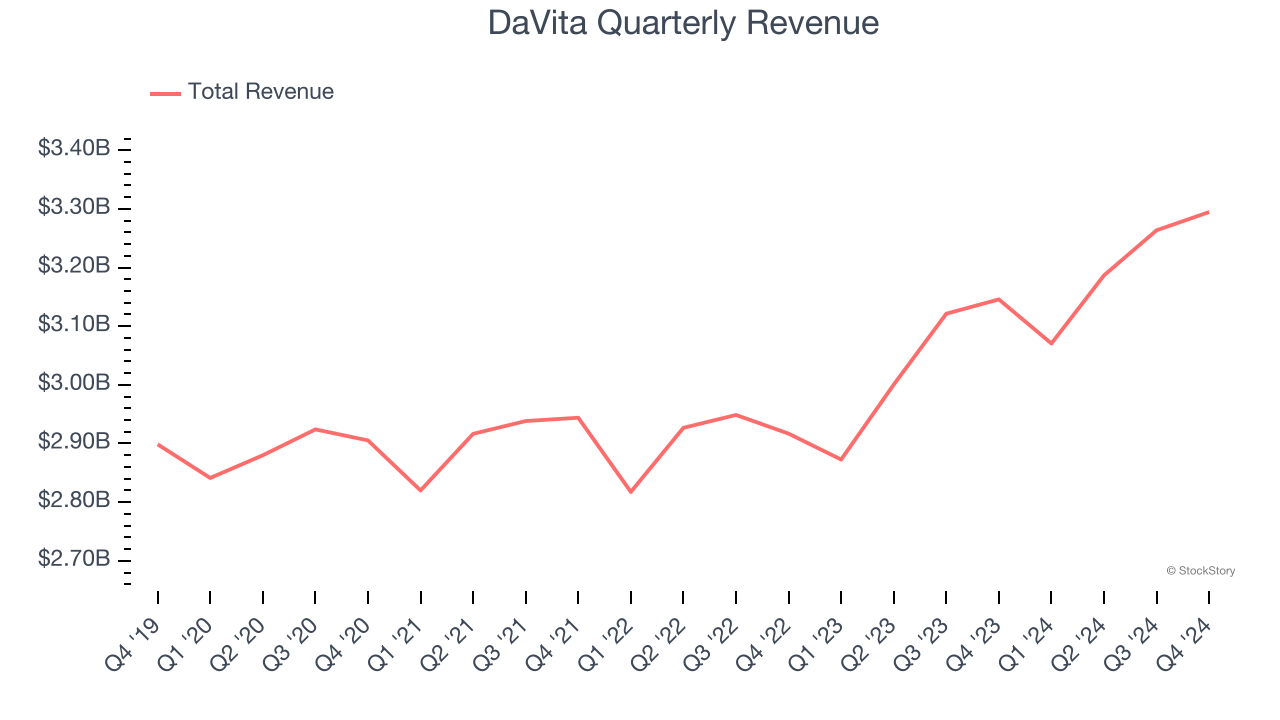

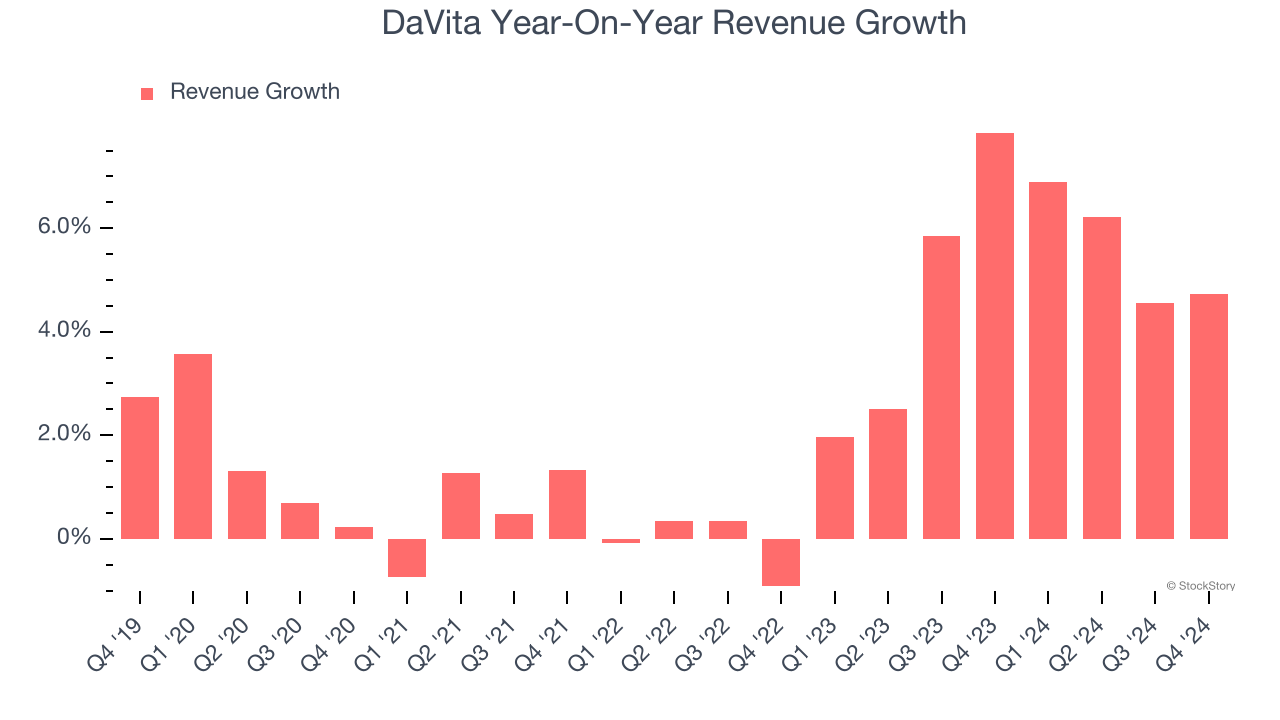

Dialysis provider DaVita Inc. (NYSE: DVA) beat Wall Street’s revenue expectations in Q4 CY2024, with sales up 4.7% year on year to $3.29 billion. Its non-GAAP profit of $2.24 per share was 4.3% above analysts’ consensus estimates.

Is now the time to buy DaVita? Find out by accessing our full research report, it’s free.

DaVita (DVA) Q4 CY2024 Highlights:

- Revenue: $3.29 billion vs analyst estimates of $3.27 billion (4.7% year-on-year growth, 0.9% beat)

- Adjusted EPS: $2.24 vs analyst estimates of $2.15 (4.3% beat)

- Adjusted EBITDA: $766.9 million vs analyst estimates of $644 million (23.3% margin, 19.1% beat)

- Adjusted EPS guidance for the upcoming financial year 2025 is $10.75 at the midpoint, missing analyst estimates by 6.1%

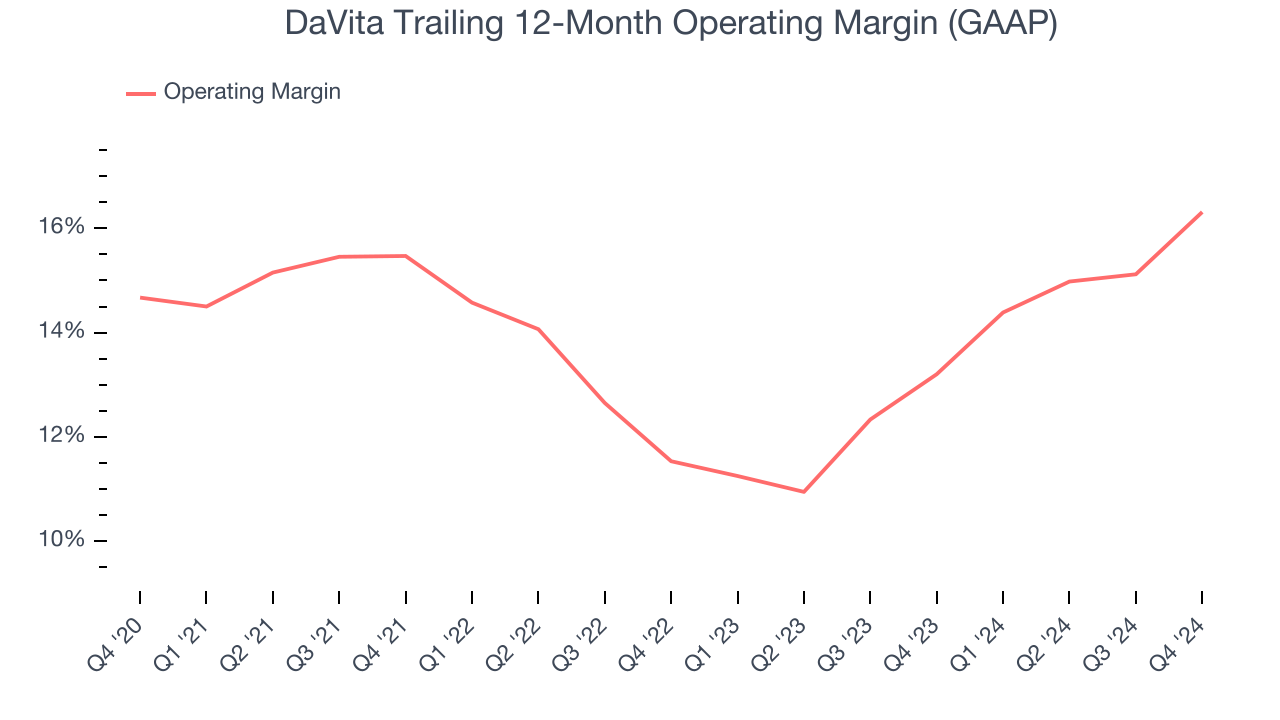

- Operating Margin: 17.2%, up from 12.4% in the same quarter last year

- Free Cash Flow Margin: 11.4%, up from 10.4% in the same quarter last year

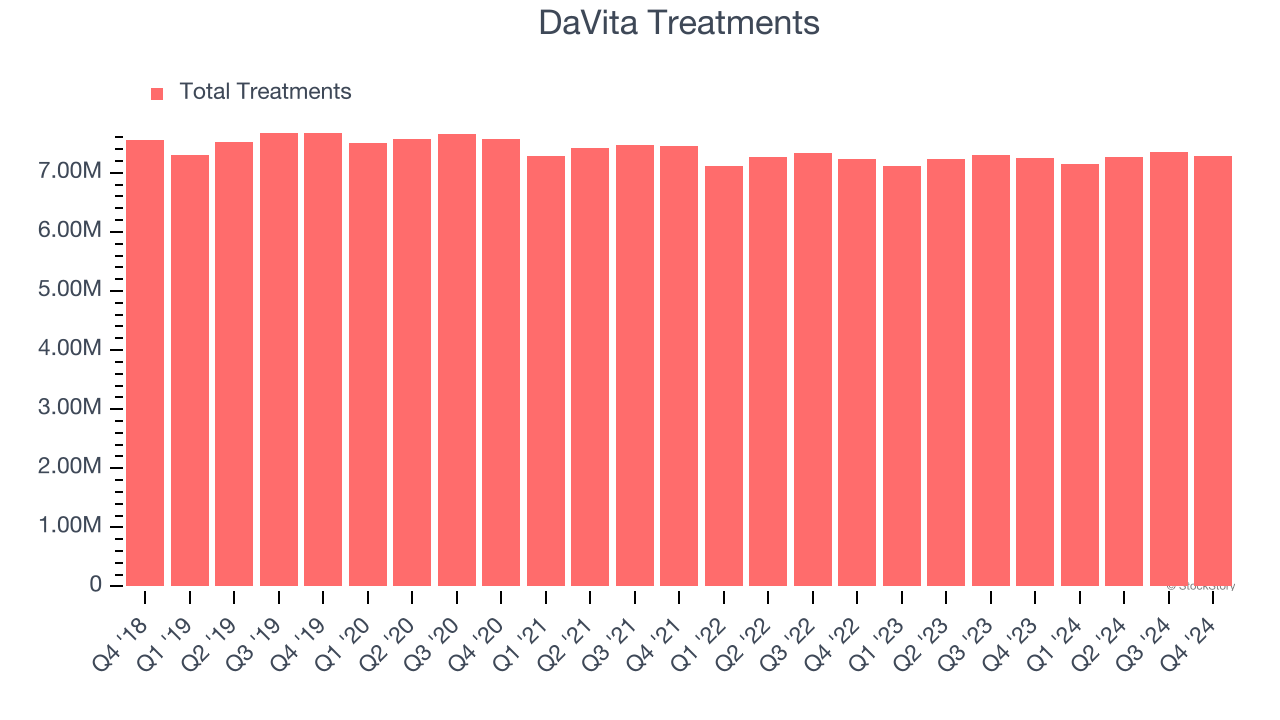

- Sales Volumes were flat year on year, in line with the same quarter last year

- Market Capitalization: $14.1 billion

"Despite a year with unique hurdles, we finished strong in 2024, producing full year adjusted operating income and adjusted EPS in the top half of our guidance range," said Javier Rodriquez, CEO of DaVita Inc.

Company Overview

Founded in 1994, DaVita Inc. (NYSE: DVA) provides dialysis services to patients with chronic kidney failure and end-stage renal disease, offering both in-center and at-home treatment options.

Outpatient & Specialty Care

The outpatient and specialty care industry delivers targeted medical services in non-hospital settings that are often cost-effective compared to inpatient alternatives. This means that they are more desired as rising healthcare costs and ways to combat them become more and more top-of-mind. Outpatient and specialty care providers boast revenue streams that are stable due to the recurring nature of treatment for chronic conditions and long-term patient relationships. However, their reliance on government reimbursement programs like Medicare means stroke-of-the-pen risk. Additionally, scaling a network of facilities can be capital-intensive with uneven return profiles amid competition from integrated healthcare systems. Looking ahead, the industry is positioned to grow as demand for outpatient services expands, driven by aging populations, a rising prevalence of chronic diseases, and a shift toward value-based care models. Tailwinds include advancements in medical technology that support more complex procedures in outpatient settings and the increasing focus on preventive care, which can be aided by data and AI. However, headwinds such as reimbursement rate cuts, labor shortages, and the financial strain of digitization may temper growth.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Unfortunately, DaVita’s 2.4% annualized revenue growth over the last five years was tepid. This fell short of our benchmarks and is a rough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. DaVita’s annualized revenue growth of 5.1% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can dig further into the company’s revenue dynamics by analyzing its number of treatments, which reached 7.28 million in the latest quarter. Over the last two years, DaVita’s number of treatments were flat. Because this is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, DaVita reported modest year-on-year revenue growth of 4.7% but beat Wall Street’s estimates by 0.9%.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

DaVita has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 14.3%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, DaVita’s operating margin rose by 1.6 percentage points over the last five years. This performance was mostly driven by its recent improvements as the company’s margin has increased by 4.8 percentage points on a two-year basis.

This quarter, DaVita generated an operating profit margin of 17.2%, up 4.8 percentage points year on year. This increase was a welcome development and shows it was recently more efficient because its expenses grew slower than its revenue.

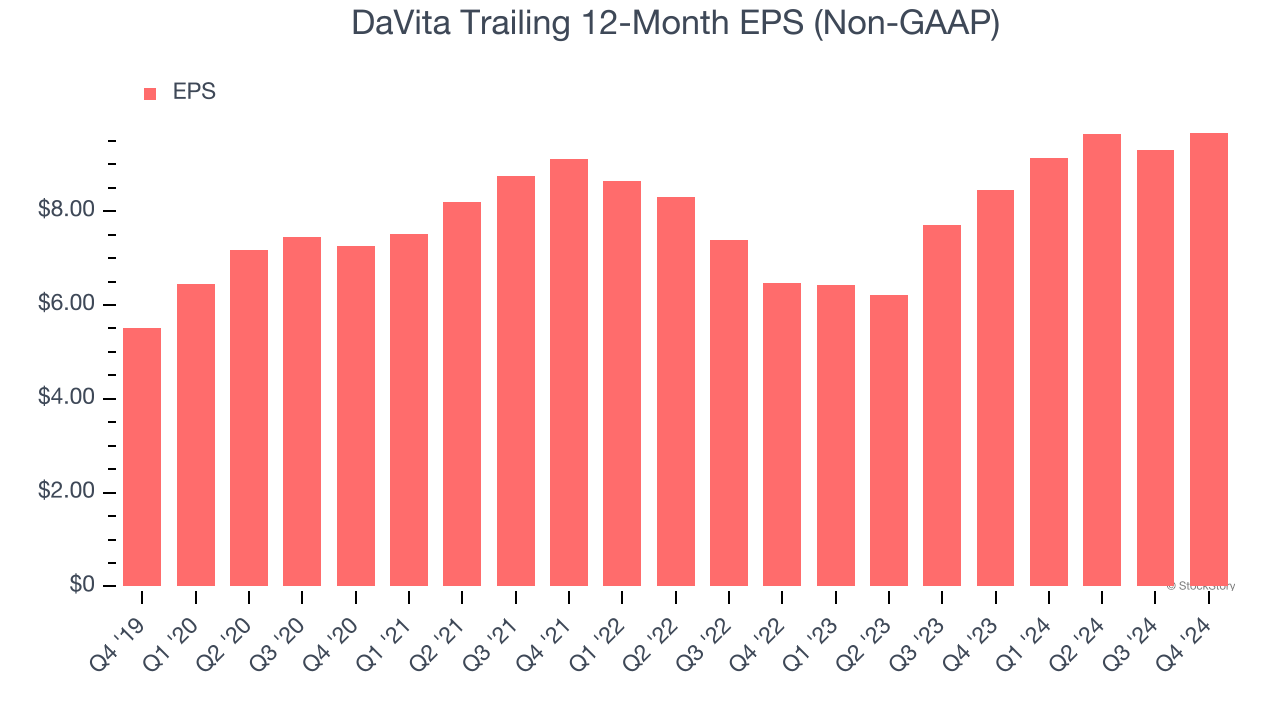

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

DaVita’s EPS grew at a remarkable 11.9% compounded annual growth rate over the last five years, higher than its 2.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

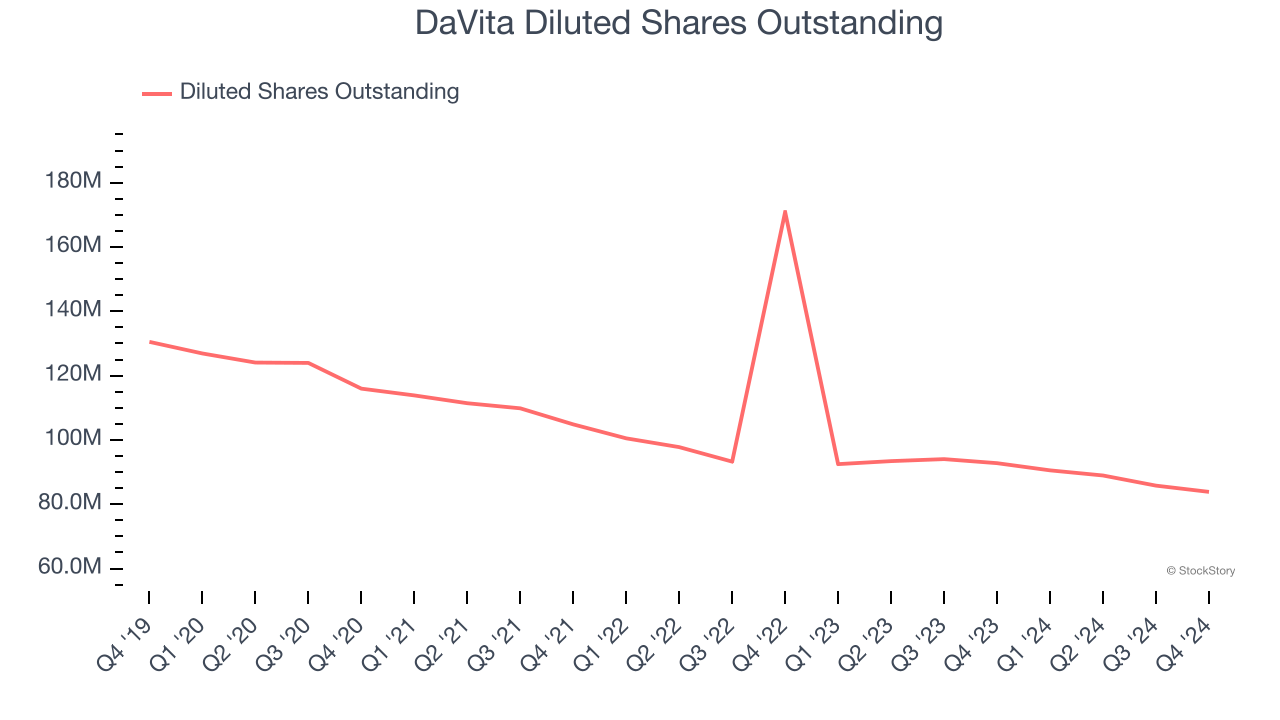

Diving into DaVita’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, DaVita’s operating margin expanded by 1.6 percentage points over the last five years. On top of that, its share count shrank by 35.7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, DaVita reported EPS at $2.24, up from $1.86 in the same quarter last year. This print beat analysts’ estimates by 4.3%. Over the next 12 months, Wall Street expects DaVita’s full-year EPS of $9.68 to grow 16.6%.

Key Takeaways from DaVita’s Q4 Results

It was good to see DaVita narrowly top analysts’ revenue expectations this quarter. On the other hand, its full-year EPS guidance missed significantly. Overall, this quarter could have been better. The stock traded down 9.7% to $159.80 immediately following the results.

DaVita may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.