Since February 2025, Mondelez has been in a holding pattern, posting a small loss of 4.1% while floating around $61.61. The stock also fell short of the S&P 500’s 8.8% gain during that period.

Is now the time to buy Mondelez, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Mondelez Not Exciting?

We're sitting this one out for now. Here are three reasons you should be careful with MDLZ and a stock we'd rather own.

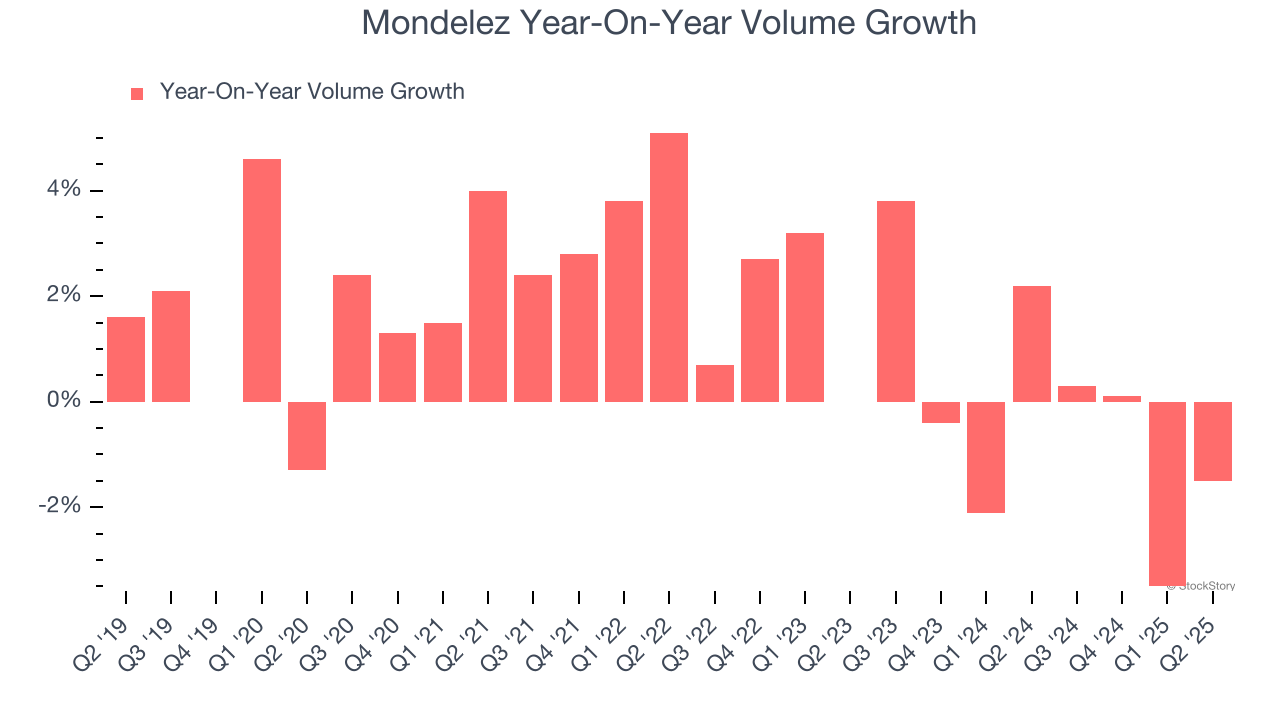

1. Sales Volumes Stall, Demand Waning

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Mondelez’s quarterly sales volumes have, on average, stayed about the same over the last two years. This stability is normal because the quantity demanded for consumer staples products typically doesn’t see much volatility.

2. Shrinking Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Analyzing the trend in its profitability, Mondelez’s operating margin decreased by 4.7 percentage points over the last year. This raises questions about the company’s expense base because its revenue

growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 12.4%.

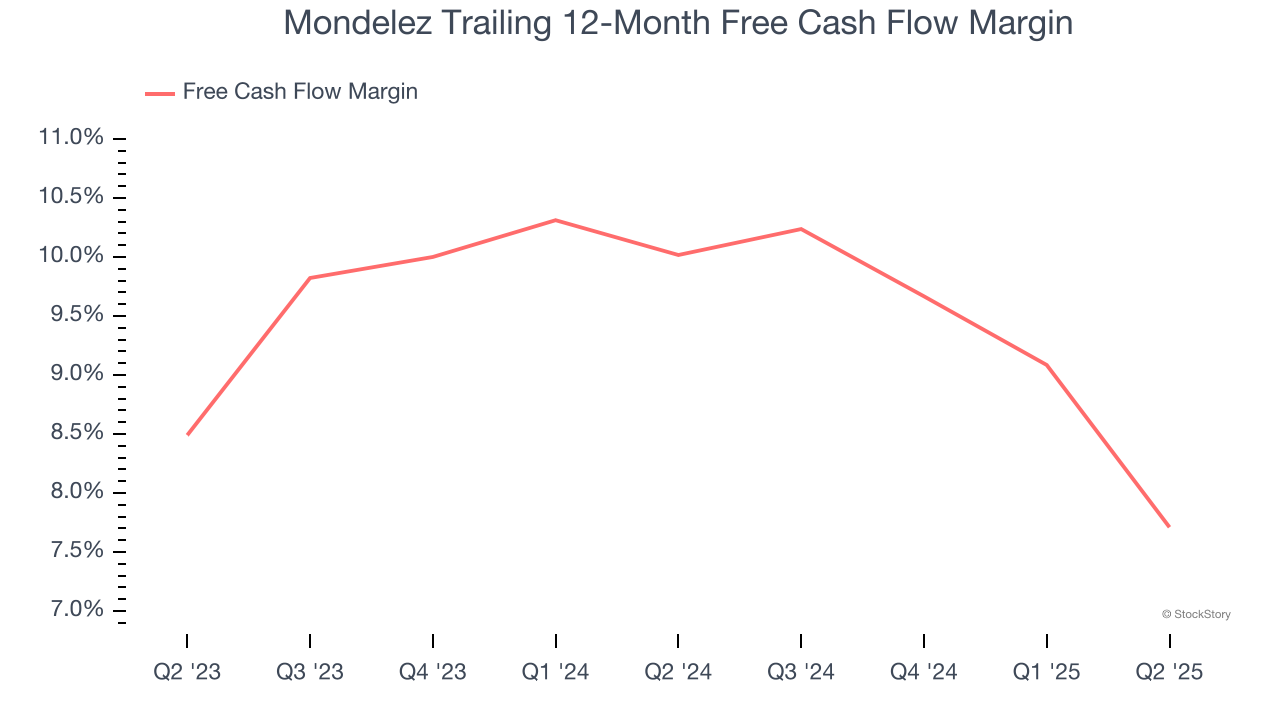

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Mondelez’s margin dropped by 2.3 percentage points over the last year. Continued declines could signal it is in the middle of an investment cycle. Mondelez’s free cash flow margin for the trailing 12 months was 7.7%.

Final Judgment

Mondelez isn’t a terrible business, but it isn’t one of our picks. With its shares lagging the market recently, the stock trades at 19.2× forward P/E (or $61.61 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward the Amazon and PayPal of Latin America.

High-Quality Stocks for All Market Conditions

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.