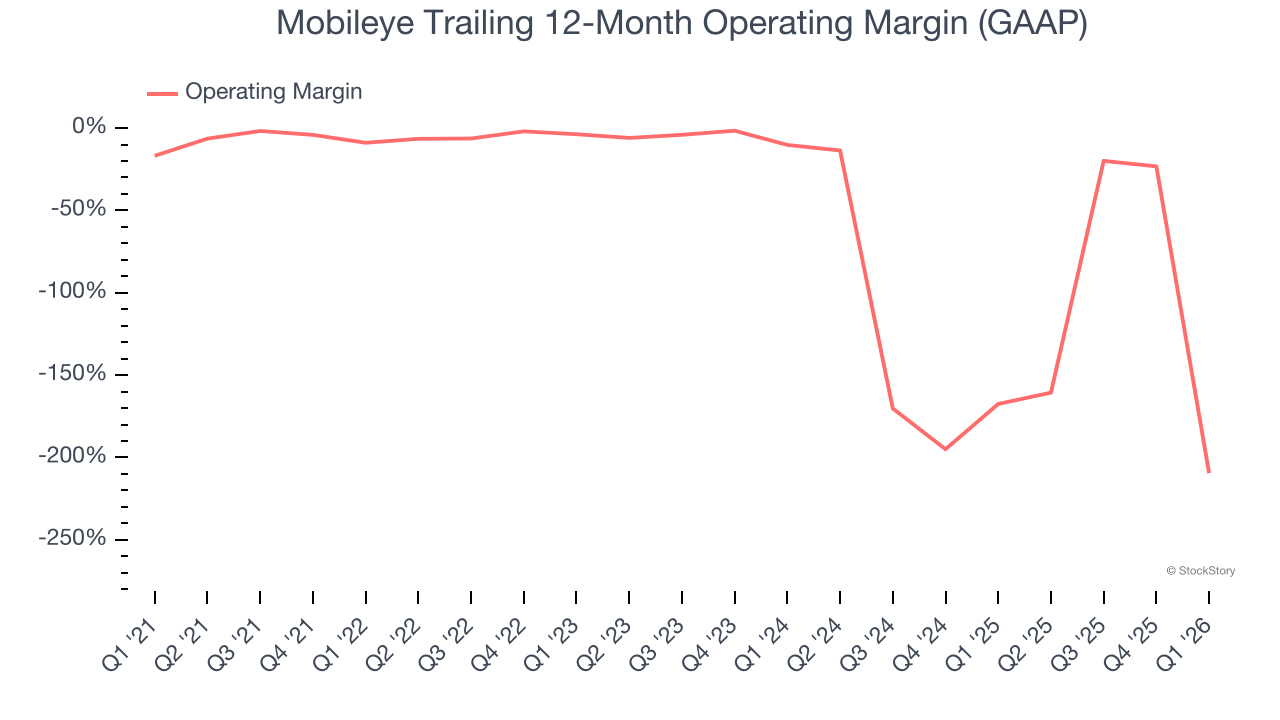

- Operating Margin: -698%, down from -26.7% in the same quarter last year

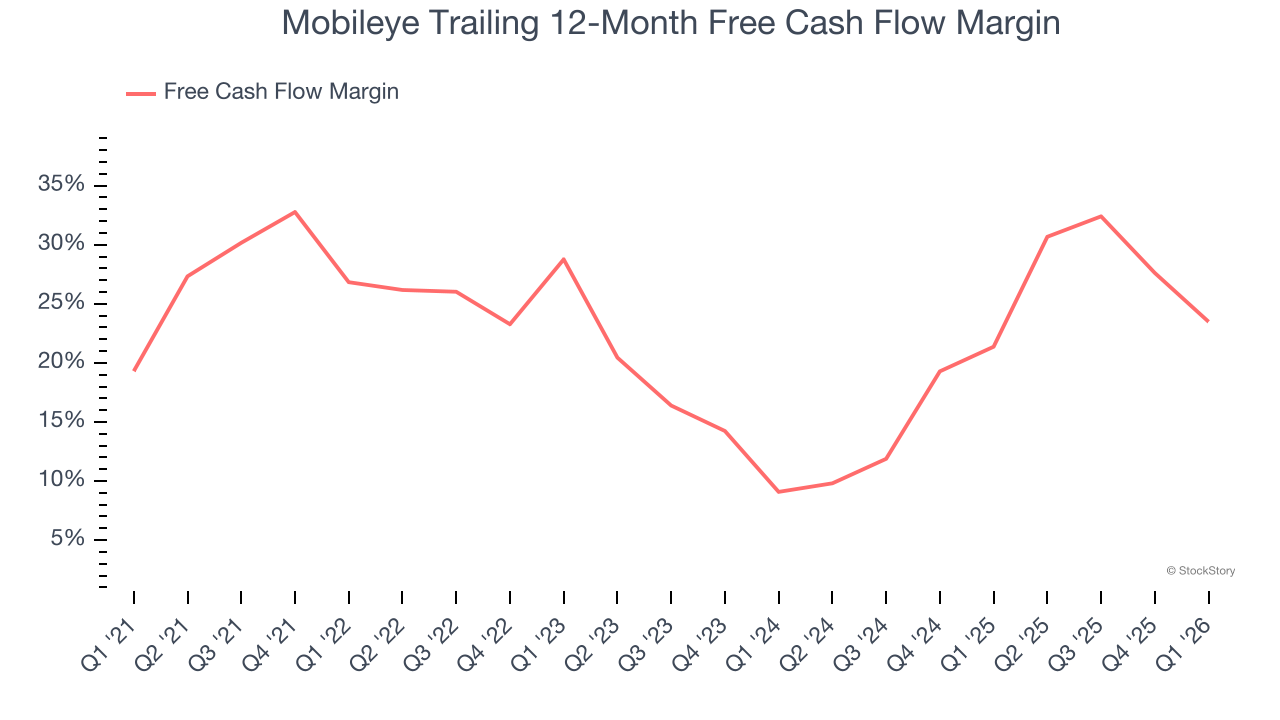

- Free Cash Flow Margin: 8.1%, down from 21.7% in the same quarter last year

- Market Capitalization: $6.65 billion

Company Overview

With its EyeQ chips installed in over 200 million vehicles worldwide, Mobileye (NASDAQ: MBLY) develops advanced driver assistance systems and autonomous driving technologies that help vehicles detect and respond to road conditions.

Revenue Growth

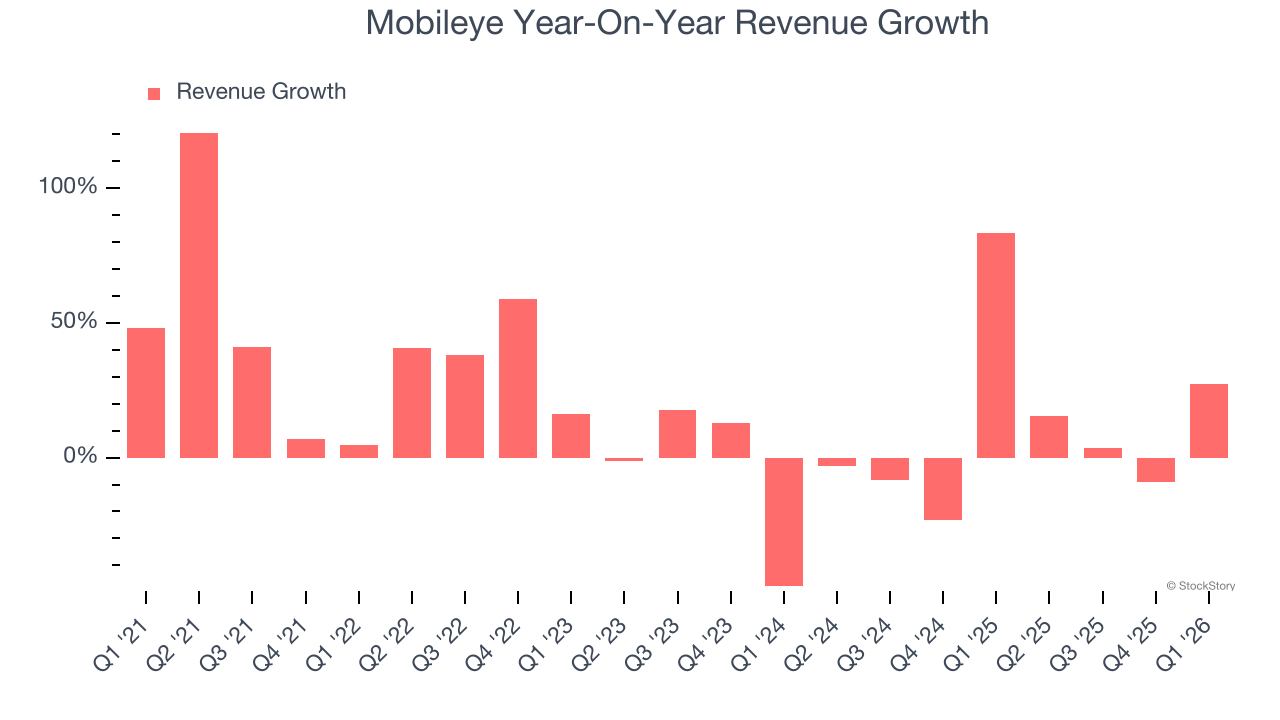

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Mobileye’s 13.1% annualized revenue growth over the last five years was excellent. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Mobileye’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.1% over the last two years was well below its five-year trend.

This quarter, Mobileye reported robust year-on-year revenue growth of 27.4%, and its $558 million of revenue topped Wall Street estimates by 7.8%.

Looking ahead, sell-side analysts expect revenue to decline by 3.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Mobileye’s high expenses have contributed to an average operating margin of negative 85.1% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Mobileye’s operating margin decreased significantly over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Mobileye’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q1, Mobileye generated a negative 698% operating margin.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Mobileye has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 21.7% over the last five years. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Mobileye’s margin dropped by 3.3 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal it is in the middle of an investment cycle.

Mobileye’s free cash flow clocked in at $45 million in Q1, equivalent to a 8.1% margin. The company’s cash profitability regressed as it was 13.6 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

Key Takeaways from Mobileye’s Q1 Results

It was good to see Mobileye beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its adjusted operating income missed. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 11.7% to $8.82 immediately after reporting.

Mobileye may have had a good quarter, but does that mean you should invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).