Over the past six months, Cigna’s stock price fell to $301.01. Shareholders have lost 7.9% of their capital, which is disappointing considering the S&P 500 has climbed by 16%. This might have investors contemplating their next move.

Following the drawdown, is now the time to buy CI? Find out in our full research report, it’s free.

Why Does Cigna Spark Debate?

With roots dating back to 1792 and serving millions of customers across the globe, The Cigna Group (NYSE: CI) provides healthcare services through its Evernorth Health Services and Cigna Healthcare segments, offering pharmacy benefits, specialty care, and medical plans.

Two Positive Attributes:

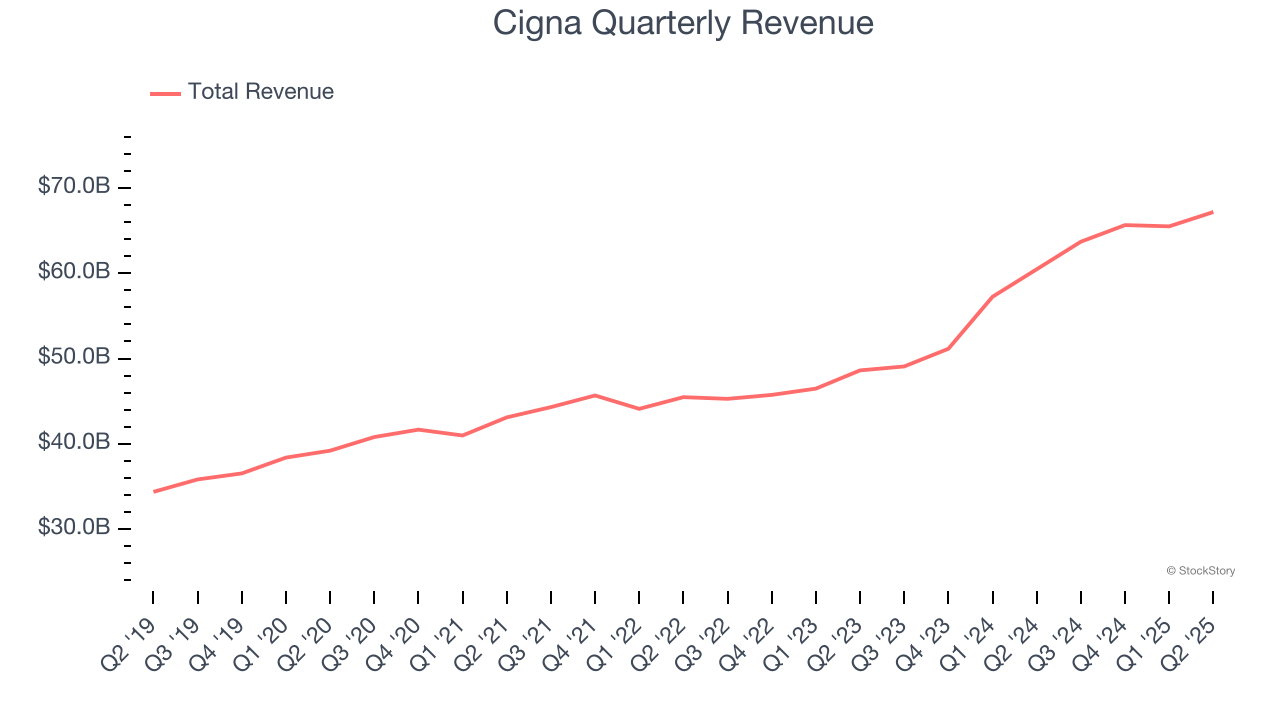

1. Long-Term Revenue Growth Shows Momentum

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Cigna’s sales grew at a decent 11.8% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $262 billion in revenue over the past 12 months, Cigna is one of the most scaled enterprises in healthcare. This is particularly important because health insurance providers companies are volume-driven businesses due to their low margins.

One Reason to be Careful:

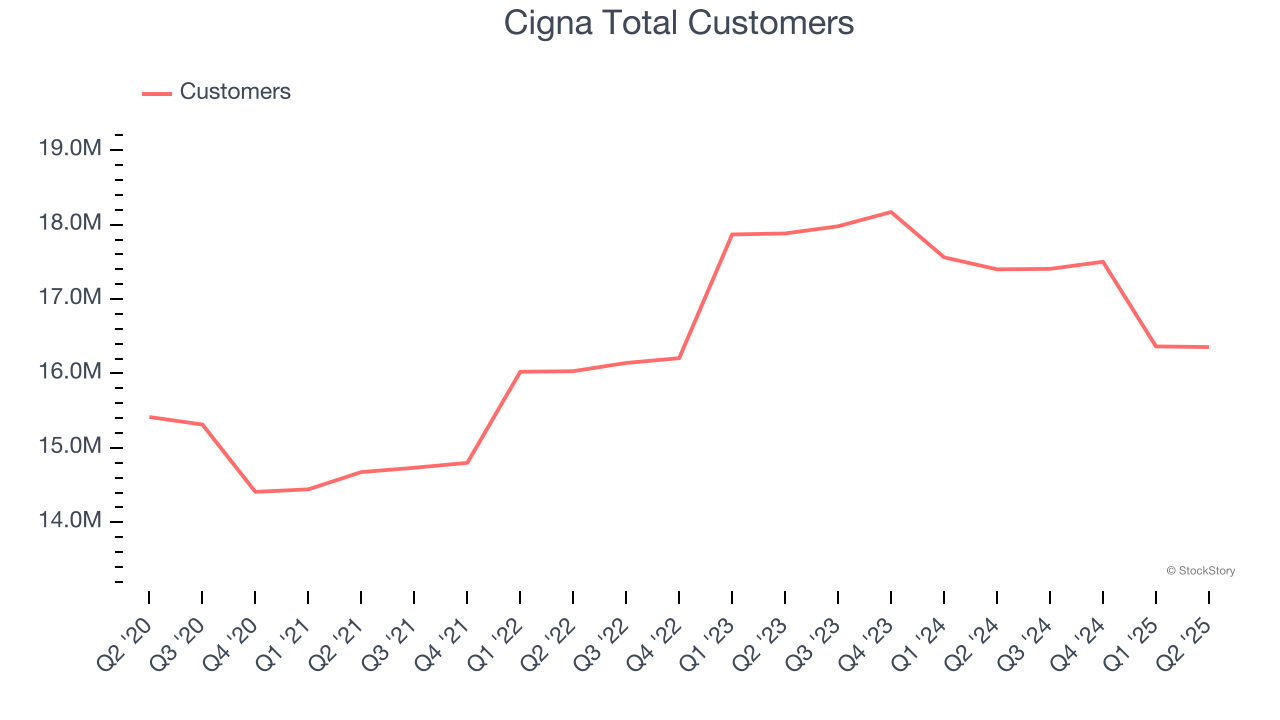

Customer Base Hits a Plateau

Revenue growth can be broken down into the number of customers and the average spend per customer. Both are important because an increasing customer base leads to more upselling opportunities while the revenue per customer shows how successful a company was in executing its upselling strategy.

Over the last two years, Cigna’s total customers were flat, coming in at 16.36 million in the latest quarter. This performance was underwhelming and shows the company faced challenges in landing new contracts. It also suggests there may be increasing competition or market saturation.

Final Judgment

Cigna has huge potential even though it has some open questions. With the recent decline, the stock trades at 9.5× forward P/E (or $301.01 per share). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

High-Quality Stocks for All Market Conditions

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.